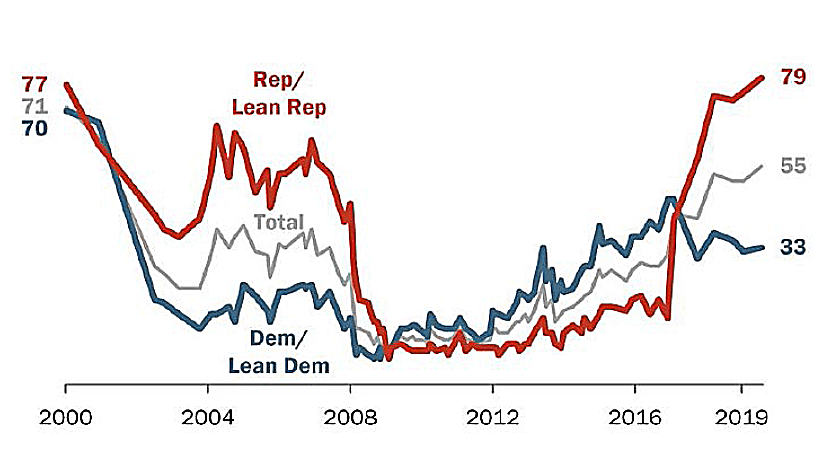

New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for Chevron Employees and Retirees

/General/General%207.png?width=1280&height=853&name=General%207.png)

Annualized crude volatility around 80% and a $50 to $120 trading range create a complex picture for Chevron. As an integrated operator, the company benefits from high crude through its upstream segment while managing procurement costs in refining and leveraging midstream fee contracts for stability. This multi-segment exposure means no single oil price direction is purely good or bad for the company's overall financial health. Building retirement security at Chevron requires recognizing that savings contributions, equity compensation values, and even job stability can move with crude oil, making diversification beyond employer stock essential. Given this uncertainty, a financial advisor who understands energy sector dynamics can help you position your financial plan for long-term success regardless of oil price direction.

Â

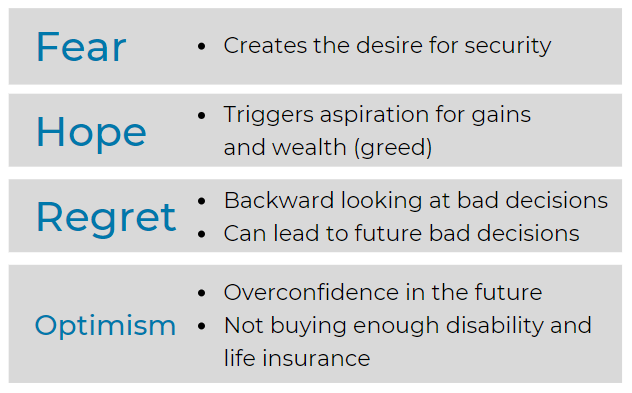

Financial Decision-making in Extremely Uncertain Times

Â

Emotional Intelligence Development and Maintenance

Â

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how Chevron's employer-sponsored benefits fit into the broader picture. According to publicly available information, Chevron maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. Chevron also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with Chevron's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

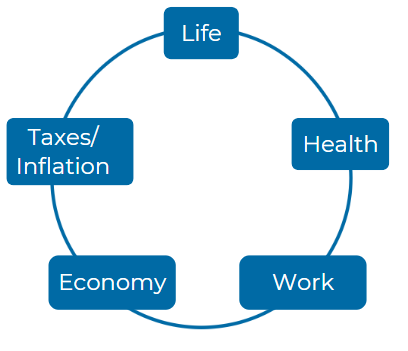

Consider these five Elements:

Â

Â

How does Chevron Phillips Chemical determine an employee's eligibility for retirement benefits, and what factors contribute to this determination? In your response, consider aspects such as age, years of service, and any specific milestones that the company factors into its retirement policy.

Eligibility for Retirement Benefits: Employees of Chevron Phillips Chemical become eligible for retirement benefits if they are regular employees scheduled to work at least 20 hours per week. Eligibility starts from the first day of employment. Retirement benefits accrue based on factors including age, years of service, and specific milestones like reaching Normal Retirement Age, which is age 65 or completion of three years of Vesting Service, whichever is later.

What are the various payment options available to employees when they retire from Chevron Phillips Chemical, and how do these options cater to different financial needs? Discuss the implications of choosing an annuity versus a lump-sum payment and the impact these decisions may have on an employee's financial planning during retirement.

Payment Options Available at Retirement: Chevron Phillips Chemical offers various payment options for retirement benefits, including lifetime monthly annuities and lump-sum payments. The choice between these options affects financial planning, as annuities provide a steady income while a lump-sum can be invested differently but comes with different tax implications and management responsibilities.

In the event of untimely death before retirement, what retirement benefits are available to the surviving spouse or beneficiaries of a Chevron Phillips Chemical employee? Explain the conditions under which these benefits are payable and how they align with the company’s policy objectives for retirement planning.

Benefits for Surviving Spouses or Beneficiaries: In the event of an employee's untimely death before retirement, the surviving spouse or beneficiaries are eligible for benefits under the terms of the plan. The company provides options for continued income for a spouse or other beneficiary, ensuring financial support aligns with the company’s policy objectives for family protection and retirement planning.

Chevron Phillips Chemical employees often face questions regarding early retirement. What criteria must be met to qualify for early retirement benefits, and how does the early retirement factor affect the overall benefit amount? Delve into the calculations and adjustments made for employees who opt for early retirement.

Early Retirement Criteria and Benefits: To qualify for early retirement, Chevron Phillips Chemical employees must be at least 55 years old with 10 years of Vesting Service or have completed 25 years of Vesting Service regardless of age. Early retirement benefits are adjusted based on the age at retirement and the distance from Normal Retirement Age, with specific reductions applied for each year benefits are taken before age 62.

As employees approach retirement age, understanding the process and necessary steps to receive retirement benefits is crucial. Can you outline the application process for claiming retirement benefits at Chevron Phillips Chemical, including key timelines and documentation required from employees?

Application Process for Retirement Benefits: The process for claiming retirement benefits involves contacting the Chevron Phillips Pension and Savings Service Center or accessing the Fidelity NetBenefits website. Key timelines include submitting an application 30 to 180 days before the desired retirement date, with required documentation such as employment verification and personal identification.

The retirement benefits at Chevron Phillips Chemical appear complex and multifaceted. How does the company ensure employees understand their retirement planning options, and what resources are available for employees to seek assistance or clarification about their retirement plans?

Understanding Retirement Planning Options: Chevron Phillips Chemical ensures that employees understand their retirement planning options through resources like the company’s benefits website, informational sessions, and one-on-one consultations with benefits advisors. This support helps employees make informed decisions about their retirement options.

How does the Chevron Phillips Chemical retirement plan integrate with Social Security benefits, and what considerations should employees bear in mind when planning their overall retirement income strategy? Discuss any supplemental benefits or adjustments available for employees who want to maximize their retirement income.

Integration with Social Security Benefits: The retirement plan is designed to complement Social Security benefits, which employees need to consider in their overall retirement income strategy. The plan may include supplemental benefits that adjust based on Social Security payouts, offering a coordinated approach to maximize retirement income.

Considering the varying forms of benefits accrued over years of service, how does Chevron Phillips Chemical calculate final retirement benefits? Focus on the role of eligible compensation and service time in determining the overall benefit, including specific formulas or examples that illustrate this processing.

Calculation of Final Retirement Benefits: Final retirement benefits at Chevron Phillips Chemical are calculated based on eligible compensation and years of Benefit Service. The plan includes formulas like the Stable Value Formula and the Traditional Retirement Plan Formula, which consider different elements of compensation and service duration.

What is the policy of Chevron Phillips Chemical regarding vesting service, and how does it impact employees' rights to their retirement benefits? Elaborate on the significance of vesting service in the broader context of employee retention and long-term planning.

Policy on Vesting Service: Vesting Service at Chevron Phillips Chemical is crucial for establishing an employee’s right to retirement benefits. Employees are vested after three years of service, which grants them a nonforfeitable right to benefits accrued up to that point, enhancing retention and long-term financial security.

For employees seeking additional information about their retirement plans or benefits, what is the most effective way to contact Chevron Phillips Chemical? Identify the channels through which employees can obtain further assistance and clarify whom they should reach out to for specific queries related to their retirement planning documentation.

Contact Channels for Further Information: Employees seeking more information about their retirement plans or needing specific assistance can contact the Chevron Phillips Pension and Savings Service Center. This center provides detailed support and access to personal benefit information, facilitating effective retirement planning.

For more information you can reach the plan administrator for Chevron at 6001 bollinger canyon road San Ramon, CA 94583; or by calling them at 713-372-4335.

https://hr2.chevron.com/-/media/hr2/docs/Chevron-2022-Wealth-Benefits.pdf - Page 7, https://hr2.chevron.com/-/media/hr2/docs/Chevron-2023-Wealth-Benefits.pdf - Page 12, https://hr2.chevron.com/-/media/hr2/docs/Chevron-2024-Wealth-Benefits.pdf - Page 15, https://www.chevron.com/-/media/chevron/annual-report/2022/documents/2022-Annual-Report.pdf - Page 8, https://chevron.pensioncharges.com/docs/Chevron-UK-Pension-Plan-2022.pdf - Page 22, https://chevron.pensioncharges.com/docs/Chevron-UK-Pension-Plan-2023.pdf - Page 28, https://hr2.chevron.com/-/media/hr2/docs/Chevron-Employee-Handbook-2023.pdf - Page 20, https://hr2.chevron.com/-/media/hr2/docs/Chevron-Retirement-Plan-2024.pdf - Page 14, https://hr2.chevron.com/-/media/hr2/docs/Chevron-Savings-Investment-Plan-2024.pdf - Page 17, https://hr2.chevron.com/-/media/hr2/docs/Chevron-Health-Benefits-Guide-2024.pdf - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.