New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for PepsiCo Employees and Retirees

The sustained volatility in crude oil markets, with prices ranging from $50 to $120 and annualized swings near 80%, creates economic effects that extend far beyond energy companies. Petroleum-derived fertilizer costs, packaging materials, and refrigerated logistics connect food and beverage companies directly to crude oil price movements. Retirement savings strategies at PepsiCo should account for how energy price cycles influence inflation, interest rates, and market returns over the long horizons that retirement planning requires. In this environment, a financial advisor can help you assess your exposure to oil-driven economic effects and build appropriately diversified strategies.

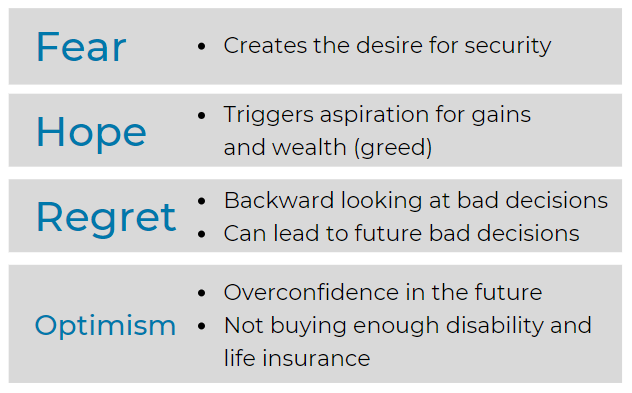

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

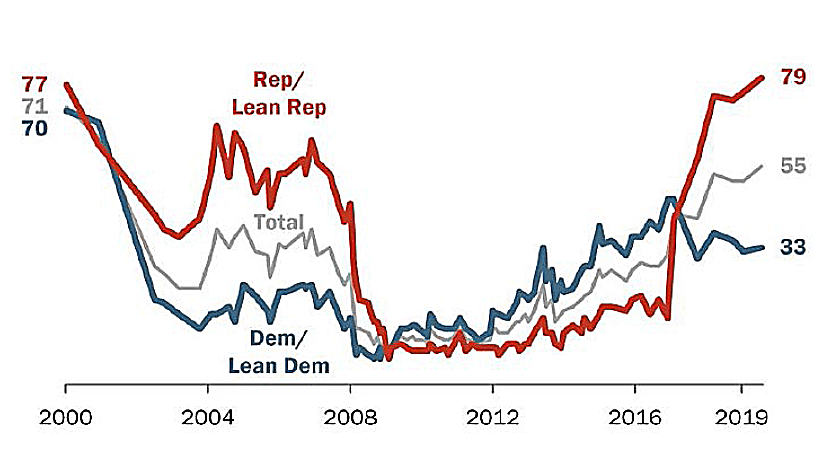

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how PepsiCo's employer-sponsored benefits fit into the broader picture. According to publicly available information, PepsiCo maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. PepsiCo also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with PepsiCo's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

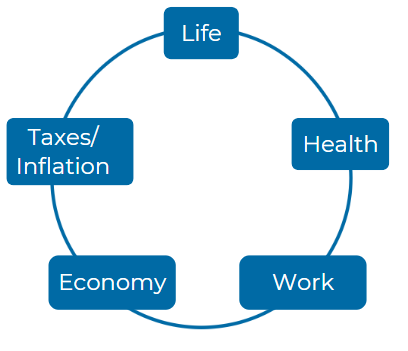

Consider these five Elements:

Â

Â

What are the key steps an employee needs to take to prepare for retirement from PepsiCo, and how do these steps ensure that they maximize their benefits and entitlements?

Preparing for Retirement: Employees preparing for retirement from PepsiCo need to understand their retirement benefits, estimate their financial needs, and officially inform PepsiCo of their decision to retire. These steps are vital to ensure they maximize their benefits, including pensions, 401(k) plans, and retiree healthcare. The PepsiCo Savings and Retirement Center at Fidelity helps guide employees through this process, ensuring they make well-informed decisions(PepsiCo_October 2022_Ge…).

In what ways can PepsiCo employees navigate the complexities of their pension options, and what considerations should they have in mind when deciding between a lump sum and annuity?

Navigating Pension Options: PepsiCo employees can choose between a lump sum or an annuity for their pension benefits. When deciding, they should consider personal circumstances, such as life expectancy and financial needs. Employees can use the NetBenefits platform to estimate pension values at different retirement dates and consult financial counselors through Healthy Money for personalized advice(PepsiCo_October 2022_Ge…).

How does the PepsiCo Retiree Health Care Program function after retirement, and what criteria must be met for an employee to effectively enroll and maintain this coverage?

Retiree Health Care Program: PepsiCo offers a Retiree Health Care Program available until employees reach age 65, after which coverage transitions to the Via Benefits marketplace. Employees must actively enroll within 31 days of retirement to maintain coverage, or defer enrollment if preferred. The Retiree Health Care Contribution Estimator helps estimate future costs(PepsiCo_October 2022_Ge…)(PepsiCo_October 2022_Ge…).

How do the Automatic Retirement Contributions (ARC) at PepsiCo enhance an employee's retirement savings strategy, and what options do employees have to manage their ARC investments?

Automatic Retirement Contributions (ARC): Employees who receive ARC can manage their investments through NetBenefits. These contributions are automatically added to their retirement savings, enhancing long-term financial security. Employees can review and adjust their investment options to align with their retirement strategy(PepsiCo_October 2022_Ge…).

For employees aging 50 and over, what catch-up contribution options does PepsiCo provide to help with their 401(k) savings, and how can they take advantage of these benefits in their retirement planning?

Catch-Up Contributions: PepsiCo employees aged 50 and above can contribute additional amounts to their 401(k) plans under the catch-up contribution option. This benefit allows employees to boost their retirement savings, helping them prepare more effectively for retirement(PepsiCo_October 2022_Ge…).

What resources are available through PepsiCo for employees looking to calculate their retirement expenses, and how do these tools help in setting realistic financial goals for retirement?

Retirement Expense Calculators: PepsiCo provides tools like the Fidelity Planning & Guidance Center, which helps employees estimate retirement expenses. This tool includes health care costs, mortgage payments, and other potential retirement expenses, enabling employees to set realistic financial goals(PepsiCo_October 2022_Ge…).

How should employees at PepsiCo approach Social Security benefits when planning for retirement, and what role does the company play in facilitating their understanding of these benefits?

Social Security Benefits: Employees approaching retirement should consider when to start Social Security benefits. PepsiCo provides guidance through Healthy Money, helping employees understand how Social Security fits into their overall retirement strategy(PepsiCo_October 2022_Ge…).

What impact does health care coverage have on retired employees' finances, and how can PepsiCo retirees effectively use the Retiree Health Care Contribution Estimator to prepare for future health costs?

Retiree Health Care Contribution Estimator: Health care can significantly impact a retiree's budget. The Retiree Health Care Contribution Estimator is a tool PepsiCo retirees can use to prepare for future health costs. It helps employees estimate their contributions and explore different plan options to manage their post-retirement health care expenses(PepsiCo_October 2022_Ge…).

How can employees get in touch with the appropriate resources to learn more about PepsiCo’s retirement benefits, and what specific contact information should they keep handy during this process?

Contact Information: To learn more about PepsiCo's retirement benefits, employees should contact the PepsiCo Savings and Retirement Center at Fidelity at 1-800-632-2014. Additionally, they can access resources on NetBenefits or consult Healthy Money counselors for personalized financial guidance(PepsiCo_October 2022_Ge…).

What are the implications of interest rate fluctuations on pension benefit calculations at PepsiCo, and how should employees factor these rates into their retirement planning decisions? These questions encourage a comprehensive understanding of the various aspects of retirement planning specific to PepsiCo, as well as consideration for personal financial management.

Interest Rate Fluctuations and Pension Calculations: PepsiCo employees considering a lump sum pension payout should be aware that lump sum values are inversely related to interest rates. A higher interest rate results in a lower lump sum payout, so employees should monitor interest rate trends when planning their pension distribution(PepsiCo_October 2022_Ge…)(PepsiCo_October 2022_Ge…).

For more information you can reach the plan administrator for PepsiCo at 700 anderson rd Purchase, NY 10577; or by calling them at 914-253-2000.

https://www.pepsico.com/documents/pension-plan-2022.pdf - Page 5 https://www.pepsico.com/documents/pension-plan-2023.pdf - Page 12 https://www.pepsico.com/documents/pension-plan-2024.pdf - Page 15 https://www.pepsico.com/documents/401k-plan-2022.pdf - Page 8 https://www.pepsico.com/documents/401k-plan-2023.pdf - Page 22 https://www.pepsico.com/documents/401k-plan-2024.pdf - Page 28 https://www.pepsico.com/documents/rsu-plan-2022.pdf - Page 20 https://www.pepsico.com/documents/rsu-plan-2023.pdf - Page 14 https://www.pepsico.com/documents/rsu-plan-2024.pdf - Page 17 https://www.pepsico.com/documents/healthcare-plan-2022.pdf - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.