Want to see our most updated article on ExxonMobil interest rates, click here.

Interest rates are tending upward, if this trend continues it will decrease the value of ExxonMobil employees' pension lump-sums. The IRS has recently released the Segment rates for the month of March, recorded at: 2.44% / 3.71% / 3.94%. Over the course of 2021 and now into 2022, interest rates at ExxonMobil increased significantly, which greatly reduced many lump sum payments. With record low rates culminating in the first quarter of 2021, ExxonMobil employees have since seen a significant increase in interest rates. We saw rates rise consistently in 2021 and with the announcement of March segment rates those waiting until the third quarter will likely see an even further reduction in lump sums. This ongoing trend upward looks be an early indicator of bad news for ExxonMobil employees opting for a lump-sum in the future.

Your pension is calculated based on your last date of employment and benefit start date. The benefit calculation is a defined benefit based on your years of service and final average pay. These, along with a social security offset are used to determine your single life annuity. All other forms of pension payments are based off this figure. This information is pertinent to all age groups, however those entering their Retirement Years will find the information particularly important.

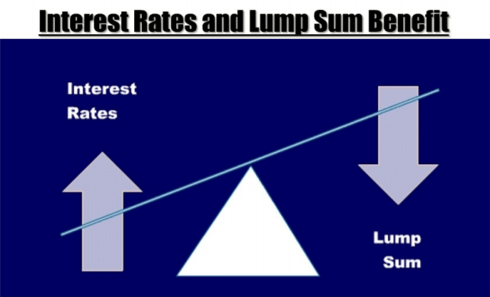

If you decide to take your pension as a lump sum, ExxonMobil will use interest rates and your age to calculate your lump sum payment. When interest rates move up or down, your pension lump sum amount will move in an inverse relationship.

ExxonMobil Pension Lump Sum Calculation:

Quarter 3 Interest Rates

Grandfathered Employees

If you are at least 63 years old with at least 23 years of ExxonMobil service by December 31, 2020, you are considered grandfathered into the old pension calculation method. The old pension calculation method uses the 30-year Treasury bond interest rates. ExxonMobil will take the average Treasury rate for the fourth, fifth, and sixth months prior to the quarter you elect to “commence” your pension benefit, also known as your benefit commencement date (BCD). Then ExxonMobil multiplies this rate by 95% and rounds to the nearest quarter percent. For example, if you retire in July and want to receive your pension in August, ExxonMobil will take the average Treasury rate for January, February, and March multiplied by .95, and then round to the nearest quarter percent.

The grandfathered rate for the third quarter is now set at 2.25%, a sizeable increase from the first two quarters of 2022. The trend of rising rates might be sufficient reason for some employees who are considering retirement to take advantage of current rates and retire this year. In order to take advantage of the current low interest rates, you would need to commence your retirement before June 30, 2022.

Non‐Grandfathered Employees

If you are not at least 63 years old with at least 23 years of ExxonMobil service by December 31st, 2020, then you are not grandfathered into the old pension calculation method. In calculating your lump sum, ExxonMobil will use the average of the short, intermediate and long term corporate bond segment rates for the fourth and fifth months prior to the quarter you plan to commence your pension benefit. For instance, if you plan to retire in July and to start your pension in August of 2022, ExxonMobil will use the average corporate bond interest rates for the months of February and March of 2022 to calculate your pension lump sum (the average of the fourth and fifth month prior to the quarter you plan to start your pension).

The rates for the first quarter of 2021 were the lowest rates in history for non-grandfathered employees, producing some of the highest lump sums since this calculation method went into effect almost a decade ago. Rates for the second quarter rose moderately, but the newly announced rates for the third quarter of 2022 are significantly higher, meaning that an even further reduction in lump sum values is likely.

| ExxonMobil Lump Sum Interest Rates for Q1, Q2 & Q3 2022: |

|

| |

1st Segment |

2nd Segment |

3rd Segment |

|

| March 2022 |

2.44 |

3.71 |

3.10 |

|

| February 2022 |

1.02 |

2.72 |

3.08 |

Grandfathered Rates |

| Q3 2022 Blended Rates |

2.16 |

3.53 |

3.82 |

2.25% |

| Q2 2022 Blended Rates |

1.09 |

2.72 |

3.09 |

1.75% |

| Q1 2022 Blended Rates |

0.68 |

2.53 |

3.09 |

1.75% |

| |

| Q1 2020 Blended Rates: |

2.11 |

3.04 |

3.63 |

2.25% |

| Q1 2021 Blended Rates: |

0.52 |

2.27 |

3.09 |

1.25% |

For lump-sum conversions, the pension annuity is discounted to a present value using the first segment rate for the first five years of expected payments, the second segment rate for the next 15 years of expected payments and the third segment rate for all years of expected payments over 20. Because the annuity is discounted based on mortality as well as interest rates, the present value of each monthly payment reduces as the probability of living to receive each payment reduces. The older you are when you commence your pension benefit, the fewer the number of years that will be valued using the third segment rate (20+ years) and, conversely, the younger you are, the greater the number of years that will be valued using the third segment rate.

| "...on average, a 1% change could increase or decrease your pension lump sum by roughly 10%" |

|

This methodology essentially means that there will be a unique quarterly interest rate (lump-sum conversion factor) for each year and month of birth.

How Do Rate Changes Affect Your ExxonMobil Pension?

Pension pricing is based on interest calculations, therefore making a slight adjustment in your retirement date may have a significant financial impact on your pension due to changing rates each month.

Everything else held equal, a lower interest rate will produce a higher lump sum. The exact changes depend on your specific age, but on average a 1% change in rates can equate to an 8% to 12% change in lump sums. So, on average, a 1% change could increase or decrease your pension lump sum by roughly 10%.

The changes from the second quarter of 2022 to the third quarter of 2022 may account for about a 5-8% decrease in lump sums, depending on whether or not you are considered grandfathered. Prior to this latest release, even though rates had been rising, they were still below rates from the end of 2019. What has now changed, is that we are seeing even higher rates starting in the third quarter, meaning that any bump you have seen in your lump sum will likely completely diminish if your benefits are initiated next quarter. From the lowest blended rates in the beginning of 2021, the middle segment rate has increased by 1.26% which could equate to an 11%-13% decrease in your lump sum. With no sign of this upward trend in sight at the moment, it is very important we run or update your cash flow analysis so you know all your claiming options.

You do not have to commence your pension as soon as you retire. You have the option to defer it. That may be beneficial if rates are dropping and/or you are under 60 years old. If you take your pension prior to age 60 there are age penalties and you will not receive 100% of your pension benefit.

The Retirement Group is not affiliated with nor endorsed by Chevron. We are an independent financial advisory group that focuses on transition planning and lump sum distribution. Neither The Retirement Group or FSC Securities provide tax or legal advice. Please call our office at 800-900-5867 if you have additional questions or need help in the retirement planning process.

Securities through FSC Securities Corporation, member FINRA/SIPC and investment advisory services offered through The Retirement Group, LLC, a registered investment advisor not affiliated with FSC Securities Corporation. Office of Supervisor Jurisdiction: 5414 Oberlin Dr #220, San Diego CA 92121. 800-900-5867