New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for Aetna Employees and Retirees

Oil market turbulence continues to ripple through the broader economy, with crude swinging between $50 and $120 per barrel and annualized volatility near 80%. Energy price swings affect insurer investment portfolios and the broader economic conditions that drive policy demand and claims patterns. For Aetna employees building retirement savings, oil-driven inflation and market volatility make disciplined saving and diversified allocation more important, as energy cycles can disrupt both portfolio values and purchasing power. Working with a financial advisor helps ensure that energy market uncertainty does not undermine your long-term retirement and financial goals.

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

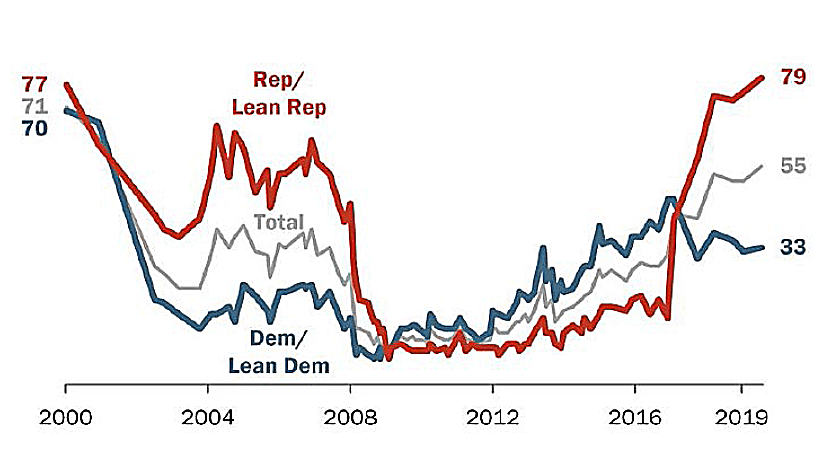

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how Aetna's employer-sponsored benefits fit into the broader picture. According to publicly available information, Aetna maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. Aetna also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with Aetna's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

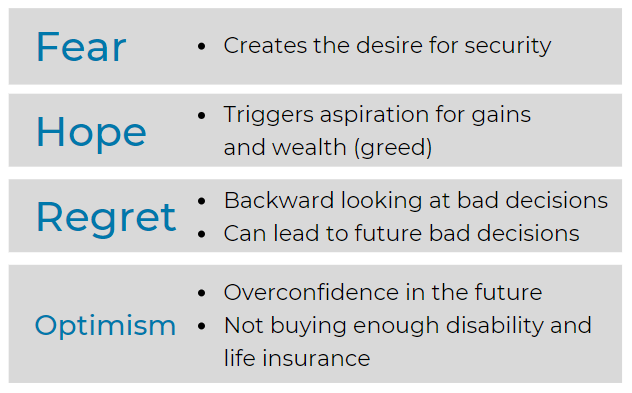

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

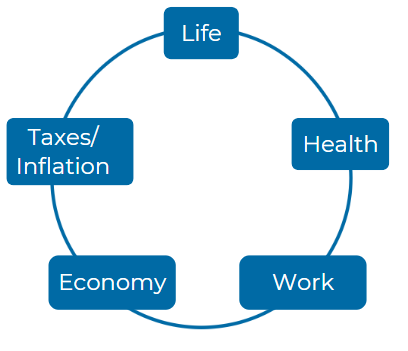

Consider these five Elements:

Â

Â

How does Aetna Inc.'s frozen pension plan affect employees' eligibility for benefits, and what specific criteria must current employees meet to qualify for any benefits from the Retirement Plan for Employees of Aetna Inc.?

Eligibility for Benefits: Aetna Inc.'s pension plan has been frozen since January 1, 2011, meaning no new pension credits are accruing. Employees who were participants before this date remain eligible for benefits but cannot accrue additional pension credits. To qualify for benefits, participants need to have been vested, which generally occurs after three years of service(PensionSPD).

In what ways can employees at Aetna Inc. transition their pension benefits if they leave the company, and what implications does this have for their tax liabilities and retirement planning?

Transitioning Pension Benefits: If employees leave Aetna, they can opt for a lump-sum distribution or an annuity. Employees can roll over their lump-sum payments into an IRA or other tax-qualified plans to avoid immediate taxes. However, direct rollovers must follow the tax-qualified plan's rules. If not rolled over, employees are subject to immediate tax and potential penalties(PensionSPD).

What steps should an Aetna Inc. employee take if they become disabled and wish to continue receiving pension benefits, and how does the company's policy on disability impact their future retirement options?

Disability and Pension Benefits: Employees who become totally disabled and qualify for long-term disability can continue participating in the pension plan until their disability benefits cease or employment is terminated. No additional pension benefits accrue after December 31, 2010, but participation continues under the plan until employment formally ends(PensionSPD).

Can you explain the implications of the plan amendment rights that Aetna Inc. retains, particularly concerning any potential changes in the pension benefits and what this could mean for employee planning?

Plan Amendment Rights: Aetna reserves the right to amend or terminate the pension plan at any time. If the plan is terminated, participants will still receive benefits accrued up to the date of termination, protected by ERISA. Any future changes could impact employees' planning and retirement options(PensionSPD).

How does the IRS's annual contribution limits for pension plans in 2024 interact with the provisions of the Retirement Plan for Employees of Aetna Inc., and what considerations should employees keep in mind when planning their retirement contributions?

IRS Contribution Limits: The IRS sets annual contribution limits for pension plans, including defined benefit plans. In 2024, employees should ensure that their pension contributions and tax planning strategies align with these limits and the provisions of Aetna's pension plan(PensionSPD).

What are the options available to Aetna Inc. employees regarding pension benefit withdrawal, and how can they strategically choose between a lump-sum distribution versus an annuity option?

Withdrawal Options: Aetna employees can choose between a lump-sum distribution or various annuity options when withdrawing pension benefits. The lump-sum option allows for immediate access to funds, while annuities provide monthly payments over time, offering a more stable income stream(PensionSPD).

How does Aetna Inc. ensure compliance with ERISA regulations concerning the rights of employees in the retirement plan, and what resources are available for employees to understand their rights and claims procedures?

ERISA Compliance: Aetna complies with ERISA regulations, ensuring employees' rights are protected. Resources are available through the Plan Administrator and myHR, providing information on claims procedures, plan rights, and how to file appeals if necessary(PensionSPD).

What documentation should employees of Aetna Inc. be aware of when applying for their pension benefits, and how can they ensure that they maximize their benefits based on their years of service?

Documentation for Benefits: Employees should retain service records and review their benefit statements to ensure they receive the maximum pension benefits. They can request additional documents and assistance through myHR to verify their years of service and other relevant criteria(PensionSPD).

How do changes in interest rates throughout the years affect the annuity payments that employees at Aetna Inc. might receive upon retirement, and what strategies can they consider to optimize their retirement income?

Impact of Interest Rates on Annuities: Interest rates significantly affect annuity payments. Higher interest rates increase the monthly annuity amount. Employees should consider the timing of their retirement, especially at the end of the year, when interest rates for the following year are announced(PensionSPD).

If employees want to learn more about their pension options or have inquiries regarding the Retirement Plan for Employees of Aetna Inc., what are the best channels to contact the company, and what specific resources does Aetna provide for assistance?

Contact for Pension Inquiries: Employees can contact myHR at 1-888-MY-HR-CVS (1-888-694-7287), selecting the pension menu option for assistance. Aetna also provides detailed resources through the myHR website, helping employees understand their pension options and benefits(PensionSPD).

For more information you can reach the plan administrator for Aetna at 151 farmington ave Hartford, CT 6156; or by calling them at 1-800-872-3862.

https://www.aetnaretirees.com/Documents/2022_Retiree_Resource_Guide.pdf - Page 8, https://www.benefitsaccountmanager.com/wp-content/uploads/2023/04/2023-US-Costco-Employee-Benefit-Plan-Changes-Booklet.pdf - Page 12, https://emeriti.aetnamedicare.com/2023-aetna-plus-ppo-plan-benefits.pdf - Page 15, https://www.opm.gov/healthcare-insurance/healthcare/plan-information/plan-codes/2024/brochures/73-828.pdf - Page 22, https://www.mynavyexchange.com/assets/Static/ARC/2024-Benefits-Enrollment-Guide.pdf - Page 18, https://mcforms.mayo.edu/mc1000-mc1099/mc1034-43.pdf - Page 20, https://www.aetnaretirees.com/Documents/Aetna_Medicare_Advantage_Plan_2023.pdf - Page 14, https://www.aetnaretirees.com/Documents/2024_Aetna_PPO_Plan.pdf - Page 28, https://www.aetnaretirees.com/Documents/2023_Aetna_Employee_Benefits.pdf - Page 17, https://www.aetnaretirees.com/Documents/2022_Aetna_Health_Insurance.pdf - Page 11

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.