New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for Abbott Laboratories Employees and Retirees

/General/General%2012.png?width=1280&height=853&name=General%2012.png)

With crude oil volatility near 80% and prices spanning $50 to $120 per barrel over the past six months, energy cost uncertainty influences economic conditions across industries. Petrochemical inputs for pharmaceutical production and cold-chain distribution logistics create tangible cost pressure when crude prices remain elevated. For Abbott Laboratories employees building retirement savings, oil-driven inflation and market volatility make disciplined saving and diversified allocation more important, as energy cycles can disrupt both portfolio values and purchasing power. Professional guidance can help you navigate the indirect effects of oil volatility on your retirement planning and ensure your strategy accounts for these dynamics.

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

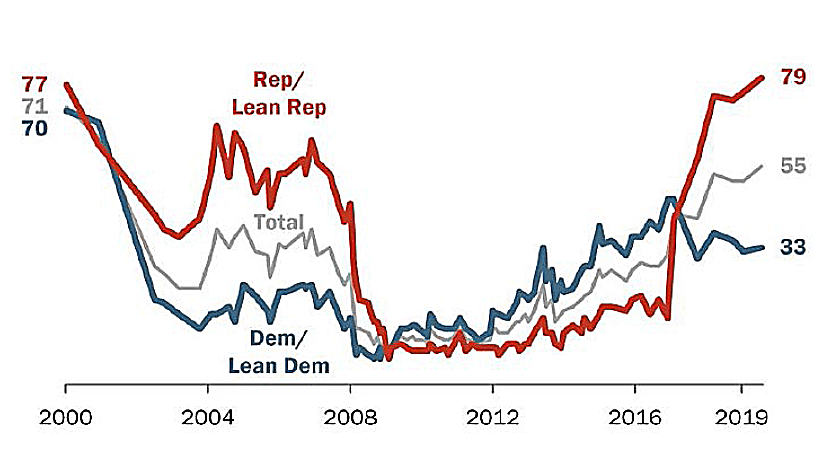

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how Abbott Laboratories's employer-sponsored benefits fit into the broader picture. According to publicly available information, Abbott Laboratories maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. Abbott Laboratories does not appear to offer a formal retiree healthcare program, making healthcare coverage planning an important consideration if you retire before age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with Abbott Laboratories's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

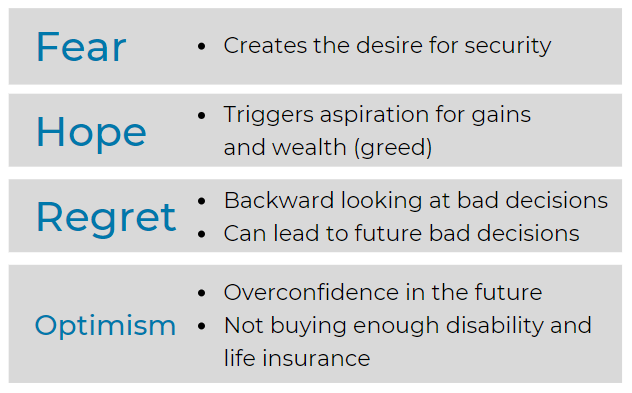

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

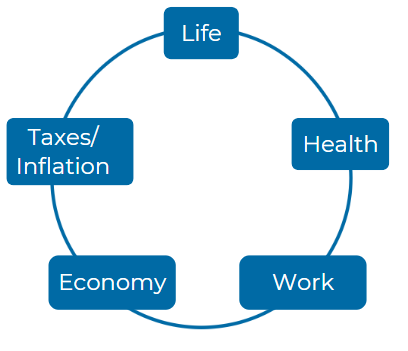

Consider these five Elements:

Â

Â

How does the Abbott Laboratories Annuity Retirement Plan (ARP) determine the eligibility requirements for employees, and how can potential changes in federal regulations impact these requirements? Employees of Abbott Laboratories may need to understand the nuances of eligibility, particularly regarding age and service criteria. Changes in laws governing retirement benefits could pose questions about continued eligibility and could affect when employees can begin pension payments.

Eligibility Requirements & Impact of Federal Regulations: Employees at Abbott Laboratories become eligible for the ARP by being part of a participating division, being at least 21 years old, and residing in the U.S. (with certain exceptions for U.S. employees abroad). Changes in federal regulations could potentially alter these eligibility criteria, especially since such rules often influence age and service requirements for retirement plans. Any changes in legislation regarding retirement benefits might necessitate adjustments in eligibility rules, affecting when employees can begin receiving pension payments.

Can you explain the significance of Vesting Service in the context of the Abbott Laboratories Annuity Retirement Plan? Employees often wonder how their years of service influence their benefit eligibility and the amount they can expect. Understanding the elements that constitute Vesting Service, and the implications of terminating employment before achieving vesting, is crucial for Abbott Laboratories employees planning for retirement.

Significance of Vesting Service: Vesting Service at Abbott Laboratories refers to the time an employee must accumulate to gain entitlement to pension benefits, irrespective of continued employment. This service is critical as it determines the security of an employee's future benefits and the degree of an employee's investment in the company's pension plan. Employees who terminate employment prior to achieving full vesting lose entitlement to accrued pension benefits, making understanding and accruing Vesting Service essential for long-term financial planning.

In what ways does the calculation of Final Average Pay play a role in determining retirement benefits under the Abbott Laboratories Annuity Retirement Plan? The methodology used to calculate an employee's Final Average Pay can significantly impact the retirement income they receive. Employees at Abbott Laboratories should consider how their earnings history and the inclusion or exclusion of certain payments factor into their anticipated benefits.

Role of Final Average Pay in Benefit Calculation: Final Average Pay (FAP) is crucial in determining the pension benefits under the ARP as it represents the average of an employee’s highest earnings over a specified period. Abbott’s ARP calculates pension based on a percentage of the FAP, multiplied by years of eligible service. This calculation means that higher earnings towards the end of an employee's career can significantly increase the pension benefits, incentivizing employees to maximize their earnings potential in their final working years.

What optional forms of payment are available to employees upon retirement under the Abbott Laboratories Annuity Retirement Plan, and how do these choices affect overall pension benefits? Abbott Laboratories employees need to evaluate whether to choose single or joint survivor annuities, among other options, as these decisions can have long-term financial implications for both themselves and their beneficiaries.

Optional Forms of Payment at Retirement: The ARP offers various payment options upon retirement, including single and joint survivor annuities, which affect the benefit's distribution and longevity. These choices impact financial planning for retirement, particularly in ensuring that a spouse or beneficiary may continue to receive benefits after the retiree's death. The selection between these options should align with personal financial needs and considerations for dependents' security.

Different employees may have varying perspectives on the importance of early retirement options offered by Abbott Laboratories. What are the qualifications for early special retirement, and how does this option affect retirement income? Employees contemplating retirement before the standard age should understand how factors such as age, years of service, and the specific provisions of the Abbott Laboratories Annuity Retirement Plan influence their benefits.

Early Retirement Qualifications and Impacts: Early retirement under the ARP is available to employees who meet specific age and service criteria, allowing them to retire with reduced benefits before reaching the normal retirement age. This option can significantly affect retirement income, depending on the number of years ahead of normal retirement age the employee chooses to retire, making it crucial for employees to understand the financial trade-offs involved in retiring early.

How does the Abbott Laboratories Annuity Retirement Plan ensure compliance with the Employee Retirement Income Security Act (ERISA), and what rights do employees have under this act? Abbott Laboratories employees should be informed about their rights regarding plan documentation, required disclosures, and recourse in the event of disputes pertaining to their retirement benefits.

ARP Compliance with ERISA: The ARP is designed to comply with the Employee Retirement Income Security Act (ERISA), providing employees with rights to information about plan features and funding, benefits accrual, and recourse in case of disputes. Compliance with ERISA ensures that employees' retirement benefits are protected under federal law, offering a framework for security and transparency in their retirement planning.

How do Abbott Laboratories employees who experience a medical leave of absence or disability maintain their retirement service credits under the Annuity Retirement Plan? Understanding the interaction between long-term disability benefits, medical leave, and retirement plan participation is essential for employees navigating health-related issues while planning for their retirement.

Impact of Medical Leave or Disability on Retirement Credits: Employees on medical leave or disability continue to accrue service credits under the ARP, ensuring that such periods do not adversely affect their pension benefits. This protection helps employees who are temporarily unable to work due to health issues maintain their trajectory towards earning full retirement benefits.

Given the potential for changes to the Abbott Laboratories Annuity Retirement Plan, how can employees stay informed about their rights and any modifications to the plan’s terms? Employees at Abbott Laboratories should have access to reliable communication channels, including how to receive updates about the retirement plan, which could impact their financial planning.

Staying Informed About Plan Changes: Employees can stay informed about changes to the ARP through regular communications from Abbott Laboratories, access to updated plan documents, and direct inquiries to the Abbott Benefits Center. Staying proactive in seeking information and understanding the implications of plan modifications is essential for effective retirement planning.

What processes should Abbott Laboratories employees follow if they wish to obtain a statement regarding their entitlement to a pension? Employees looking to plan for retirement need clear instructions on how to request this crucial information and understand its importance in their long-term financial strategy.

Obtaining a Pension Statement: Employees wishing to obtain a statement of their pension entitlements under the ARP should contact the Abbott Benefits Center. Clear instructions on how to request this information are crucial for employees to plan accurately for retirement and understand their accrued benefits.

If an employee at Abbott Laboratories has further questions about the Annuity Retirement Plan or requires clarification on the document contents, how can they effectively contact the appropriate department? Knowing how to reach out to Abbott Laboratories' Benefits Center regarding retirement plan inquiries is vital for all employees wanting to confirm their understanding or seek additional information about their retirement benefits.

Contacting the Appropriate Department for Plan Inquiries: For further inquiries or clarification regarding the ARP, employees should contact the Abbott Benefits Center. Knowing the correct contact information and how to reach out effectively is vital for resolving concerns and gaining a deeper understanding of their retirement benefits.

For more information you can reach the plan administrator for Abbott Laboratories at 1295 state street Springfield, MA 1111; or by calling them at 1-866-329-6277.

https://cache.hacontent.com/ybr/R516/00472_ybr_ybrfndt/downloads/EmpHandbook.pdf - Page 12,https://abbottbenefits.com/wp-content/uploads/BenefitsHighlightsGuide_2024.pdf - Page 7,https://cache.hacontent.com/ybr/R516/00472_ybr_ybrfndt/downloads/RetirementGuide2023.pdf - Page 22,https://cache.hacontent.com/ybr/R516/00472_ybr_ybrfndt/downloads/HealthcareOptions2024.pdf - Page 19,https://abbottbenefits.com/wp-content/uploads/2023/01/BenefitsHighlightsGuide_2023.pdf - Page 14,https://abbottbenefits.com/wp-content/uploads/2022/05/BenefitsHighlightsGuide_2022.pdf - Page 8,https://cache.hacontent.com/ybr/R516/00472_ybr_ybrfndt/downloads/AbbottAnnuityRetirementPlan.pdf - Page 11,https://cache.hacontent.com/ybr/R516/00472_ybr_ybrfndt/downloads/AbbottAbbVieMEPP.pdf - Page 25,https://abbottbenefits.com/wp-content/uploads/2024/02/BenefitsCenterGuide.pdf - Page 16,https://www.abbott.com/content/dam/abbott/en-us/documents/pdfs/annual-report-2023.pdf - Page 55

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.