New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for Caterpillar Employees and Retirees

/General/General%2013.png?width=1280&height=853&name=General%2013.png)

Energy market instability persists, with crude prices fluctuating between $50 and $120 per barrel and annualized volatility running around 80%. The effects reach well beyond the energy sector. Diesel fuel for heavy equipment fleets, steel and component transport costs, and energy-intensive fabrication processes create substantial direct oil price exposure for heavy machinery and equipment manufacturers. Retirement savings strategies at Caterpillar should account for how energy price cycles influence inflation, interest rates, and market returns over the long horizons that retirement planning requires. Working with a financial advisor can help you position your planning strategy for sustained energy price uncertainty.

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

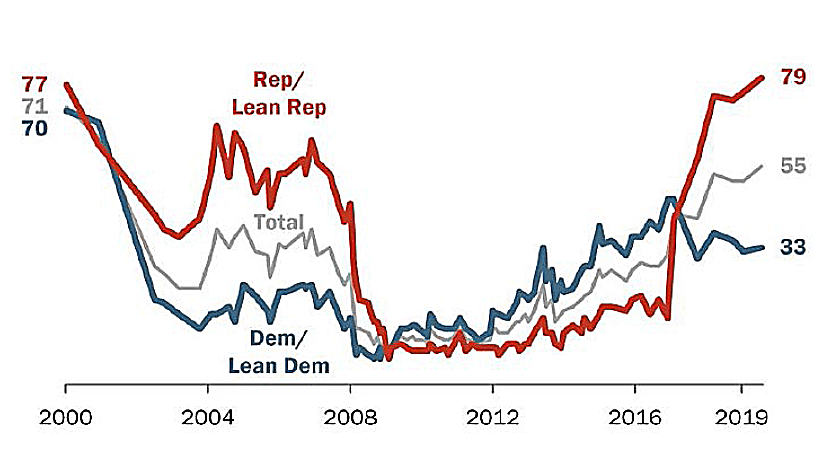

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how Caterpillar's employer-sponsored benefits fit into the broader picture. It is important to note that Caterpillar maintains a defined benefit pension plan that has been frozen to new benefit accruals -- meaning the plan no longer accumulates future benefits for most employees, but those who were already vested may still be entitled to receive the pension benefit they accrued prior to the freeze, subject to the vesting requirements described in their plan documents - this means the plan no longer accumulates future benefits for most employees, but those who were already vested may still be entitled to receive the pension benefit they accrued prior to the freeze, subject to the vesting requirements described in their plan documents. Caterpillar also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension benefit, retiree healthcare eligibility, and any matching contributions depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with Caterpillar's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

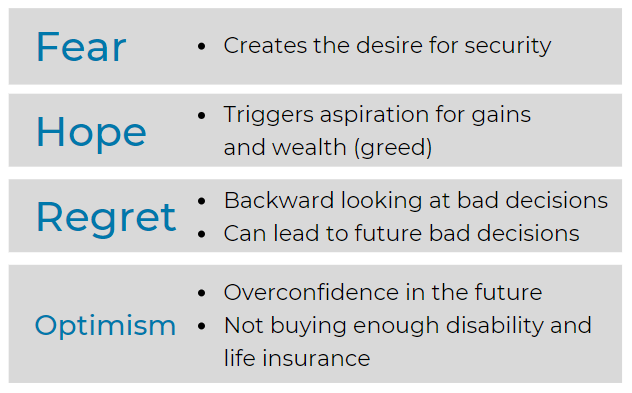

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

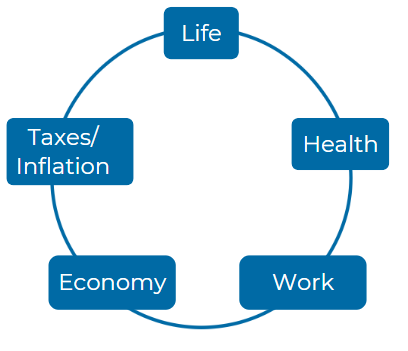

Consider these five Elements:

Â

Â

How does the transition from the Solar Plan to the Caterpillar Inc. Retirement Income Plan impact current or former employees of Caterpillar Inc. in terms of retirement benefits and service credits? Considering both plans' differences, what aspects should employees of Caterpillar Inc. understand to ensure they are maximizing their retirement benefits under this merged structure?

Transition from Solar Plan to Caterpillar Inc. Retirement Income Plan: The transition from the Solar Plan to the Caterpillar Inc. Retirement Income Plan maintained the benefits of those previously covered under the Solar Plan without impact. Both plans allowed the continuation of prior service credits and the incorporation of benefits payable under previous retirement plans. For current or former employees, understanding the nuances of how prior service credits and benefits are integrated can maximize their retirement benefits under the merged structure.

What specific criteria must Caterpillar Inc. employees meet to qualify for early retirement and what implications does this have on their pension benefits? For employees planning early retirement, what calculations or benefit reductions should they be prepared for according to Caterpillar Inc.’s policies?

Criteria for Early Retirement at Caterpillar Inc.: Employees wishing to take early retirement must meet specific age and service requirements detailed in the plan documents. For early retirement, benefits calculations and potential reductions are significant. Employees need to prepare for possible reductions in their pension benefits depending on their age and years of credited service at retirement.

In the context of the Pension Equity Plan (PEP) and the Traditional Pension Plan, how do the benefit calculations differ for employees at Caterpillar Inc., particularly for those who switched from the Traditional Plan to the PEP? What considerations should current Caterpillar Inc. employees take into account when evaluating which plan may offer them more secure benefits?

Differences Between PEP and Traditional Pension Plan: The benefit calculations for the Pension Equity Plan (PEP) and the Traditional Pension Plan differ significantly. PEP calculates a lump sum based on salary and years of service, while the Traditional Plan calculates benefits based on final earnings or credited service formulas. Employees need to consider which plan offers more secure benefits based on their individual career trajectory and earnings history.

What steps must Caterpillar Inc. employees take to ensure that their Credited Service is accurately calculated and maintained throughout their employment, especially in light of the company's policies regarding breaks in service? How might phases of employment, such as parental leave or temporary positions, affect this calculation?

Credited Service Calculation and Maintenance: To ensure accurate credited service calculation, employees must maintain thorough records and communicate any changes in employment status, such as breaks in service or changes in personal information, to the plan administrator. Understanding the rules for service credits during different phases of employment, such as parental leave or temporary positions, is crucial.

How can employees at Caterpillar Inc. file a claim for benefits under the retirement plans, and what are the essential details they need to provide to ensure their claims are processed smoothly? If they encounter issues or denials, what recourse do they have within the Caterpillar Inc. system to appeal these decisions?

Filing a Claim for Benefits: Employees should provide detailed and accurate information when filing a claim for benefits under the retirement plans. If issues or denials occur, they have the right to appeal these decisions. Familiarity with the claims procedure and required documentation can streamline this process.

For employees approaching retirement, what resources are available through Caterpillar Inc. to help them navigate the complexities of their retirement benefits? What steps should an employee take if they wish to understand their benefits better or need assistance with retirement planning?

Resources for Navigating Retirement Benefits: Caterpillar Inc. offers resources to assist employees in navigating the complexities of their retirement benefits. Employees approaching retirement should utilize these resources and may need to engage with the company's human resources or benefits departments for personalized assistance.

What are the implications of the changes to the cash-out limit for de minimis benefits at Caterpillar Inc., which will take effect after December 31, 2023? How does this change affect employees who may have a vested interest in understanding their financial benefit options upon termination or retirement?

Implications of Cash-Out Limit Changes: The increase in the cash-out limit for de minimis benefits affects how small vested benefits are processed upon termination or retirement. Employees with small benefit amounts should understand how these changes may impact their options and tax implications.

How does Caterpillar Inc. ensure that its pension benefits are protected from creditors, and what specific provisions exist to safeguard these benefits? Moreover, how do legal instruments like Qualified Domestic Relations Orders (QDROs) interact with Caterpillar Inc.'s benefits system for employees undergoing divorce?

Protection of Pension Benefits from Creditors: Caterpillar Inc.'s retirement plans are designed with protections to safeguard benefits from creditors, including adherence to Qualified Domestic Relations Orders (QDROs) during instances like divorce. Employees should understand how these legal instruments can affect their retirement savings.

In what ways does the Caterpillar Inc. Retirement Income Plan provide coverage for disability retirement, and how is this benefit calculated for employees? What factors influence eligibility and how do employees initiate claims if they find themselves in need of these benefits?

Disability Retirement Coverage: The plan provides specific provisions for disability retirement, including how benefits are calculated and eligibility criteria. Employees should be aware of how disability affects their benefits and the process for initiating claims if needed.

How can Caterpillar Inc. employees contact the company to learn more about their retirement benefits, and what information should they have ready when making inquiries? Additionally, what specific departments at Caterpillar Inc. should employees reach out to for the most efficient assistance regarding their retirement plan questions?

Contacting the Company for Retirement Benefit Information: Employees can contact the Caterpillar Benefits Center for inquiries about their retirement benefits. Knowing the specific departments to contact for efficient assistance is crucial for addressing concerns and making informed decisions about retirement planning.

For more information you can reach the plan administrator for Caterpillar at 510 lake cook rd Deerfield, IL 60015; or by calling them at 224-551-400.

https://cache.hacontent.com/ybr/R516/02358_ybr_ybrfndt/downloads/UAW_SPD.pdf - Page 7, https://www.mycatpension.co.uk/uploads/documents/00/00/01/71/documentdocument_file/caterpillar-db-newsletter-2024.pdf - Page 9, https://benefits.cat.com/content/dam/benefits/PDF%20Documents/2023-ae/HR-Benefits_Enrollment-2023-Employee-web_FINAL.pdf - Page 12, https://benefits.cat.com/content/dam/benefits/PDF%20Documents/HR-BenefitsEnrollment-2022-Retiree-Final-111621-LR.pdf - Page 14, https://www.mycatpension.co.uk/uploads/documents/00/00/01/47/documentdocument_file/caterpillar-db-newsletter-2023.pdf - Page 16, https://www.mycatpension.co.uk/Uploads/Documents/00/00/01/72/DocumentDocument_FILE/Caterpillar-DC-newsletter-2024.pdf - Page 20, https://cache.hacontent.com/ybr/R516/02358_ybr_ybrfndt/downloads/RIP_AFN.pdf - Page 11, https://s25.q4cdn.com/358376879/files/doc_presentations/2024/2023-Caterpillar-Investor-Presentation.pdf - Page 18, https://www.mycatpension.co.uk/Uploads/Documents/00/00/01/69/DocumentDocument_FILE/Caterpillar-DC-Pension-Plan-2023-Chair-s-Statement.pdf - Page 22, https://cache.hacontent.com/ybr/R516/02358_ybr_ybrfndt/downloads/SPDDB2VR.pdf - Page 24

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.