New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Kimberly-Clark Employees: Estimating the Cost of College

Crude oil prices remain elevated and volatile, with annualized volatility around 80% and prices ranging between $50 and $120 per barrel over the past six months. Petrochemical inputs for plastics and packaging, service fleet fuel costs, and distribution energy create direct exposure to oil price swings for consumer product manufacturers. For Kimberly-Clark employees focused on long-term financial health, periods of oil-driven economic volatility reinforce the value of diversified strategies that account for how energy markets influence the broader investment landscape. Working with a financial advisor helps ensure that energy market uncertainty does not undermine your long-term retirement and financial goals.

It doesn’t take a degree in finance to see the cost of college continues to rise.

In its 2017 report, the College Board showed that public four-year institutions raised prices an average of 3.2% annually between the 2007-08 and 2017-18 school years. Put another way, a $5,000 education in 2007-08 would cost $6,851 in 2017-18.

For a few families, the lion’s share of education costs falls on parents and, in some cases, on grandparents. For our Kimberly-Clark clients who are parents you may already know, generally, the majority of families rely on a combination of scholarships, grants, financial aid, part-time jobs, and parent support to help pay the cost.

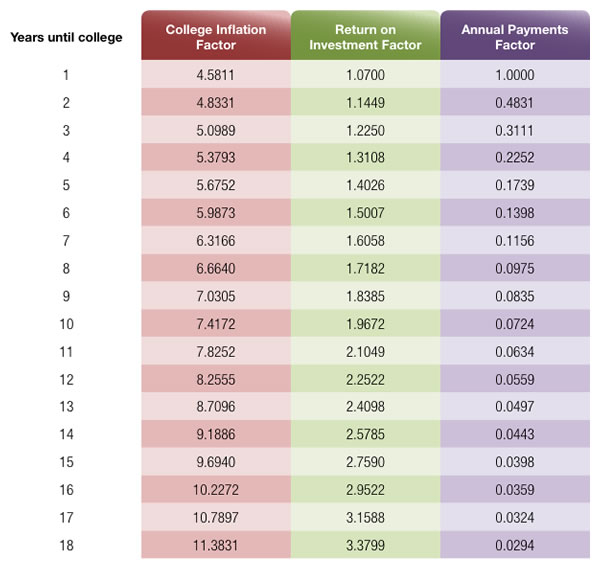

For Kimberly-Clark employees who have children approaching college age, a good first step is estimating the potential costs. The accompanying worksheet can help you get a better idea about the cost of a four-year college.

For Kimberly-Clark employees who already put money away for college, the worksheet will take that amount into consideration. For Kimberly-Clark employees who haven’t, it’s never too late to start.

Resources

There are a number of resources that can help individuals prepare for college. The U.S. government distributes certain information on colleges and costs. Here are two sites for these Kimberly-Clark employees to consider reviewing:

www.studentaid.ed.gov

The government’s college and financial aid portal.

www.collegeboard.org

The group that administers the SAT test.

Estimating the Cost of College

Before finalizing any estate plan, it is worth examining how Kimberly-Clark's employer-sponsored benefits fit into the broader picture. At the core of your retirement package, Kimberly-Clark maintains a defined benefit pension plan that has been frozen to new benefit accruals -- meaning the plan no longer accumulates future benefits for most employees, but those who were already vested may still be entitled to receive the pension benefit they accrued prior to the freeze, subject to the vesting requirements described in their plan documents, meaning the plan no longer accumulates future benefits for most employees, but those who were already vested may still be entitled to receive the pension benefit they accrued prior to the freeze, subject to the vesting requirements described in their plan documents. Kimberly-Clark also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension benefit, retiree healthcare eligibility, and any matching contributions depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with Kimberly-Clark's HR or benefits team for the most current details.

What is the 401(k) plan offered by Kimberly-Clark?

The 401(k) plan offered by Kimberly-Clark is a retirement savings plan that allows employees to save a portion of their paycheck before taxes are taken out.

How does Kimberly-Clark match employee contributions to the 401(k) plan?

Kimberly-Clark provides a matching contribution to the 401(k) plan, which typically matches a percentage of what employees contribute, up to a specified limit.

Can employees at Kimberly-Clark choose how their 401(k) contributions are invested?

Yes, employees at Kimberly-Clark can choose from a variety of investment options within the 401(k) plan to align with their retirement goals.

When can employees at Kimberly-Clark enroll in the 401(k) plan?

Employees at Kimberly-Clark can enroll in the 401(k) plan during their initial onboarding period or during designated open enrollment periods.

Is there a vesting schedule for Kimberly-Clark's 401(k) matching contributions?

Yes, Kimberly-Clark has a vesting schedule for matching contributions, meaning employees must work for the company for a certain period before they fully own the matched funds.

What is the maximum contribution limit for Kimberly-Clark's 401(k) plan?

The maximum contribution limit for Kimberly-Clark's 401(k) plan is subject to IRS regulations, which are updated annually. Employees should refer to the latest guidelines for specific limits.

Does Kimberly-Clark offer any financial education resources for employees regarding their 401(k)?

Yes, Kimberly-Clark provides financial education resources and tools to help employees make informed decisions about their 401(k) savings and investments.

Can employees take loans against their 401(k) savings at Kimberly-Clark?

Yes, Kimberly-Clark allows employees to take loans against their 401(k) savings, subject to specific terms and conditions outlined in the plan.

What happens to my 401(k) if I leave Kimberly-Clark?

If you leave Kimberly-Clark, you have several options for your 401(k), including rolling it over to another retirement account, cashing it out, or leaving it in the Kimberly-Clark plan if allowed.

How often can employees change their contribution amounts to the 401(k) at Kimberly-Clark?

Employees at Kimberly-Clark can typically change their contribution amounts to the 401(k) plan during designated enrollment periods or as specified by the plan guidelines.

For more information you can reach the plan administrator for Kimberly-Clark at 100 centurylink drive Monroe, LA 71203; or by calling them at 800-871-9244.

https://annualreport.stocklight.com/nyse/kmb/23601986.pdf - Page 5, https://www.kcpensions.co.uk/documents/kimberly-clark-pension-scheme-2022.pdf - Page 12, https://www.kcpensions.co.uk/documents/kimberly-clark-pension-scheme-2023.pdf - Page 15, https://www.kcpensions.co.uk/documents/kimberly-clark-pension-scheme-2024.pdf - Page 8, https://www.kimberly-clark.com/documents/benefits-guide-2023.pdf - Page 22, https://www.kimberly-clark.com/documents/benefits-guide-2024.pdf - Page 28, https://cache.hacontent.com/documents/kimberly-clark-retirement-guide-2022.pdf - Page 20, https://cache.hacontent.com/documents/kimberly-clark-retirement-guide-2023.pdf - Page 14, https://cache.hacontent.com/documents/kimberly-clark-retirement-guide-2024.pdf - Page 17, https://www.kimberly-clark.com/documents/healthcare-plan-2023.pdf - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.