New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for Lumen Employees and Retirees

/General/General%203.png?width=1280&height=853&name=General%203.png)

Crude oil prices remain elevated and volatile, with annualized volatility around 80% and prices ranging between $50 and $120 per barrel over the past six months. Fleet fuel for service vehicles, backup generator diesel, and cell tower energy consumption connect telecom infrastructure operations to crude oil price movements. For Lumen employees building retirement savings, oil-driven inflation and market volatility make disciplined saving and diversified allocation more important, as energy cycles can disrupt both portfolio values and purchasing power. A financial advisor can help you build strategies that maintain progress toward retirement goals through periods of energy-driven economic turbulence.

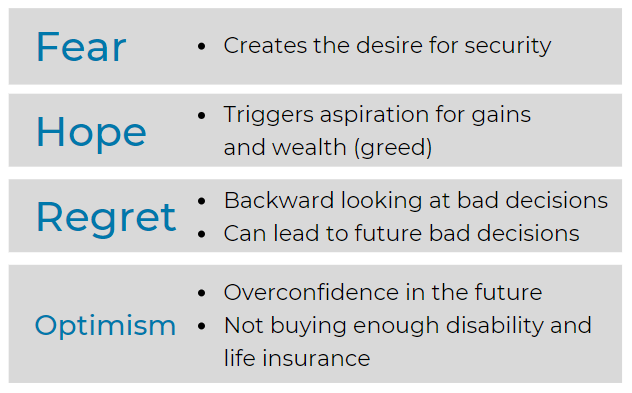

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

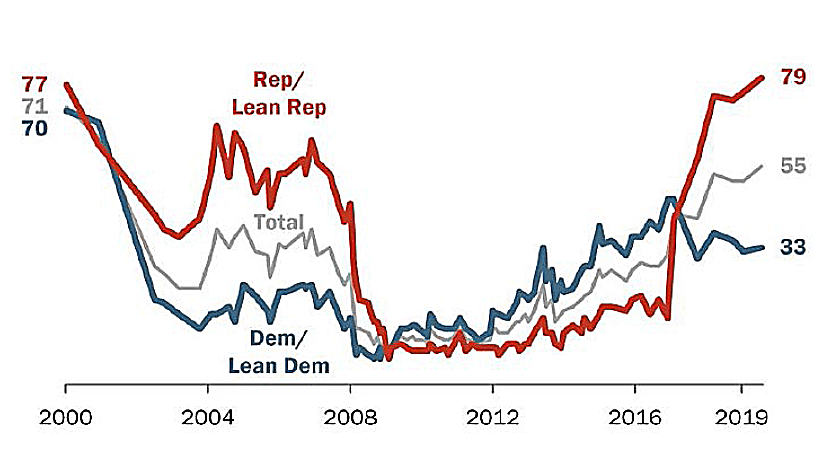

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how Lumen's employer-sponsored benefits fit into the broader picture. According to publicly available information, Lumen maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. Lumen does not appear to offer a formal retiree healthcare program, making healthcare coverage planning an important consideration if you retire before age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with Lumen's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

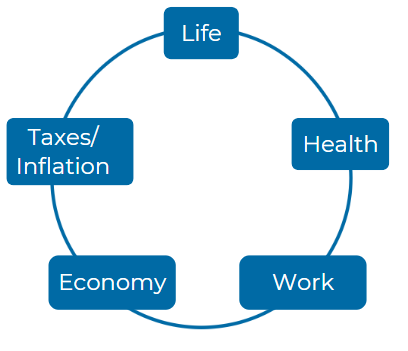

Consider these five Elements:

Â

Â

What specific retirement benefits does Lumen Technologies, Inc. offer to employees who have dedicated many years of service to the company? In what ways do these benefits reflect Lumen's commitment to taking care of its employees post-retirement, and how do they align with the company's overall values regarding employee welfare and support?

Retirement Benefits: Lumen Technologies offers its employees retirement benefits that include 401(k) plans and pension options, reflecting its commitment to post-retirement welfare. These benefits are aligned with Lumen’s values of providing security and care for its employees after years of dedicated service. They are designed to ensure long-term financial stability for retirees, aligning with Lumen's mission of enhancing employee well-being(Lumen Technologies Inc_…).

As an employee of Lumen Technologies, Inc., how can you effectively plan for your retirement to maximize your benefits? What factors should you consider, and what resources does Lumen provide to help employees navigate the complexities of retirement planning to ensure a secure financial future?

Retirement Planning: As an employee of Lumen Technologies, you should consider factors like years of service, retirement plan contributions, and projected retirement age to maximize your benefits. Lumen provides resources such as retirement calculators and financial planning tools to help employees navigate these complexities and secure their financial future post-retirement(Lumen Technologies Inc_…).

How do Lumen Technologies, Inc.'s retirement plans compare with the industry standards? In which areas can Lumen improve its offerings to remain competitive and retain top talent while ensuring the financial security of its employees in their retirement years?

Comparison with Industry Standards: Lumen’s retirement plans are competitive within the industry, but improvements could be made in areas such as enhanced pension offerings or matching contributions in the 401(k) plans to attract and retain top talent. This would ensure financial security for employees in their retirement years while keeping Lumen competitive in the market(Lumen Technologies Inc_…).

Can you explain the role of the HRCC (Human Resources and Compensation Committee) at Lumen Technologies, Inc. in overseeing employee retirement plans? What measures does this committee take to ensure that retirement benefits remain aligned with the organization’s goals and employee expectations?

HRCC Role in Retirement Plans: The Human Resources and Compensation Committee (HRCC) at Lumen oversees retirement benefits to ensure they align with the company’s goals and employee expectations. The committee reviews and updates the plans regularly, ensuring they remain relevant and meet both the company’s financial objectives and the needs of its employees(Lumen Technologies Inc_…).

What changes to federal regulations or IRS limits in 2024 could potentially impact Lumen Technologies, Inc.'s retirement plans? How should employees prepare for these potential changes to ensure they are fully utilizing their benefits?

Federal Regulation Changes in 2024: Changes to IRS limits or federal regulations, such as adjustments to contribution caps or tax deductions, could impact Lumen’s retirement plans. Employees should stay informed about these changes to fully utilize their benefits, and Lumen’s HR team provides updates and resources to assist in navigating these regulatory adjustments(Lumen Technologies Inc_…).

How does Lumen Technologies, Inc. ensure that all employees are aware of their retirement options? What communication strategies does the company employ to make sure employees understand the specifics of their retirement benefits and the necessary steps for enrollment or participation?

Employee Awareness of Retirement Options: Lumen employs a variety of communication strategies, including workshops, online resources, and HR consultations, to ensure that employees are aware of their retirement options. Regular updates and easy access to information help employees understand the steps needed for enrollment or participation(Lumen Technologies Inc_…).

In the event of unforeseen circumstances, such as death or disability, how does Lumen Technologies, Inc. protect the retirement benefits of its employees and their families? What provisions are specifically designed to support employees and their loved ones during these challenging times?

Protection of Retirement Benefits: In cases of death or disability, Lumen has provisions to protect retirement benefits for employees and their families. Survivor benefits and disability accommodations are designed to provide continued financial security for employees and their loved ones during challenging times(Lumen Technologies Inc_…).

For employees nearing retirement at Lumen Technologies, Inc., what strategies should they adopt to ensure they transition smoothly out of the workforce? What resources or programs does Lumen offer to assist employees during this significant life change?

Transitioning to Retirement: Employees nearing retirement at Lumen can benefit from financial planning tools and transition programs offered by the company. These resources help ensure a smooth exit from the workforce and provide the necessary support for this significant life change(Lumen Technologies Inc_…).

How is Lumen Technologies, Inc. addressing the challenges of an aging workforce regarding retirement readiness? What initiatives or programs are in place to help older employees prepare for retirement and to facilitate knowledge transfer to younger employees?

Addressing an Aging Workforce: Lumen is addressing retirement readiness through programs that help older employees prepare for their transition into retirement. These initiatives include financial education, retirement planning resources, and mentorship programs to facilitate knowledge transfer to younger employees(Lumen Technologies Inc_…).

For employees who wish to learn more about the retirement benefits and planning processes offered by Lumen Technologies, Inc., what contact methods are available? How can employees reach out to the appropriate department for detailed inquiries and assistance regarding their retirement options?

Contact Methods for Retirement Inquiries: Employees wishing to learn more about Lumen’s retirement benefits can reach out to the HR department via phone, email, or the company’s internal benefits portal. Lumen’s HR team provides detailed assistance regarding retirement options and planning(Lumen Technologies Inc_…).

For more information you can reach the plan administrator for Lumen at 2500 w utopia rd Phoenix, AZ 85027-4129; or by calling them at 623-582-7000.

https://www.lumen.com/documents/pension-plan-2022.pdf - Page 5, https://www.lumen.com/documents/pension-plan-2023.pdf - Page 12, https://www.lumen.com/documents/pension-plan-2024.pdf - Page 15, https://www.lumen.com/documents/401k-plan-2022.pdf - Page 8, https://www.lumen.com/documents/401k-plan-2023.pdf - Page 22, https://www.lumen.com/documents/401k-plan-2024.pdf - Page 28, https://www.lumen.com/documents/rsu-plan-2022.pdf - Page 20, https://www.lumen.com/documents/rsu-plan-2023.pdf - Page 14, https://www.lumen.com/documents/rsu-plan-2024.pdf - Page 17, https://www.lumen.com/documents/healthcare-plan-2022.pdf - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.