New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for Kraft Employees and Retirees

/General/General%205.png?width=1280&height=853&name=General%205.png)

Oil market turbulence continues to ripple through the broader economy, with crude swinging between $50 and $120 per barrel and annualized volatility near 80%. Petroleum-derived fertilizer costs, packaging materials, and refrigerated logistics connect food and beverage companies directly to crude oil price movements. Retirement savings strategies at Kraft should account for how energy price cycles influence inflation, interest rates, and market returns over the long horizons that retirement planning requires. Consulting with a financial advisor can help you understand how energy conditions affect your specific situation and build a plan that adapts accordingly.

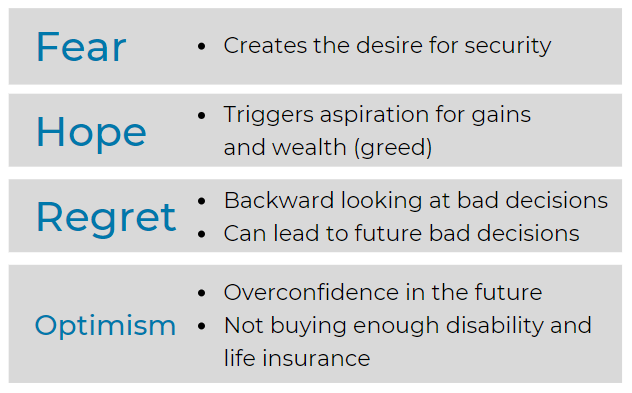

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

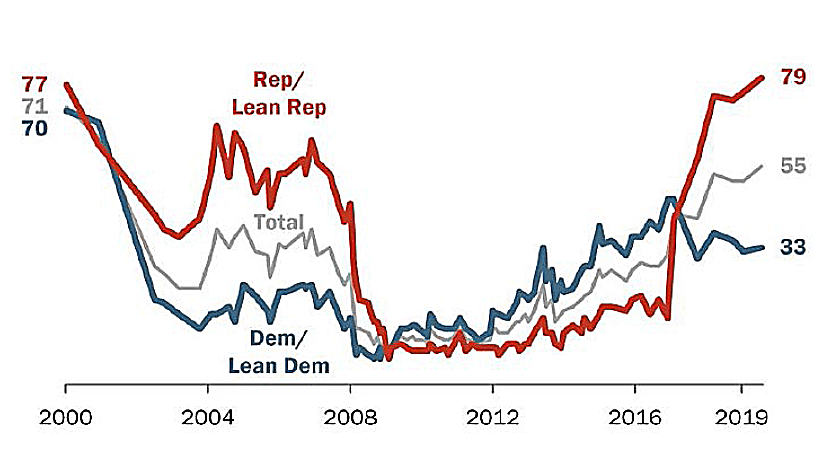

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how Kraft's employer-sponsored benefits fit into the broader picture. According to publicly available information, Kraft does not maintain a traditional defined benefit pension plan, making your 401(k) plan and personal savings the primary vehicles for retirement income. We encourage you to review your Summary Plan Description (SPD) or speak with Kraft's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

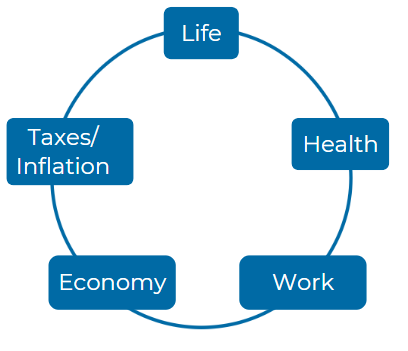

Consider these five Elements:

Â

Â

How does the pension plan offered by Kraft Foods Global, Inc. compare to standard retirement plans in terms of employer contribution allocation, and what specific policies should employees be aware of when considering their retirement options through Kraft Foods Global, Inc.?

Kraft Foods Global, Inc. Pension Plan vs. Standard Retirement Plans: The pension plan offered by Kraft Foods Global, Inc. operates as a defined benefit plan, which allocates employer contributions based on years of service and compensation, ensuring steady retirement income based on a formula. This contrasts with standard retirement plans like 401(k)s, where contributions are often employee-driven and subject to market performance. Employees should understand that the guaranteed nature of a pension provides long-term stability, but they must consider the plan’s specific terms regarding eligibility, vesting, and distribution options.

In what ways do the eligibility requirements for contributions to the retirement plans at Kraft Foods Global, Inc. align with IRS regulations for 2024, and what should employees know about these rules when planning their retirement funds?

Eligibility and IRS Regulations for 2024: The eligibility requirements for Kraft Foods Global, Inc.’s retirement plan align with IRS regulations by requiring one year of service for plan participation, with no minimum age requirement. This is typical for defined benefit plans and is in line with IRS standards for qualified plans. Employees planning their retirement funds should ensure they meet the service requirements and understand that contributions are employer-funded rather than employee-driven, unlike other retirement plans that follow IRS contribution limits(Kraft Foods Global Inc_…).

Considering the defined benefit plan structure of Kraft Foods Global, Inc., how are distributions processed at retirement, and what potential tax implications should employees consider when deciding between a lump sum or annuity option upon retirement?

Distribution Options and Tax Implications: Kraft Foods Global, Inc.’s defined benefit plan offers both lump sum and annuity options for retirement distributions. Employees must carefully consider tax implications: lump sums may be subject to immediate taxation, while annuity payments spread income over time, potentially offering tax advantages. Employees should evaluate their financial needs and tax situation to choose the most suitable option for their retirement(Kraft Foods Global Inc_…).

How does Kraft Foods Global, Inc. ensure the stability and sustainability of its retirement funds, known as the retirement plan funding levels, and what measures are in place to protect employees' interests in case of economic downturns?

Retirement Plan Stability and Economic Downturns: Kraft Foods Global, Inc. ensures the stability and sustainability of its retirement funds through a well-funded pension plan, with funding levels reported at over 100%. This level of funding offers protection against economic downturns, safeguarding employee interests. The company also maintains a significant fidelity bond, providing additional security for plan participants in case of adverse financial events(Kraft Foods Global Inc_…).

What resources are available to employees of Kraft Foods Global, Inc. for financial planning assistance related to their retirement, and how can knowledge of these resources influence their decisions regarding retirement savings and benefits?

Financial Planning Resources: Employees of Kraft Foods Global, Inc. have access to various resources, such as retirement plan summaries and consultations with financial planners. These tools can help employees make informed decisions regarding their retirement savings and benefits, potentially influencing their strategies for maximizing contributions and taking advantage of plan features like early retirement options(Kraft Foods Global Inc_…).

How should employees at Kraft Foods Global, Inc. approach the process for requesting a distribution from their retirement plan, and what specific information is required to expedite this process effectively?

Requesting a Distribution: Employees at Kraft Foods Global, Inc. must contact the plan administrator to request a distribution. Providing accurate personal information, retirement dates, and preferred payment methods is essential to expedite the process. It’s crucial to ensure that all documentation is complete to avoid delays(Kraft Foods Global Inc_…).

How does the participation in the additional retirement plans offered by Kraft Foods Global, Inc., such as the Thrift Investment Plan, benefit employees in the context of overall retirement savings and IRS contribution limits for 2024?

Additional Retirement Plans and IRS Contribution Limits: Participation in Kraft Foods Global, Inc.’s Thrift Investment Plan allows employees to enhance their retirement savings while adhering to IRS contribution limits for 2024. This plan complements the pension plan by offering a defined contribution option, giving employees the chance to maximize their overall retirement savings through a combination of employer contributions and personal investments(Kraft Foods Global Inc_…).

What communication channels does Kraft Foods Global, Inc. provide for employees to ask questions or seek clarification regarding their retirement benefits, and what should employees include in their inquiries to receive detailed answers?

Communication Channels for Retirement Benefits: Kraft Foods Global, Inc. provides clear communication channels through its HR department and plan administrators, where employees can ask detailed questions about their retirement benefits. It’s advisable for employees to include specific details in their inquiries, such as their years of service and expected retirement dates, to receive thorough responses(Kraft Foods Global Inc_…).

How do the overall retirement plan offerings at Kraft Foods Global, Inc. facilitate long-term financial security for employees compared to industry standards, and what unique features should employees leverage to maximize their retirement savings?

Maximizing Long-Term Financial Security: The retirement plan offerings at Kraft Foods Global, Inc. focus on long-term financial security by providing guaranteed income through its defined benefit structure. Compared to industry standards, this approach offers employees a more predictable and stable source of retirement income. Employees should leverage features like early retirement options and understand their full benefit potential to optimize their financial outcomes(Kraft Foods Global Inc_…).

What strategies should employees at Kraft Foods Global, Inc. employ to ensure they remain informed about ongoing changes in retirement planning regulations and plan offerings as they approach retirement, especially in light of any adjustments to IRS rules or company policies?

Staying Informed on Retirement Plan Changes: Employees should stay informed about ongoing changes in retirement planning regulations and company policies by regularly reviewing updates from Kraft Foods Global, Inc. and keeping track of IRS adjustments. Attending company-provided financial planning seminars and consulting with financial advisors can help ensure that employees are well-prepared for retirement, especially as IRS rules or plan offerings evolve(Kraft Foods Global Inc_…).

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.