New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Averaging Your Dollar Vs. One-time Investment for L3Harris Employees

Oil market turbulence continues to ripple through the broader economy, with crude swinging between $50 and $120 per barrel and annualized volatility near 80%. Jet fuel costs, petrochemical composite materials, and fixed-price contract structures mean elevated crude prices create margin pressure across the aerospace supply chain. Comprehensive financial planning at L3Harris benefits from understanding how energy price volatility creates indirect effects on inflation, interest rates, and portfolio valuations that affect long-term wealth building. Working with a financial advisor helps ensure that energy market uncertainty does not undermine your long-term retirement and financial goals.

Many L3Harris employees and retirees have told us how difficult it feels to evaluate certain investment strategies. To evaluate DCA as an investment strategy we will compare it to lump sum investing for rolling 10-year investment periods with monthly steps. This means that starting with the first available month we will examine DCA and lump sum investing through the following decade of returns, and then move the start point one month ahead. For most data series in our sample, this results in 485 10-year periods. For Canada, we have 652 periods, and 1013 for the US. We will evaluate a 12-month DCA implementation, which means splitting up a lump sum into 12 equal monthly investments, against a single lump sum investment. The following chart shows an approximate allocation between cash and stocks over the course of a 12-month DCA period for $1,000,000 of starting cash.

Â

Figure 1 – Dollar-Cost Averaging Illustration

Â

Â

Before finalizing any estate plan, it is worth examining how L3Harris's employer-sponsored benefits fit into the broader picture. According to publicly available information, L3Harris maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. L3Harris also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with L3Harris's HR or benefits team for the most current details.

Source:Â Benjamin Felix, Portfolio Manager, PWL Capital Inc.

Â

In our model, the cash will earn interest at the rate of One-Month US Treasury Bills while it is waiting to be invested. The portfolios are 100% invested in stocks when fully implemented. All analysis has been conducted in US dollars using monthly returns for One-Month US Treasury Bills and the six global stock markets listed in Table 1.

Â

Table 1 – Stock Market Indexes

Â

Â

Source: Benjamin Felix, Portfolio Manager, PWL Capital Inc.

Â

In order to evaluate LSI relative to DCA, we have chosen to look at the ending performance of an investment after 10 years. First, we evaluated the full data series for each market to understand the average outcomes. We isolated the most extreme bad outcomes for LSI to examine how DCA performed in those periods. Knowing that we cannot predict when LSI will have its worst outcomes, we then compared LSI to DCA during bear markets and when stock prices are high.

Â

Â

Data source:Â Dimensional Returns Web, CRSP, PWL Capital Inc.

Â

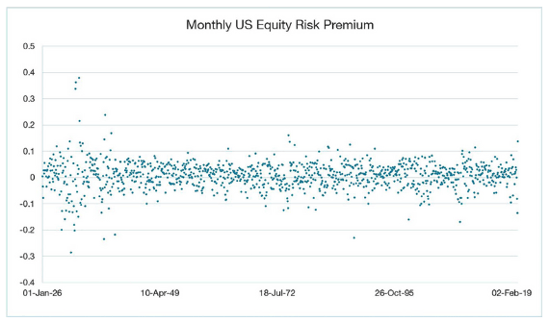

The monthly US equity premium has been remarkably consistent, within a range, throughout history. It has an arithmetic average of 0.65%, and it has been positive 60% of the time. There tend to be periods, visible in Figure 2, where the monthly premium becomes more volatile; volatility clustering is a well-known phenomenon. Over periods longer than one month we also observe characteristic negative skewness - frequent small gains and a few extreme losses.

Â

Given the nature of stock returns, we would expect a stock investor to achieve positive returns with roughly the same frequency as the equity risk premium being positive. For the remainder of this paper, we will be comparing lump sum investing to dollar-cost averaging in terms of absolute returns, as opposed to observing their risk premiums. US stock returns have been positive in absolute terms 63% of the time in the historical data.

For most markets, and on average across markets, we find that roughly two-thirds of the time LSI beats DCA over 10-year periods in terms of ending assets. The exception is Japan which is unsurprising given its unique long-term stock market outcome; Japan’s equity market has trailed One-Month US Treasury Bills since 1990.

Â

Table 2 – LSI vs. DCA for 10-Year Historical Periods

Â

Â

Data source: Dimensional Returns Web, CRSP, MSCI, S&P Dow Jones Indices, PWL Capital Inc.

Â

The basic insight that we draw from this result is that, on average, LSI leads to greater ending wealth than DCA. To quantify the extent to which LSI tends to beat DCA we examined the 10-year annualized performance difference for the full sample. An annualized figure stated as a percentage makes for an easy comparison to familiar items like fees and withholding taxes. On average, DCA is leaving a meaningful amount of expected returns on the table at 0.38% annualized over ten years in the historical data; this should not be a surprise considering that DCA delays exposure to higher expected returning stocks.

Â

Table 3 – LSI vs. DCA Annualized 10-Year Performance Difference

Â

Â

Â

Comparing average outcomes is interesting but it does not speak to the dispersion of outcomes. Even if DCA is worse on average in terms of expected average outcomes, maybe it offers some protection on the downside. To assess this, we calculate the difference in annualized returns for LSI and DCA over 10-year periods and sort the data into percentiles. The 10th percentile is the bottom 10% of outcomes, the 50th percentile is the median, and the 90th percentile is the top 10%.

Â

Table 4 – Difference in Annualized Returns (LSI – DCA)

Â

Â

Data source:Â Dimensional Returns Web, CRSP, MSCI, S&P Dow Jones Indices, PWL Capital Inc.

Â

It should be clear from Table 4 that LSI is beating DCA by a healthy margin on average. In the best 10% of outcomes (90th percentile), more has been gained by LSI over DCA than what has been lost in the worst 10% of outcomes. The median outcome is positive, and the distribution is negatively skewed. None of this should be a surprise considering the positive expected risk premium of stocks over treasury bills, and the left-skewed distribution of stock returns. Figure 3 shows the shape of the distribution of the differences in outcomes for LSI less DCA in terms of 10-year annualized returns.

Â

Figure 3 – Distribution of Differences in 10-Year Annualized Outcomes (LSI - DCA)

Â

Â

Data source:Â Dimensional Returns Web, CRSP, MSCI, S&P Dow Jones Indices, PWL Capital Inc.

Â

At the most extreme, the far left and right tails of the distribution, LSI does look worse than DCA. This observation is consistent with a negatively skewed distribution; we see that most of the outcomes are good, but the worst outcomes are more extreme than the best outcomes. This validates the idea that DCA might be able to offer protection from the worst outcomes, but it comes at a significant cost in terms of expected returns.

Â

Table 5 – LSI vs. DCA in the 10th Percentile LSI Historical Periods

Â

Â

Data source:Â Dimensional Returns Web, CRSP, MSCI, S&P Dow Jones Indices, PWL Capital Inc.

Â

In half of our markets, LSI still beats DCA most of the time even when LSI has delivered its worst historical outcomes; this is also true with an equal-weighted average of all markets in the sample. The results are not as strongly in favor of LSI as the full data series but remember that we have intentionally selected the worst LSI outcomes for this sample. While the number of outcomes is evenly matched, the bad outcomes in this case are worse in magnitude than the good ones. The result is a negative difference in annualized 10-year performance. This should not be surprising considering our intentional selection of the worst LSI outcomes in the sample.

Â

Table 6 – Difference in Annualized Returns for 10th Percentile LSI Outcomes (LSI – DCA)

Â

Â

Data source:Â Dimensional Returns Web, CRSP, MSCI, S&P Dow Jones Indices, PWL Capital Inc.

Â

Even under artificial conditions of a known bad future outcome for LSI, DCA offers less than a 50% shot at an improvement. DCA does however offer an edge when the magnitude of positive and negative outcomes is considered – despite the roughly even split between good and bad outcomes, the bad outcomes are worse than the good outcomes are good. This seems to give credence to the mythical ability of DCA to improve an extremely bad LSI outcome. An important nuance in the data is that the worst LSI outcomes relative to other LSI outcomes do not correspond with the worst LSI outcomes relative to DCA outcomes. The most extreme instances of underperformance for LSI relative to DCA have less to do with the LSI outcome being extremely bad and more to do with the DCA outcome being extremely good. In other words, lucky timing for DCA, as opposed to avoiding unlucky timing for LSI, drives the difference in the most extreme cases.

Â

Given that it is impossible to predict which time periods will result in the worst outcomes for a lump sum investment, we next turn to two signals commonly believed to offer forward-looking insight into future investment returns.

Â

Â

Data source:Â Dimensional Returns Web, CRSP, MSCI, S&P Dow Jones Indices, PWL Capital Inc.

Â

We again find that LSI produces a better outcome than DCA most of the time in most countries in the sample. L3Harris employees and retirees should note that the US experience is significantly impacted by the enormous volatility and seemingly perpetual market drops in the 1930s. We find that, on average, LSI beats DCA by a 10-year annualized 0.25% when the investment period begins with the month after a drop of 20% or more has occurred. Echoing the experience of the full data series we also see that there has historically been more to gain from LSI in the 90th percentile of outcomes than there has been to lose in the 10th percentile. DCA is not offering protection from bad outcomes without also exposing us to a greater risk of missing good outcomes.

Â

Table 8 – Difference in Annualized Returns Starting at Bear Markets (LSI – DCA)

Â

Â

Data source:Â Dimensional Returns Web, CRSP, MSCI, S&P Dow Jones Indices, PWL Capital Inc.

Â

It's important for L3Harris employees to keep in mind that our trigger to begin the investment period is a 20% drop. In some cases, a 20% drop is followed by more drops, while in other cases it is followed by a rebound. Based on the data in Tables 7 and 8 we can see that rebounds are more impactful, on average than further drops. This results in LSI delivering a better result than DCA most of the time, even during periods of market volatility.

Â

Â

Data source:Â Dimensional Returns Web, CRSP, Barclays Research, PWL Capital Inc.

Â

While it may seem concerning, this observation suffers from a massive bias: at any point in time we do not have the full set of past and future Shiller CAPE data to base a decision - we only have past data in our possession. We adjust for this by measuring the market’s expensiveness only relative to historical data for each data point. For example, for January 1926 we are comparing the Shiller CAPE to the set of data from February 1872 to January 1926, not from February 1872 to May 2026 to test for expansiveness. In this case, LSI beats DCA 63.70% of the time.

Â

Table 10 – LSI vs. DCA when Stock Prices are High Relative to Backward-looking History

Â

This exercise is to remind L3Harris employees and retirees that while valuations may look high at a point in time, they can always get higher. Japan might be a particularly interesting case study on the usefulness of market valuations in making the LSI vs. DCA decision. We have less data for Japan, so instead of comparing historical Japanese data, we will compare Japanese valuations to US data to determine expensiveness. The highest level of the monthly Shiller CAPE for the full US historical data series is 44.19 which occurred in December 1999. Japan exceeded this level in May 1986 with a Shiller CAPE of 44.31. While the Japanese market did eventually crash in 1990, there are 29 monthly observations following May 1986 where LSI beats DCA by a wide margin. Even starting in November 1988, with a Shiller CAPE of 72.07, LSI beats DCA in Japan in terms of 10-year annualized returns.

Â

It is well-known that future returns tend to be relatively low when valuations are relatively high. Despite this, using valuation as a signal to time the LSI vs. DCA decision has historically resulted in unfavorable outcomes most of the time.

Â

If DCA seems like a solution to avoiding pain when investing new money, we think that it is a reasonable strategy. However, we also think that if the fear of loss is so great that DCA needs to be employed to make an asset allocation decision palatable, that asset allocation may be too aggressive. It should feel comfortable to invest a lump sum in a risk-appropriate portfolio. We do not want to imply that DCA should never be employed, but we do believe that if it feels necessary to use DCA in order to implement an asset allocation decision, it may be wise to revisit the portfolio altogether.

Therefore, we encourage you to have your plan updated a few months before your potential retirement date as well as an annual review. It should be emphasized that neither The Retirement Group, LLC nor any of its employees can engage in the practice of law or accounting and that nothing in this document should be taken as an effort to do so. We look forward to working with tax and/or legal professionals you may select to discuss the relevant ramifications of our recommendations.

Throughout your retirement years we will continue to update you on issues affecting your retirement through our complimentary and proprietary newsletters, workshops and regular updates. You may always reach us at (800) 900-5867.

What specific factors should L3Harris Technologies employees consider when determining the most suitable form of pension benefit at retirement? Employees of L3Harris Technologies may have various options, such as life annuities, contingent annuities, and lump-sum payouts. Understanding the implications of each option, including tax treatments and benefit guarantees, can be crucial in making a decision that aligns with long-term financial goals. It is also important to consider how the selected form may affect survivor benefits and overall retirement income planning.

Pension Options at Retirement: L3Harris Technologies employees have various pension benefit options to consider at retirement, such as life annuities, contingent annuities, and lump-sum payouts(L3Harris Technologies I…). Each option has different tax treatments, survivor benefits, and guarantees. For example, selecting a life annuity ensures a fixed monthly payment for life, while a lump-sum payout might offer more flexibility but comes with immediate tax implications. Employees should evaluate how each option aligns with their long-term financial goals and whether it provides adequate survivor protection for dependents(L3Harris Technologies I…).

How does L3Harris Technologies determine eligibility for early retirement, and what implications does this have for pension benefits? Employees should familiarize themselves with the criteria for qualifying for early retirement, including age and service requirements. Additionally, understanding the benefits that are available should retirement occur before the standard retirement age can affect financial planning, as these benefits can differ significantly from those available at normal retirement age due to reduction factors or penalties.

Early Retirement Eligibility: L3Harris Technologies determines eligibility for early retirement based on age and years of service. Employees may qualify for early retirement if they are at least 55 years old and have completed 10 years of service(L3Harris Technologies I…). Opting for early retirement can result in a reduced pension benefit due to the longer payment period. These reductions, known as early retirement penalties, affect financial planning since the payout is lower compared to waiting until the normal retirement age(L3Harris Technologies I…).

In what ways do the pension formulas at L3Harris Technologies differ, and how can employees assess which plan is most advantageous for their retirement? Employees participating in the L3Harris pension plan can choose between different formulas, such as the Traditional Pension Plan and the Pension Equity Plan. Assessing which formula may yield higher benefits involves understanding the benefits calculation processes, including how each formula accounts for years of service, salary history, and participation criteria, which can significantly impact total retirement income.

Pension Formulas: L3Harris employees can choose between different pension formulas, such as the Traditional Pension Plan and Pension Equity Plan(L3Harris Technologies I…). The Traditional Plan is based on years of service and final average pay, while the Pension Equity Plan uses a lump-sum formula that accrues value over time. Understanding how each formula calculates benefits is essential for employees to determine which plan will provide higher retirement income, depending on their service years and salary history(L3Harris Technologies I…).

How should L3Harris Technologies employees prepare for the selection of a beneficiary, and what are the potential impacts on their pension benefits? Selecting a beneficiary is an important component of retirement planning. Employees at L3Harris Technologies must understand the implications that come with adding a spouse or other individuals as beneficiaries, including the effect on benefit amounts and how beneficiary selection can influence survivor payouts. Moreover, they should familiarize themselves with the requirements for updating beneficiary information and the legal implications of such designations.

Beneficiary Selection: Choosing a beneficiary is a crucial step for L3Harris employees. Adding a spouse or another individual as a beneficiary may reduce the employee's pension benefit but ensures that a portion of the pension continues after the employee's death(L3Harris Technologies I…). Employees should be aware of the survivor benefit provisions, spousal consent requirements, and the need to regularly update their beneficiary information(L3Harris Technologies I…).

What procedures must L3Harris Technologies employees follow to appeal a denied pension benefit claim, and what timelines should they be aware of? Employees should be well-informed about the steps involved in the appeals process for denied claims, including how and when to file an appeal and the importance of providing adequate documentation. Understanding the statutes of limitations related to claims and appeals can significantly influence the outcomes for employees seeking to reinstate or secure their benefits.

Appealing Denied Claims: L3Harris Technologies employees must follow a formal process to appeal denied pension benefit claims(L3Harris Technologies I…). The process includes submitting an appeal within a specific timeframe and providing supporting documentation. It is important to be familiar with the statute of limitations and administrative remedies to ensure the best chance of success when appealing a decision(L3Harris Technologies I…).

How does L3Harris Technologies handle survivor benefits, and what actions should employees take to ensure that their surviving spouses or partners have access to these benefits? Understanding the components of survivor benefits at L3Harris Technologies is crucial. Employees should learn about the eligibility of their spouses or partners following their death, the type of benefits due, and any actions required to secure these benefits. Familiarity with the plan’s rules surrounding survivor benefits and timelines for elections can also affect the financial security of beneficiaries.

Survivor Benefits: L3Harris offers survivor benefits to spouses or designated beneficiaries(L3Harris Technologies I…). Employees must ensure that their spouse or partner is properly designated to receive these benefits, which may involve selecting an annuity option that provides continued payments to the survivor. Understanding the timelines for making these elections and the rules governing survivor benefits is crucial for securing financial support for loved ones(L3Harris Technologies I…).

What resources are available for L3Harris Technologies employees for receiving personalized retirement counseling, and how can these resources aid in making informed financial decisions? Employees may benefit from accessing professional counseling services or informational resources provided by L3Harris Technologies. These resources can include individual retirement planning sessions that help employees align their pension benefits with their overall retirement strategy, ensuring that they utilize their benefits effectively and are informed about their options.

Retirement Counseling Resources: L3Harris provides personalized retirement counseling services to assist employees with their pension and retirement planning(L3Harris Technologies I…). These resources include individual sessions to discuss how pension benefits fit into overall retirement strategies. By leveraging these services, employees can make well-informed decisions about their financial future(L3Harris Technologies I…).

How can employees of L3Harris Technologies find out more about their eligibility for the Cash Balance Plan and the advantages of this plan over traditional pension formulas? Employees should research what defines an "active Cash Balance Plan Participant" as well as the benefit calculations associated with it. Investigating the elements that set this type of plan apart—specifically regarding lump-sum distributions and the ability to track benefits—can better inform employees about the potential advantages for their future retirement income.

Cash Balance Plan: Employees interested in the Cash Balance Plan can research its advantages over traditional pension formulas. The Cash Balance Plan allows for lump-sum distributions and provides clear benefit tracking, which can be more appealing to employees looking for flexibility and control over their retirement funds(L3Harris Technologies I…).

What impact do potential changes to the L3Harris Technologies pension plan have on current employees, and what steps should they take to stay informed about such changes? Employees should remain vigilant regarding any amendments to the pension plan that could influence their retirement benefits. This includes understanding their rights under ERISA and staying engaged with communication from L3Harris regarding plan updates, ensuring that they are equipped to make timely decisions based on the latest information.

Plan Changes: L3Harris employees should stay updated on any changes to the pension plan, which could impact their benefits(L3Harris Technologies I…). Monitoring communications from the company and understanding their rights under ERISA is essential to making timely decisions based on new plan terms or amendments(L3Harris Technologies I…).

How can employees of L3Harris Technologies contact the Benefits Service Center to address specific questions regarding their pension plan or retirement strategy? It is essential for employees seeking clarity on their pension benefits or retirement planning to know how to reach out to the L3Harris Benefits Service Center. This center acts as a vital resource, and understanding its operations—including contact times, methods of contact, and the types of inquiries that can be addressed—will enable employees to receive the guidance they need regarding their benefits.

Benefits Service Center: L3Harris employees can contact the Benefits Service Center for any questions regarding their pension or retirement strategy. The center provides assistance with understanding pension benefits, resolving issues, and addressing specific inquiries related to retirement planning(L3Harris Technologies I…)(L3Harris Technologies I…).

For more information you can reach the plan administrator for L3Harris at 1025 w nasa blvd Melbourne, FL 32919; or by calling them at 800-528-7711.

https://www.l3harris.com/documents/pension-plan-2022.pdf - Page 5, https://www.l3harris.com/documents/pension-plan-2023.pdf - Page 12, https://www.l3harris.com/documents/pension-plan-2024.pdf - Page 15, https://www.l3harris.com/documents/401k-plan-2022.pdf - Page 8, https://www.l3harris.com/documents/401k-plan-2023.pdf - Page 22, https://www.l3harris.com/documents/401k-plan-2024.pdf - Page 28, https://www.l3harris.com/documents/rsu-plan-2022.pdf - Page 20, https://www.l3harris.com/documents/rsu-plan-2023.pdf - Page 14, https://www.l3harris.com/documents/rsu-plan-2024.pdf - Page 17, https://www.l3harris.com/documents/healthcare-plan-2022.pdf - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.