New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for Rockwell Employees and Retirees

/General/General%205.png?width=1280&height=853&name=General%205.png)

The sustained volatility in crude oil markets, with prices ranging from $50 to $120 and annualized swings near 80%, creates economic effects that extend far beyond energy companies. Petroleum-derived adhesives, coatings, plastics, and chemical feedstocks, along with global distribution energy costs, create meaningful oil price exposure for diversified industrial manufacturers. For Rockwell employees building retirement savings, oil-driven inflation and market volatility make disciplined saving and diversified allocation more important, as energy cycles can disrupt both portfolio values and purchasing power. Working with a financial advisor can help you position your planning strategy for sustained energy price uncertainty.

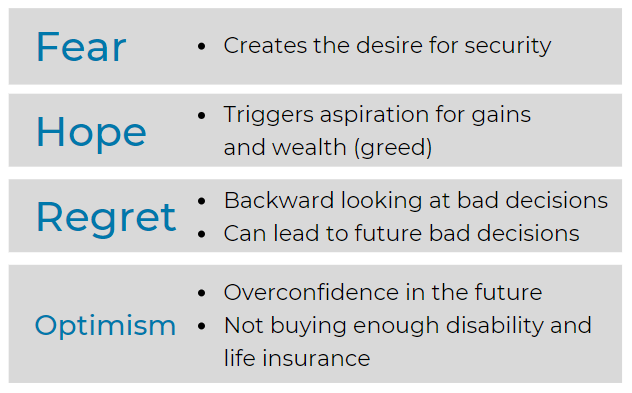

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

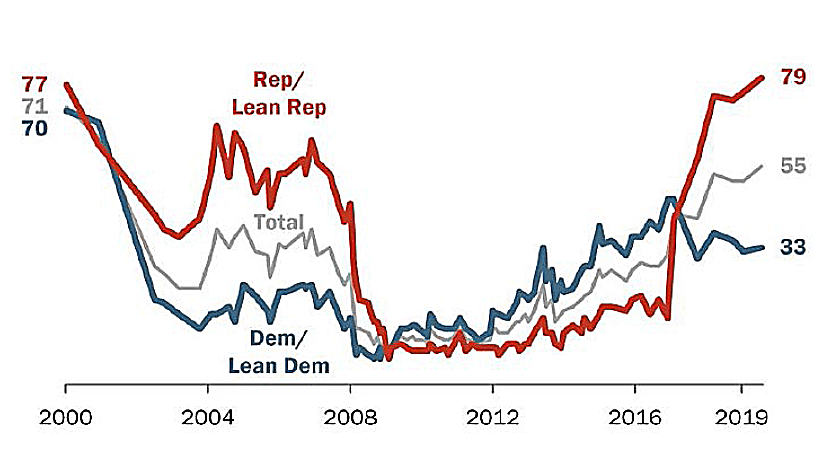

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how Rockwell's employer-sponsored benefits fit into the broader picture. According to publicly available information, Rockwell maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. Rockwell also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with Rockwell's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

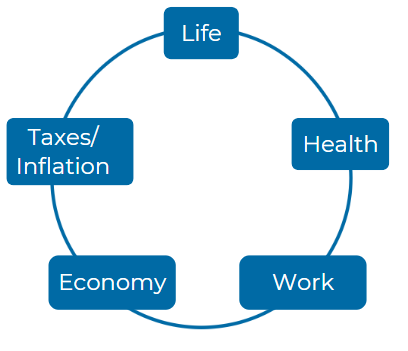

Consider these five Elements:

Â

Â

What retirement planning resources are available to employees of Rockwell Automation that can assist them in understanding their benefits upon retirement, specifically regarding the Pension Plan and Retirement Savings Plan? Discuss how Rockwell Automation provides these resources and the potential impact on an employee's financial security in retirement.

Retirement Planning Resources: Rockwell Automation provides several retirement planning resources to aid employees in understanding their Pension Plan and Retirement Savings Plan benefits. The company offers access to a pension calculator and detailed plan descriptions through their benefits portal. Additionally, employees can seek personalized advice from Edelman Financial Engines, which can guide on Social Security, pensions, and 401(k) management. These tools collectively help in maximizing retirement income, ensuring financial security.

In what ways does Rockwell Automation support employees who are transitioning to retirement to find appropriate health coverage, particularly for those who may be eligible for Medicare? Explore the relationship between Rockwell Automation's healthcare offerings and external resources like Via Benefits and how they assist retirees in navigating their healthcare options.

Health Coverage for Retiring Employees: Rockwell Automation supports transitioning employees by offering pre-65 retiree medical coverage and facilitating access to Via Benefits for those eligible for Medicare. This linkage ensures continuous healthcare coverage and aids retirees in navigating their options effectively. Via Benefits provides a platform to compare and select Medicare supplement plans, ensuring that retirees find coverage that best fits their medical and financial needs.

How does the retirement process affect the life insurance benefits that employees of Rockwell Automation currently hold? Investigate the various options available to retiring employees regarding their life insurance policies and the importance of planning for these changes to ensure adequate coverage post-retirement.

Life Insurance Benefits: Upon retirement, life insurance coverage through Rockwell Automation ends, but employees have options to convert or port their policies. This transition plan allows retirees to maintain necessary coverage and adapt their life insurance plans to meet their changing financial and familial obligations post-retirement, thus ensuring continued protection.

What considerations should Rockwell Automation employees take into account when planning the timing of their pension benefit elections, and how can this timing affect their retirement income? Discuss the implications of pension benefit timing on financial planning and the suggested practices by Rockwell Automation for making these decisions.

Pension Benefit Election Timing: The timing of pension benefit elections can significantly impact retirement income. Rockwell Automation provides resources to model different retirement scenarios using their pension calculator. Employees are advised to consider the timing of benefit elections carefully, as early or delayed starts impact the financial outcome, thereby affecting overall financial stability in retirement.

How can employees of Rockwell Automation estimate their Social Security benefits before retirement, and what tools or resources does Rockwell Automation provide to aid in this process? Delve into the importance of understanding Social Security benefits as part of an overall retirement strategy and how Rockwell Automation facilitates this understanding.

Estimating Social Security Benefits: Employees are encouraged to use resources provided by Rockwell Automation to estimate their Social Security benefits. The company offers tools and external advisory services, including consultations with Edelman Financial Engines through the company’s portal, which help in understanding how Social Security benefits integrate with other retirement income sources for a comprehensive retirement strategy.

What are the health care options available to Rockwell Automation employees who retire before reaching the age of 65, and how do these options differ from those available to employees who retire after age 65? Discuss the eligibility requirements and implications of choosing, or deferring, retiree medical coverage under Rockwell Automation's plans.

Health Care Options for Employees Retiring Before Age 65: Rockwell Automation offers distinct health care plans for employees retiring before age 65, with eligibility dependent on age and years of service. These plans provide substantial support by covering different medical needs until the retiree is eligible for Medicare, illustrating the company’s commitment to ensuring health coverage continuity for its workforce.

In what ways can Rockwell Automation employees effectively prepare for potential cash flow gaps when transitioning into retirement? Evaluate the financial planning strategies recommended by Rockwell Automation to minimize the stress associated with income disruption during this critical period.

Preparing for Cash Flow Gaps: Rockwell Automation addresses potential cash flow gaps during retirement transition through detailed planning resources. The company highlights the importance of budgeting and provides tools to estimate the timing and amounts of retirement benefits. This proactive approach helps employees manage their finances effectively during the transitional phase of retirement.

What resources does Rockwell Automation offer to help employees make informed decisions regarding their retirement income sources, including pensions, savings plans, and Social Security? Examine the tools and guidance supplied by the company and how these can impact the employee's financial readiness for retirement.

Informed Decisions on Retirement Income Sources: Rockwell Automation offers extensive resources, including workshops and personalized counseling through partners like Edelman Financial Engines, to help employees make informed decisions about their retirement income sources. This support is crucial in helping employees optimize their income streams from pensions, savings plans, and Social Security.

How do Rockwell Automation's retirement benefits differ based on an employee's years of service, and what implications do these differences have for planning a secure retirement? Analyze the various tiers of benefits and options available to long-term versus newer employees and the importance of understanding these differences.

Impact of Service Years on Retirement Benefits: The company’s retirement benefits vary with the length of service, affecting the retirement planning of both long-term and newer employees. This tiered benefit structure underscores the importance of understanding how service length impacts pension calculations and eligibility for other retirement benefits, guiding employees in their long-term financial planning.

How can employees contact Rockwell Automation to seek further information about the retirement benefits discussed in the retirement document? Specify the available channels for communication and the types of inquiries that can be addressed through these means, underscoring the company's commitment to supporting employees during the retirement process.

Seeking Further Information: Employees can contact the Rockwell Automation Service Center for further information about retirement benefits. The availability of detailed plan descriptions and direct access to retirement specialists via phone ensures that employees receive support tailored to their specific retirement planning needs, reinforcing the company's commitment to facilitating a smooth transition to retirement.

For more information you can reach the plan administrator for Rockwell at 1201 s 2nd st Milwaukee, WI 53204; or by calling them at 1-414-382-2000.

https://www.rockwellautomation.com/documents/pension-plan-2022.pdf - Page 5 https://www.rockwellautomation.com/documents/pension-plan-2023.pdf - Page 12 https://www.rockwellautomation.com/documents/pension-plan-2024.pdf - Page 15 https://www.rockwellautomation.com/documents/401k-plan-2022.pdf - Page 8 https://www.rockwellautomation.com/documents/401k-plan-2023.pdf - Page 22 https://www.rockwellautomation.com/documents/401k-plan-2024.pdf - Page 28 https://www.rockwellautomation.com/documents/rsu-plan-2022.pdf - Page 20 https://www.rockwellautomation.com/documents/rsu-plan-2023.pdf - Page 14 https://www.rockwellautomation.com/documents/rsu-plan-2024.pdf - Page 17 https://www.rockwellautomation.com/documents/healthcare-plan-2022.pdf - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.