Retirement Planning Handbook for Farmers Insurance Group Employees

28

/General/General%205.png?width=1280&height=853&name=General%205.png)

The traditional rule of thumb with retirement was that you will need 70-80% of your income in retirement to be able to live a comfortable life. However, everyone’s situation is different: some people find that they actually spend more money in retirement than they did the last few previous years and others find they are perfectly content to live their mature years modestly with simple pleasures. Completing a retirement budget is a far more comprehensive way to examine your money needs than simply relying on a percentage of your current expenses. While it can be difficult to project your lifestyle into the future – especially if you are currently many years away from leaving Farmers Insurance Group – begin by using your current budget as a jumping-off point. Think about expenses that may be less in retirement - like clothing or gas – and expenses that could be more - like airline tickets or healthcare expenses. Of course, remember to calculate inflation, especially if you are more than a year or two from your Farmers Insurance Group retirement.

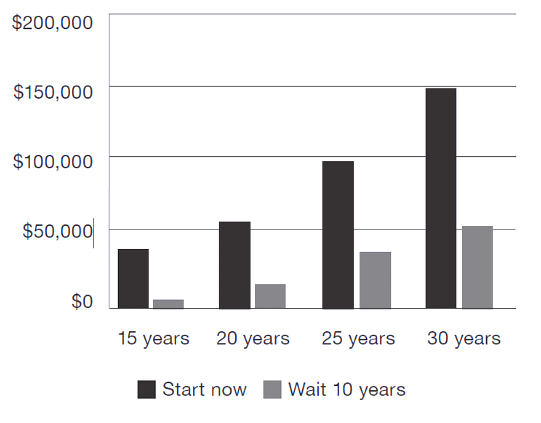

The financial calculators at www.balancepro.net can help you crunch the numbers. If you are close to retiring from Farmers Insurance Group and want to see if your budget is realistic, give it a test run for a month. The chart below reflects a savings plan of $2,000 a year at nine percent interest.

Knowing you will have enough on a monthly basis to live comfortably is great, but how do you know if it will last? After all, you don’t know how long you might live, especially with increasing life spans resulting in retirements of 30 or even 40 years. If you are worried about stretching your dollars over the full length of your retirement from Farmers Insurance Group, consider meeting with a financial planner and taking one or more of the following steps:

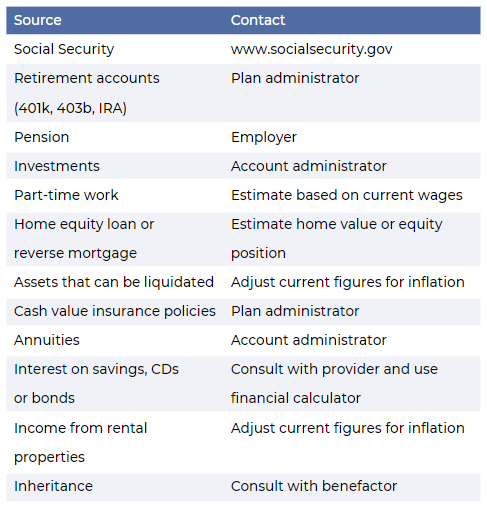

If you are currently among the gainfully employed, you are used to receiving a regular paycheck from Farmers Insurance Group each month. In retirement, this may be different, since you could have several sources of income making up your monthly “paycheck.” To see what your current retirement paycheck looks like, consider all potential sources of income:

Add your monthly expected retirement totals from all these potential sources of income to see how your income projection currently sizes up. If this falls short of what you had projected in your retirement budget, look for ways to increase the amount you are currently putting toward your Farmers Insurance Group retirement or ways to generate extra income during retirement.

Other Articles of Interest

Articles Relevant to Farmers Insurance Group Employees

Loading...

-

-

8 Tenets of Choosing a Mutual Fund -

Use of Escrow Accounts: Divorce -

Section 303 Stock Redemption Buy-Sell Agreement -

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

Medicare Open Enrollment Is Here: How Are Costs Changing for 2023? -

2022 High Net Worth Tax Planning -

Policy Roadmap -

Section 179 Deductions -

Learn About the Path to Retirement -

Contemplating Change: 7 Key Factors When Considering a Transition from Your Company -

How Are Workers Impacted by Inflation & Rising Interest Rates? -

Lump-Sum vs Annuity and Rising Interest Rates -

Advice for Retirees Trying to Survive a Bear Market -

5 Most Important Things to do Before Leaving Your Company -

Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

-

8 Tenets of Choosing a Mutual Fund -

Use of Escrow Accounts: Divorce -

Section 303 Stock Redemption Buy-Sell Agreement -

Medicare Open Enrollment Is Here: How Are Costs Changing for 2023? -

2022 High Net Worth Tax Planning -

Policy Roadmap -

Section 179 Deductions -

Learn About the Path to Retirement -

Contemplating Change: 7 Key Factors When Considering a Transition from Your Company -

How Are Workers Impacted by Inflation & Rising Interest Rates? -

Lump-Sum vs Annuity and Rising Interest Rates -

Advice for Retirees Trying to Survive a Bear Market -

5 Most Important Things to do Before Leaving Your Company -

Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

For more information you can reach the plan administrator for Farmers Insurance Group at p.o. box 4363 Woodland Hills, CA 91365-4363; or by calling them at 800-451-0797.

Disclaimer: Securities offered through Osaic Wealth Inc, member FINRA/SIPC. Investment advisory services offered through The Retirement Group, LLC. a registered investment advisor not affiliated with Osaic Wealth Inc. *We are not affiliated with or endorsed by Farmers Insurance Group. This message and any attachments contain information, which may be confidential and/or privileged, and is intended for use only by the intended recipient. Any review, copying, distribution or use of this transmission is strictly prohibited. If you have received this transmission in error, please (i) notify the sender immediately and (ii) destroy all copies of this message. The Retirement Group, LLC is registered to conduct advisory business in the following states: AZ, CA, CO, FL, ID, IL, IN, LA, MD, MI, MO, NE, NV, NJ, NY, NC, OK, OR, PA, SC, SD, TX, UT, VA, WA. Office of Supervisory Jurisdiction: 5414 Oberlin Dr #220, San Diego CA 92121 (800) 900-5867

Originally Posted: December 1, 2022

Company:

Farmers Insurance Group*

Plan Administrator:

p.o. box 4363

Woodland Hills, CA

91365-4363

800-451-0797

*Please see disclaimer for more information

Featured Articles

Articles Relevant to Farmers Insurance Group Employees

Loading...

-

-

8 Tenets of Choosing a Mutual Fund

8 Tenets of Choosing a Mutual Fund

-

Use of Escrow Accounts: Divorce

Use of Escrow Accounts: Divorce

-

Section 303 Stock Redemption Buy-Sell Agreement

-

-2.png) Medicare Open Enrollment Is Here: How Are Costs Changing for 2023?

Medicare Open Enrollment Is Here: How Are Costs Changing for 2023?

-

2022 High Net Worth Tax Planning

2022 High Net Worth Tax Planning

-

Policy Roadmap

Policy Roadmap

-

Section 179 Deductions

Section 179 Deductions

-

Learn About the Path to Retirement

Learn About the Path to Retirement

-

Contemplating Change: 7 Key Factors When Considering a Transition from Your Company

Contemplating Change: 7 Key Factors When Considering a Transition from Your Company

-

How Are Workers Impacted by Inflation & Rising Interest Rates?

How Are Workers Impacted by Inflation & Rising Interest Rates?

-

Lump-Sum vs Annuity and Rising Interest Rates

Lump-Sum vs Annuity and Rising Interest Rates

-

Advice for Retirees Trying to Survive a Bear Market

Advice for Retirees Trying to Survive a Bear Market

-

5 Most Important Things to do Before Leaving Your Company

5 Most Important Things to do Before Leaving Your Company

-

Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

-

8 Tenets of Choosing a Mutual Fund

-

Use of Escrow Accounts: Divorce

-

-

Medicare Open Enrollment Is Here: How Are Costs Changing for 2023?

-

2022 High Net Worth Tax Planning

-

Policy Roadmap

-

Section 179 Deductions

-

Learn About the Path to Retirement

-

Contemplating Change: 7 Key Factors When Considering a Transition from Your Company

-

How Are Workers Impacted by Inflation & Rising Interest Rates?

-

Lump-Sum vs Annuity and Rising Interest Rates

-

Advice for Retirees Trying to Survive a Bear Market

-

5 Most Important Things to do Before Leaving Your Company

-

Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)