New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for L3Harris Employees and Retirees

/General/General%2011.png?width=1280&height=853&name=General%2011.png)

Energy market instability persists, with crude prices fluctuating between $50 and $120 per barrel and annualized volatility running around 80%. The effects reach well beyond the energy sector. Jet fuel costs, petrochemical composite materials, and fixed-price contract structures mean elevated crude prices create margin pressure across the aerospace supply chain. L3Harris employees building long-term savings should recognize that oil-driven economic conditions can affect both the growth of their portfolios and the purchasing power of their eventual retirement income. Consulting with a financial advisor can help you understand how energy conditions affect your specific situation and build a plan that adapts accordingly.

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

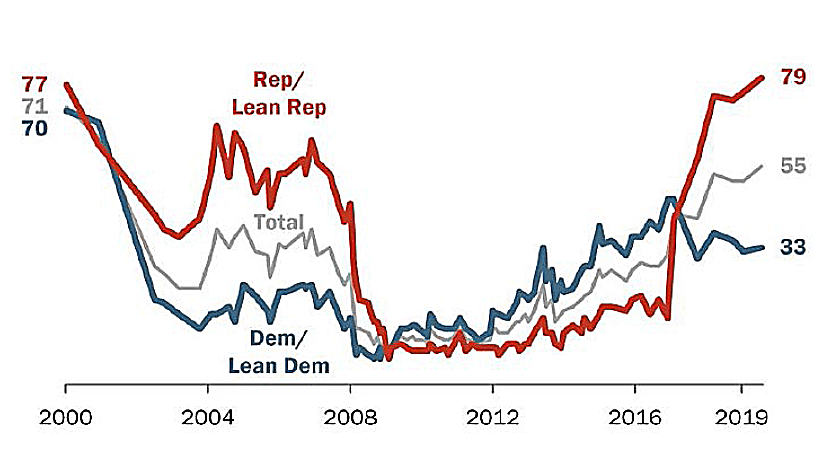

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how L3Harris's employer-sponsored benefits fit into the broader picture. According to publicly available information, L3Harris maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. L3Harris also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with L3Harris's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

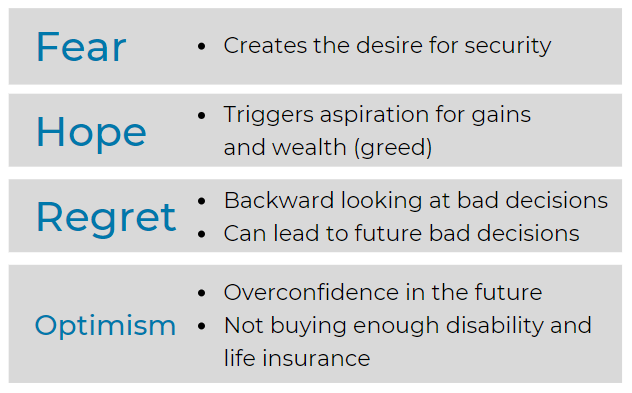

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

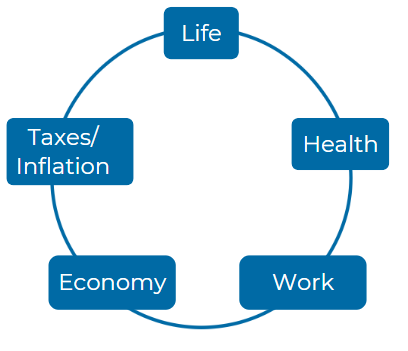

Consider these five Elements:

Â

Â

What specific factors should L3Harris Technologies employees consider when determining the most suitable form of pension benefit at retirement? Employees of L3Harris Technologies may have various options, such as life annuities, contingent annuities, and lump-sum payouts. Understanding the implications of each option, including tax treatments and benefit guarantees, can be crucial in making a decision that aligns with long-term financial goals. It is also important to consider how the selected form may affect survivor benefits and overall retirement income planning.

Pension Options at Retirement: L3Harris Technologies employees have various pension benefit options to consider at retirement, such as life annuities, contingent annuities, and lump-sum payouts(L3Harris Technologies I…). Each option has different tax treatments, survivor benefits, and guarantees. For example, selecting a life annuity ensures a fixed monthly payment for life, while a lump-sum payout might offer more flexibility but comes with immediate tax implications. Employees should evaluate how each option aligns with their long-term financial goals and whether it provides adequate survivor protection for dependents(L3Harris Technologies I…).

How does L3Harris Technologies determine eligibility for early retirement, and what implications does this have for pension benefits? Employees should familiarize themselves with the criteria for qualifying for early retirement, including age and service requirements. Additionally, understanding the benefits that are available should retirement occur before the standard retirement age can affect financial planning, as these benefits can differ significantly from those available at normal retirement age due to reduction factors or penalties.

Early Retirement Eligibility: L3Harris Technologies determines eligibility for early retirement based on age and years of service. Employees may qualify for early retirement if they are at least 55 years old and have completed 10 years of service(L3Harris Technologies I…). Opting for early retirement can result in a reduced pension benefit due to the longer payment period. These reductions, known as early retirement penalties, affect financial planning since the payout is lower compared to waiting until the normal retirement age(L3Harris Technologies I…).

In what ways do the pension formulas at L3Harris Technologies differ, and how can employees assess which plan is most advantageous for their retirement? Employees participating in the L3Harris pension plan can choose between different formulas, such as the Traditional Pension Plan and the Pension Equity Plan. Assessing which formula may yield higher benefits involves understanding the benefits calculation processes, including how each formula accounts for years of service, salary history, and participation criteria, which can significantly impact total retirement income.

Pension Formulas: L3Harris employees can choose between different pension formulas, such as the Traditional Pension Plan and Pension Equity Plan(L3Harris Technologies I…). The Traditional Plan is based on years of service and final average pay, while the Pension Equity Plan uses a lump-sum formula that accrues value over time. Understanding how each formula calculates benefits is essential for employees to determine which plan will provide higher retirement income, depending on their service years and salary history(L3Harris Technologies I…).

How should L3Harris Technologies employees prepare for the selection of a beneficiary, and what are the potential impacts on their pension benefits? Selecting a beneficiary is an important component of retirement planning. Employees at L3Harris Technologies must understand the implications that come with adding a spouse or other individuals as beneficiaries, including the effect on benefit amounts and how beneficiary selection can influence survivor payouts. Moreover, they should familiarize themselves with the requirements for updating beneficiary information and the legal implications of such designations.

Beneficiary Selection: Choosing a beneficiary is a crucial step for L3Harris employees. Adding a spouse or another individual as a beneficiary may reduce the employee's pension benefit but ensures that a portion of the pension continues after the employee's death(L3Harris Technologies I…). Employees should be aware of the survivor benefit provisions, spousal consent requirements, and the need to regularly update their beneficiary information(L3Harris Technologies I…).

What procedures must L3Harris Technologies employees follow to appeal a denied pension benefit claim, and what timelines should they be aware of? Employees should be well-informed about the steps involved in the appeals process for denied claims, including how and when to file an appeal and the importance of providing adequate documentation. Understanding the statutes of limitations related to claims and appeals can significantly influence the outcomes for employees seeking to reinstate or secure their benefits.

Appealing Denied Claims: L3Harris Technologies employees must follow a formal process to appeal denied pension benefit claims(L3Harris Technologies I…). The process includes submitting an appeal within a specific timeframe and providing supporting documentation. It is important to be familiar with the statute of limitations and administrative remedies to ensure the best chance of success when appealing a decision(L3Harris Technologies I…).

How does L3Harris Technologies handle survivor benefits, and what actions should employees take to ensure that their surviving spouses or partners have access to these benefits? Understanding the components of survivor benefits at L3Harris Technologies is crucial. Employees should learn about the eligibility of their spouses or partners following their death, the type of benefits due, and any actions required to secure these benefits. Familiarity with the plan’s rules surrounding survivor benefits and timelines for elections can also affect the financial security of beneficiaries.

Survivor Benefits: L3Harris offers survivor benefits to spouses or designated beneficiaries(L3Harris Technologies I…). Employees must ensure that their spouse or partner is properly designated to receive these benefits, which may involve selecting an annuity option that provides continued payments to the survivor. Understanding the timelines for making these elections and the rules governing survivor benefits is crucial for securing financial support for loved ones(L3Harris Technologies I…).

What resources are available for L3Harris Technologies employees for receiving personalized retirement counseling, and how can these resources aid in making informed financial decisions? Employees may benefit from accessing professional counseling services or informational resources provided by L3Harris Technologies. These resources can include individual retirement planning sessions that help employees align their pension benefits with their overall retirement strategy, ensuring that they utilize their benefits effectively and are informed about their options.

Retirement Counseling Resources: L3Harris provides personalized retirement counseling services to assist employees with their pension and retirement planning(L3Harris Technologies I…). These resources include individual sessions to discuss how pension benefits fit into overall retirement strategies. By leveraging these services, employees can make well-informed decisions about their financial future(L3Harris Technologies I…).

How can employees of L3Harris Technologies find out more about their eligibility for the Cash Balance Plan and the advantages of this plan over traditional pension formulas? Employees should research what defines an "active Cash Balance Plan Participant" as well as the benefit calculations associated with it. Investigating the elements that set this type of plan apart—specifically regarding lump-sum distributions and the ability to track benefits—can better inform employees about the potential advantages for their future retirement income.

Cash Balance Plan: Employees interested in the Cash Balance Plan can research its advantages over traditional pension formulas. The Cash Balance Plan allows for lump-sum distributions and provides clear benefit tracking, which can be more appealing to employees looking for flexibility and control over their retirement funds(L3Harris Technologies I…).

What impact do potential changes to the L3Harris Technologies pension plan have on current employees, and what steps should they take to stay informed about such changes? Employees should remain vigilant regarding any amendments to the pension plan that could influence their retirement benefits. This includes understanding their rights under ERISA and staying engaged with communication from L3Harris regarding plan updates, ensuring that they are equipped to make timely decisions based on the latest information.

Plan Changes: L3Harris employees should stay updated on any changes to the pension plan, which could impact their benefits(L3Harris Technologies I…). Monitoring communications from the company and understanding their rights under ERISA is essential to making timely decisions based on new plan terms or amendments(L3Harris Technologies I…).

How can employees of L3Harris Technologies contact the Benefits Service Center to address specific questions regarding their pension plan or retirement strategy? It is essential for employees seeking clarity on their pension benefits or retirement planning to know how to reach out to the L3Harris Benefits Service Center. This center acts as a vital resource, and understanding its operations—including contact times, methods of contact, and the types of inquiries that can be addressed—will enable employees to receive the guidance they need regarding their benefits.

Benefits Service Center: L3Harris employees can contact the Benefits Service Center for any questions regarding their pension or retirement strategy. The center provides assistance with understanding pension benefits, resolving issues, and addressing specific inquiries related to retirement planning(L3Harris Technologies I…)(L3Harris Technologies I…).

For more information you can reach the plan administrator for L3Harris at 1025 w nasa blvd Melbourne, FL 32919; or by calling them at 800-528-7711.

https://www.l3harris.com/documents/pension-plan-2022.pdf - Page 5, https://www.l3harris.com/documents/pension-plan-2023.pdf - Page 12, https://www.l3harris.com/documents/pension-plan-2024.pdf - Page 15, https://www.l3harris.com/documents/401k-plan-2022.pdf - Page 8, https://www.l3harris.com/documents/401k-plan-2023.pdf - Page 22, https://www.l3harris.com/documents/401k-plan-2024.pdf - Page 28, https://www.l3harris.com/documents/rsu-plan-2022.pdf - Page 20, https://www.l3harris.com/documents/rsu-plan-2023.pdf - Page 14, https://www.l3harris.com/documents/rsu-plan-2024.pdf - Page 17, https://www.l3harris.com/documents/healthcare-plan-2022.pdf - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.