New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for Kroger Employees and Retirees

/General/General%2010.png?width=1280&height=853&name=General%2010.png)

The sustained volatility in crude oil markets, with prices ranging from $50 to $120 and annualized swings near 80%, creates economic effects that extend far beyond energy companies. Refrigerated distribution networks and petroleum-based packaging costs mean grocery retailers face direct margin pressure from sustained crude price increases. For Kroger employees building retirement savings, oil-driven inflation and market volatility make disciplined saving and diversified allocation more important, as energy cycles can disrupt both portfolio values and purchasing power. Working with a financial advisor helps ensure that energy market uncertainty does not undermine your long-term retirement and financial goals.

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

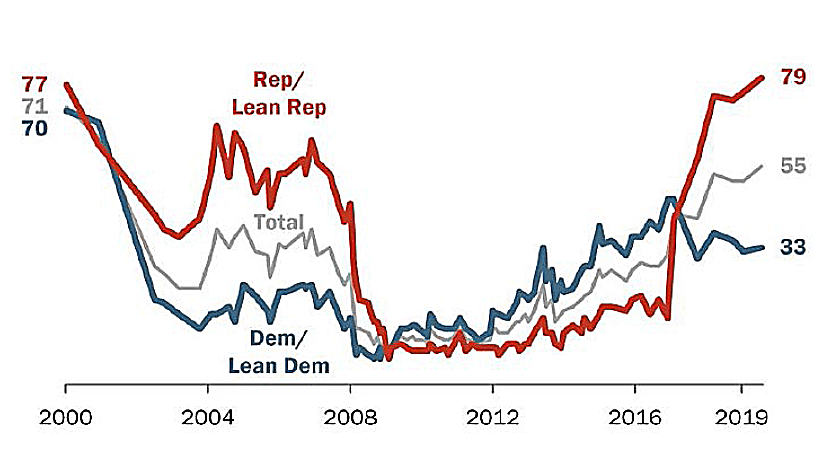

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how Kroger's employer-sponsored benefits fit into the broader picture. According to publicly available information, Kroger maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. Kroger also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with Kroger's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

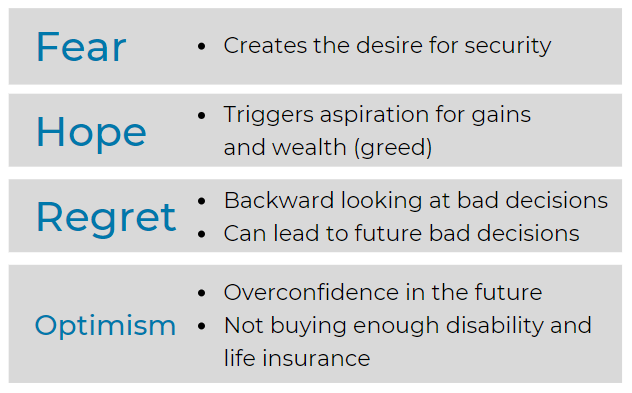

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

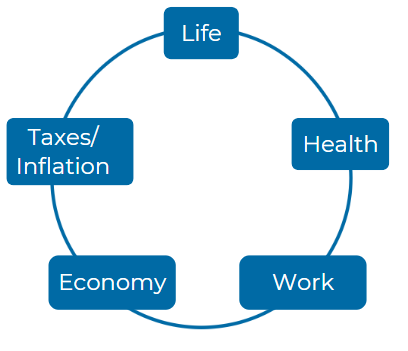

Consider these five Elements:

Â

Â

How does the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN ensure that employees receive adequate retirement benefits calculated based on their years of service and compensation? Are there specific formulas or formulas that KROGER uses to ensure fair distribution of benefits among its participants, particularly in regards to early retirement adjustments?

The KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN ensures that employees receive adequate retirement benefits based on a formula that takes into account both years of credited service and compensation. The plan, being a defined benefit plan, calculates benefits that are typically paid out monthly upon reaching the normal retirement age, but adjustments can be made for early retirement. This formula guarantees that employees who retire early will see reductions based on the plan’s terms, ensuring a fair distribution across participants(KROGER_2023-10-01_QDRO_…).

In what ways does the cash balance formula mentioned in the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN impact the retirement planning of employees? How are these benefits expressed in more relatable terms similar to a defined contribution plan, and how might this affect an employee's perception of their retirement savings?

The cash balance formula in the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN impacts retirement planning by expressing benefits in a manner similar to defined contribution plans. Instead of a traditional annuity calculation, the benefits are often framed as a hypothetical account balance or lump sum, which might make it easier for employees to relate their retirement savings to more familiar terms, thereby influencing how they perceive the growth and adequacy of their retirement savings(KROGER_2023-10-01_QDRO_…).

Can you explain the concept of "shared payment" and "separate interest" as they apply to the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN? How do these payment structures affect retirees and their alternate payees, and what considerations should participants keep in mind when navigating these options?

In the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN, "shared payment" refers to a payment structure where the alternate payee receives a portion of the participant’s benefit during the participant's lifetime. In contrast, "separate interest" means that the alternate payee receives a separate benefit, typically over their own lifetime. These structures impact how retirees and their alternate payees manage their retirement income, with shared payments being tied to the participant’s life and separate interests providing independent payments(KROGER_2023-10-01_QDRO_…).

What procedures does KROGER have in place for employees to access or review the applicable Summary Plan Description? How can understanding this document help employees make more informed decisions regarding their retirement benefits and entitlements under the KROGER plan?

KROGER provides procedures for employees to access the Summary Plan Description, typically through HR or digital platforms. Understanding this document is crucial as it outlines the plan’s specific terms, helping employees make more informed decisions about retirement benefits, including when to retire and how to maximize their benefits under the plan(KROGER_2023-10-01_QDRO_…).

With regard to early retirement options, what specific features of the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN can employees take advantage of? How does the plan's definition of "normal retirement age" influence an employee's decision to retire early, and what potential consequences might this have on their benefits?

The KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN offers early retirement options that include adjustments for those retiring before the plan’s defined "normal retirement age." This early retirement can result in reduced benefits, so employees must carefully consider how retiring early will impact their overall retirement income. The definition of normal retirement age serves as a benchmark, influencing the timing of retirement decisions(KROGER_2023-10-01_QDRO_…).

How does the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN address potential changes in federal regulations or tax law that may impact retirement plans? In what ways does KROGER communicate these changes to employees, and how can participants stay informed about updates to their retirement benefits?

The KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN incorporates changes in federal regulations or tax laws by updating the plan terms accordingly. KROGER communicates these changes to employees through official channels, such as newsletters or HR communications, ensuring participants are informed and can adjust their retirement planning in line with regulatory changes(KROGER_2023-10-01_QDRO_…).

What are some common misconceptions regarding participation in the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN that employees might have? How can these misconceptions impact their retirement planning strategies, and what resources does KROGER provide to clarify these issues?

A common misconception regarding participation in the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN is that it functions similarly to a defined contribution plan, which it does not. This can lead to confusion about benefit accrual and payouts. KROGER provides resources such as plan summaries and HR support to clarify these misunderstandings and help employees better strategize their retirement plans(KROGER_2023-10-01_QDRO_…).

How does the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN interact with other employer-sponsored retirement plans, specifically concerning offsetting benefits? What implications does this have for employees who may also be participating in defined contribution plans?

The KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN interacts with other employer-sponsored retirement plans by offsetting benefits, particularly with defined contribution plans. This means that benefits from the defined benefit plan may be reduced if the employee is also receiving benefits from a defined contribution plan, impacting the total retirement income(KROGER_2023-10-01_QDRO_…).

What options are available to employees of KROGER regarding the distribution of their retirement benefits upon reaching retirement age? How can employees effectively plan their retirement income to ensure sustainability through their retirement years based on the features of the KROGER plan?

Upon reaching retirement age, KROGER employees have various options for distributing their retirement benefits, including lump sums or annuity payments. Employees should carefully plan their retirement income, considering the sustainability of their benefits through their retirement years. The plan’s features provide flexibility, allowing employees to choose the option that best fits their financial goals(KROGER_2023-10-01_QDRO_…).

How can employees contact KROGER for more information or assistance regarding the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN? What are the recommended channels for employees seeking guidance on their retirement benefits, and what type of support can they expect from KROGER's human resources team?

Employees seeking more information or assistance regarding the KROGER CONSOLIDATED RETIREMENT BENEFIT PLAN can contact the company through HR or dedicated plan administrators. The recommended channels include direct communication with HR or online resources. Employees can expect detailed support in understanding their benefits and planning for retirement(KROGER_2023-10-01_QDRO_…).

For more information you can reach the plan administrator for Kroger at 104 vine street Cincinnati, OH 45202-1100; or by calling them at 513-762-4000.

https://www.thekrogerco.com/documents/pension-plan-2022.pdf - Page 5, https://www.thekrogerco.com/documents/pension-plan-2023.pdf - Page 12, https://www.thekrogerco.com/documents/pension-plan-2024.pdf - Page 15, https://www.thekrogerco.com/documents/401k-plan-2022.pdf - Page 8, https://www.thekrogerco.com/documents/401k-plan-2023.pdf - Page 22, https://www.thekrogerco.com/documents/401k-plan-2024.pdf - Page 28, https://www.thekrogerco.com/documents/rsu-plan-2022.pdf - Page 20, https://www.thekrogerco.com/documents/rsu-plan-2023.pdf - Page 14, https://www.thekrogerco.com/documents/rsu-plan-2024.pdf - Page 17, https://www.thekrogerco.com/documents/healthcare-plan-2022.pdf - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.