/General/General%201.png?width=1280&height=853&name=General%201.png)

Healthcare Provider Update: Healthcare Provider for Lockheed Martin Lockheed Martin primarily partners with UnitedHealthcare to provide healthcare benefits to its employees. This collaboration allows Lockheed Martin to offer comprehensive health plans tailored to meet the diverse needs of its workforce across various locations. Healthcare Cost Increases in 2026 As healthcare costs are projected to rise significantly in 2026, Lockheed Martin employees may face increased out-of-pocket expenses. Following trends revealed in recent reports, health insurance premiums for many states are slated to soar, with some seeing hikes exceeding 60%. Contributing factors include rising medical costs due to inflation and the anticipated expiration of federal premium subsidies, which could push the average increase for consumers to over 75%. The combination of these elements suggests that both employees and employers may need to strategize for heightened healthcare expenses in the coming year. Click here to learn more

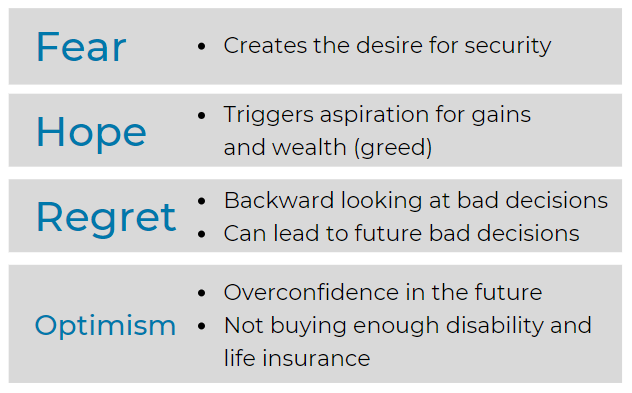

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Three Uncertain Periods:

S&P 500 Index

Featured Video

Articles you may find interesting:

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

GDP Annualized Growth Rate

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Sources: Standard & Poor’s Corporation; Copyright 2020 Crandall, Pierce & Company

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions” pages in the Appendix for additional information.

-

Pivotal to understanding ourselves

Nasdaq Composite: 2010-2021

data-hs-cos-general-type='widget' data-hs-cos-type='module'>

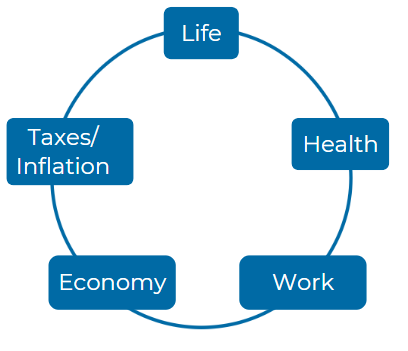

Consider these five Elements:

How does Lockheed Martin determine the monthly pension benefit for employees nearing retirement, and what factors should employees consider when planning their retirement based on this calculation? Specifically, how do the concepts of "Final Average Pay" and "Credited Years of Service" interact in the pension calculation under Lockheed Martin’s retirement plan?

Lockheed Martin Pension Calculation: Lockheed Martin calculates monthly pension benefits using the "Final Average Pay" (FAP) and "Credited Years of Service" (CYS). The FAP is determined by averaging the three highest annual compensations prior to 2016, while CYS counts the years from employment start to December 31, 2019, when the pension was frozen. The benefit per year of service is calculated based on whether the FAP is less than or exceeds the Social Security Covered Compensation, with specific formulas applied for each scenario. These calculations directly affect the monthly pension benefit, which may also be reduced if retirement commences before a certain age due to early retirement penalties.

Given the recent changes in Lockheed Martin's pension policy, what implications could this have for employees who are planning to retire in the near future? How should these employees navigate their expectations regarding retirement income given that the pension has been frozen since 2020?

Implications of Pension Freeze: Since Lockheed Martin froze its pension plan in 2020, no future earnings or years of service will increase pension benefits. This freeze shifts the emphasis towards maximizing contributions to 401(k) plans, where Lockheed Martin increased its maximum contribution to 10% for non-represented employees. Employees planning for imminent retirement should recalibrate their financial planning to account for this change, prioritizing 401(k) growth and other retirement savings vehicles to compensate for the pension freeze.

What options does Lockheed Martin provide for employees regarding healthcare insurance as they approach retirement age? How do these options compare in terms of coverage and cost, particularly for those who will transition to Medicare upon reaching age 65?

Healthcare Options Near Retirement: As Lockheed Martin employees approach retirement, they can choose from several health insurance options. Before Medicare eligibility, they may use COBRA, a Lockheed Martin retiree plan, or the ACA's private marketplace. Post-65, they transition to Medicare, with the possibility of additional coverage through Medicare Advantage or Medigap plans. Lockheed Martin supports this transition with a Health Reimbursement Arrangement, providing an annual credit to help cover medical expenses.

Understanding the complex nature of Lockheed Martin's pension and retirement benefits, what resources are available to employees to help them navigate their choices regarding pension claiming options? In what ways can the insights from these resources aid employees in making informed decisions about their financial future?

Resources for Navigating Retirement Benefits: Lockheed Martin employees have access to resources like the LM Employee Service Center intranet, which includes robust tools such as a pension estimator. This tool allows for modeling different retirement scenarios and understanding the impacts of various pension claiming options. Additional support is provided through HR consultations and detailed plan descriptions to ensure employees make informed decisions about their retirement strategies.

For employees with varying years of service at Lockheed Martin, how can their employment history impact their pension benefits? What strategies should individuals explore to maximize their benefits given the different legacy systems that might influence their retirement payout?

Impact of Employment History on Pension Benefits: The length and nature of an employee’s service at Lockheed Martin significantly influence pension calculations. Historical changes in pension policies, particularly the transition points of the pension freeze, play critical roles in determining the final pension benefits. Employees must consider their entire career timeline, including any represented or non-represented periods, to understand and maximize their eligible pension benefits fully.

How does the Lockheed Martin retirement plan ensure that benefits are preserved for spouses or dependents after an employee's passing? How do different claiming options affect the long-term financial security of the employee's family post-retirement?

Benefit Preservation for Dependents: Lockheed Martin's pension plan includes options that consider the welfare of spouses or dependents after an employee's passing. Options like "Joint and Survivor" ensure ongoing benefits for surviving spouses, while choices like "Life with X-Year guarantee" provide continued payments for a defined period after the employee’s death. Understanding these options helps secure long-term financial stability for beneficiaries.

What steps can Lockheed Martin employees take to prepare financially for retirement, especially if they have outstanding loans or financial obligations? How crucial is it for employees to understand the conditions under which these loans must be settled before retirement?

Financial Preparation for Retirement: Employees approaching retirement should focus on clearing any outstanding loans and maximizing their contributions to tax-advantaged accounts like 401(k)s and Health Savings Accounts (HSAs). These steps are crucial for ensuring a smooth financial transition to retirement, minimizing potential tax impacts, and maximizing available retirement income streams.

With the evolution of Lockheed Martin's retirement initiatives, particularly the shift toward higher 401(k) contributions, how should employees balance contributions to their 401(k) with their overall retirement savings strategy? What factors should they consider in optimizing their investment choices post-retirement?

Balancing 401(k) Contributions: With the pension freeze, Lockheed Martin employees should increasingly rely on 401(k) plans, where the company has increased its contribution cap. Employees must balance these contributions with other savings strategies and consider their investment choices carefully to ensure a robust retirement fund that can support their post-retirement life.

How does Lockheed Martin's approach to retirement planning include the management of health savings accounts (HSAs) for retirees? What are the tax advantages of HSAs, and how can employees effectively utilize this resource when planning for healthcare expenses in retirement?

Management of HSAs for Retirees: Lockheed Martin encourages maximizing contributions to Health Savings Accounts (HSAs), which offer significant tax advantages. These accounts not only provide funds for current medical expenses but can also be used tax-free for healthcare costs in retirement, making them a critical component of retirement health expense planning.

What is the best way for employees to contact Lockheed Martin regarding specifics or questions about their retirement benefits? What channels of communication are available, and how can they access the most current and relevant information regarding their retirement planning? These questions aim to encourage thoughtful consideration and discussion about retirement planning within Lockheed Martin, addressing various aspects of the company's benefits while promoting engagement with internal resources.

Contacting Lockheed Martin for Retirement Benefit Queries: Employees should direct specific inquiries about their retirement benefits to Lockheed Martin's HR department or consult the benefits Summary Plan Descriptions available through company resources. These channels ensure employees receive accurate and comprehensive information tailored to their individual circumstances.

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

.webp?width=300&height=200&name=office-builing-main-lobby%20(27).webp)

-2.png)

.webp)