New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for Southern California Edison Employees and Retirees

/General/General%203.png?width=1280&height=853&name=General%203.png)

With crude oil volatility near 80% and prices spanning $50 to $120 per barrel over the past six months, energy cost uncertainty influences economic conditions across industries. Fleet diesel costs and inflation-driven rate case pressures create indirect but meaningful exposure to sustained crude price swings. Southern California Edison employees building long-term savings should recognize that oil-driven economic conditions can affect both the growth of their portfolios and the purchasing power of their eventual retirement income. Consulting with a financial advisor can help you understand how energy conditions affect your specific situation and build a plan that adapts accordingly.

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

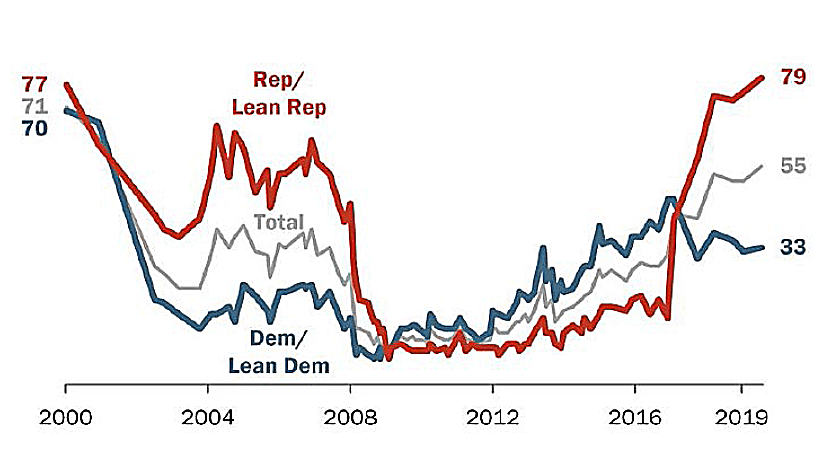

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how Southern California Edison's employer-sponsored benefits fit into the broader picture. According to publicly available information, Southern California Edison maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. Southern California Edison also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with Southern California Edison's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

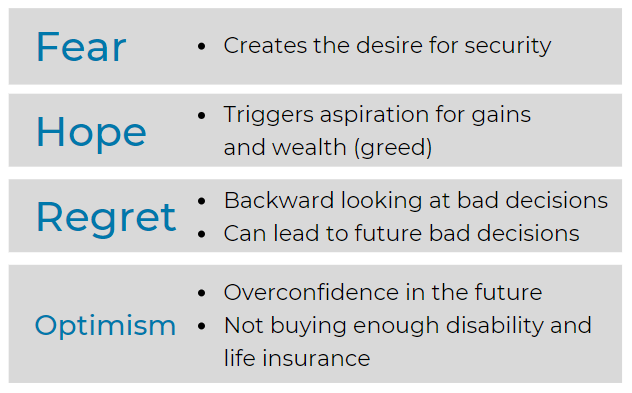

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

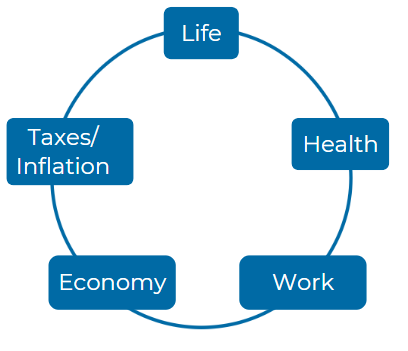

Consider these five Elements:

Â

Â

How does SoCalGas determine its pension contribution levels for 2024, and what factors influence the funding strategies to maintain financial stability? In preparing for the Test Year (TY) 2024, SoCalGas employs a detailed actuarial process to ascertain the necessary pension contributions. The actuarial valuation includes an assessment of the company's Projected Benefit Obligation (PBO) under Generally Accepted Accounting Principles (GAAP). These calculations incorporate variables such as current employee demographics, expected retirement ages, and market conditions. Additionally, SoCalGas must navigate external economic factors, including interest rates and economic forecasts, which can impact the funded status of its pension plans and the associated financial obligations.

SoCalGas determines its pension contribution levels using a detailed actuarial process that evaluates the Projected Benefit Obligation (PBO) under Generally Accepted Accounting Principles (GAAP). The contribution is influenced by variables such as employee demographics, retirement age expectations, market conditions, and external economic factors like interest rates and economic forecasts. SoCalGas maintains financial stability by adjusting funding strategies based on market returns and required amortization periods(Southern_California_Gas…).

What specific changes to SoCalGas's pension plan are being proposed for the upcoming fiscal year, and how will these changes impact existing employees and retirees? The proposals for the TY 2024 incorporate adjustments to the existing pension funding mechanisms, including the continuation of the two-way balancing account to account for fluctuations in pension costs. This measure is designed to stabilize funding while meeting both the service cost and the annual minimum contributions required under regulatory standards. Existing employees and retirees may see changes in their benefits as adjustments are made to align with these funding strategies, which may include modifications to expected payouts or contributions required from retirees depending on their service years and retirement age.

For the 2024 Test Year, SoCalGas is proposing to adjust its pension funding policy by shortening the amortization period for the PBO shortfall from fourteen to seven years. This change aims to fully fund the pension plan more quickly, improving long-term financial health while reducing intergenerational ratepayer burden. Existing employees and retirees may experience greater financial stability in the pension plan due to these proactive funding strategies(Southern_California_Gas…).

In what ways does SoCalGas's health care cost escalation projections for postretirement benefits compare with national trends, and what strategies are in place to manage these costs? The health care cost escalations required for the Postretirement Health and Welfare Benefits Other than Pension (PBOP) at SoCalGas have been developed in alignment with industry trends, which show consistent increases in health care expenses across the nation. Strategies implemented by SoCalGas involve negotiation with health care providers for favorable rates, introduction of health reimbursement accounts (HRAs), and ongoing assessments of utilization rates among retirees to identify potential savings. These measures aim to contain costs while ensuring that retirees maintain access to necessary healthcare services without a significant financial burden.

SoCalGas's healthcare cost projections for its Postretirement Benefits Other than Pensions (PBOP) align with national trends of increasing healthcare expenses. To manage these costs, SoCalGas employs strategies like negotiating favorable rates with providers, utilizing health reimbursement accounts (HRAs), and regularly assessing healthcare utilization. These efforts aim to control healthcare costs while ensuring that retirees receive necessary care(Southern_California_Gas…).

What resources are available to SoCalGas employees to help them understand their benefits and the changes that may occur in 2024? SoCalGas provides various resources to employees to clarify their benefits and upcoming changes, including dedicated HR representatives, comprehensive guides on benefits options, web-based portals, and informational seminars. Employees can access personalized accounts to view their specific benefits, contributions, and projections. Additionally, the company offers regular training sessions covering changes in benefits and how to navigate the retirement process effectively, empowering employees to make informed decisions regarding their retirement planning.

SoCalGas provides employees with various resources, including HR representatives, benefit guides, and web-based portals to help them understand their benefits. Employees also have access to personalized retirement accounts and training sessions that cover benefit changes and retirement planning, helping them make informed decisions regarding their future(Southern_California_Gas…).

How does the PBOP plan impact SoCalGas’s overall compensation strategy for attracting talent? The PBOP plan is a critical component of SoCalGas’s total compensation strategy, designed to attract and retain high-caliber talent in an increasingly competitive market. SoCalGas recognizes that comprehensive postretirement benefits enhance their appeal as an employer. The direct correlation between competitive benefits packages, including the PBOP plan's provisions for health care coverage and financial support during retirement, plays a significant role in talent acquisition and retention by providing peace of mind for employees about their long-term financial security.

SoCalGas's PBOP plan plays a crucial role in its overall compensation strategy by offering competitive postretirement health benefits that enhance the attractiveness of the company's total compensation package. This helps SoCalGas attract and retain a high-performing workforce, as comprehensive retirement and healthcare benefits are important factors for employees when choosing an employer(Southern_California_Gas…).

What are the anticipated trends in the pension and postretirement cost estimates for SoCalGas from 2024 through 2031, and what implications do these trends hold for financial planning? Anticipated trends in pension and postretirement cost estimates are projected to indicate gradual increases in these costs due to changing demographics, increasing life expectancies, and inflation impacting healthcare costs. Financial planning at SoCalGas thus necessitates a proactive approach to ensure adequate funding mechanisms are in place. This involves forecasting contributions that will remain in line with the projected obligations while also navigating regulatory requirements to avoid potential funding shortfalls or impacts on corporate finances.

SoCalGas anticipates gradual increases in pension and postretirement costs from 2024 to 2031 due to changing demographics, increased life expectancies, and rising healthcare costs. This trend implies that SoCalGas will need to implement robust financial planning strategies, including forecasting contributions and aligning funding mechanisms with regulatory requirements to avoid potential shortfalls(Southern_California_Gas…).

How do SoCalGas's pension plans compare with those offered by other utility companies in California in terms of competitiveness and sustainability? When evaluating SoCalGas's pension plans compared to other California utility companies, it becomes evident that SoCalGas's offerings emphasize not only competitive benefits but also a sustainable framework for its pension obligations. This comparative analysis includes studying funding ratios, benefit structures, and employee satisfaction levels. SoCalGas aims to maintain a robust pension plan that not only meets current employee needs but is also sustainable in the long term, adapting to changing economic conditions and workforce requirements while remaining compliant with state regulations.

SoCalGas's pension plans are competitive with those of other utility companies in California, with a focus on both benefit structure and long-term sustainability. SoCalGas emphasizes maintaining a robust pension plan that is adaptable to changing market conditions, regulatory requirements, and workforce needs. This allows the company to remain an attractive employer while ensuring the sustainability of its pension commitments(Southern_California_Gas…).

How can SoCalGas employees reach out for support regarding their pension and retirement benefits, and what types of inquiries can they make? Employees can contact SoCalGas’s Human Resources Benefits Department through dedicated communication channels such as the company’s HR support line, email, or scheduled one-on-one consultations. The HR team is trained to address a variety of inquiries related to pension benefits, eligibility requirements, plan options, and retirement planning strategies. Moreover, employees can request personalized benefits statements and assistance with understanding their entitlements and the implications of any regulatory changes affecting their plans.

SoCalGas employees can reach out to the company's HR Benefits Department through a dedicated support line, email, or consultations. They can inquire about pension benefits, eligibility, plan options, and retirement strategies. Employees may also request personalized benefits statements and clarification on regulatory changes that may affect their plans(Southern_California_Gas…).

What role does market volatility and economic conditions play in shaping the funding strategy of SoCalGas's pension plans? Market volatility and economic conditions play a significant role in shaping SoCalGas's pension funding strategy, influencing both asset returns and liabilities. Fluctuations in interest rates, market performance of invested pension assets, and changes in demographic factors directly affect the PBO calculation, requiring SoCalGas to adjust its funding strategy responsively. This involved the use of sophisticated financial modeling and scenario analysis to ensure that the pension plans remain adequately funded and financially viable despite adverse economic conditions, thereby protecting the interests of current and future beneficiaries.

Market volatility and economic conditions significantly impact SoCalGas's pension funding strategy, affecting both asset returns and liabilities. Factors like interest rates, market performance of pension assets, and demographic shifts influence the PBO calculation, prompting SoCalGas to adjust its funding strategy to ensure adequate pension funding and long-term plan viability(Southern_California_Gas…).

What steps have SoCalGas and SDG&E proposed to recover costs related to pension and PBOP to alleviate financial pressure on ratepayers? SoCalGas and SDG&E proposed implementing a two-way balancing account mechanism designed to smoothly recover the costs associated with their pension and PBOP plans. This initiative aims to ensure that any variances between projected and actual contributions are adjusted in a timely manner, thereby reducing the financial burden on ratepayers. By utilizing this approach, the Companies seek to maintain stable rates while ensuring that all pension obligations can be met without compromising operational integrity or service delivery to their customers. These questions reflect complex issues relevant to SoCalGas employees preparing for retirement and navigating the nuances of their benefits.

SoCalGas and SDG&E have proposed utilizing a two-way balancing account mechanism to recover pension and PBOP-related costs. This mechanism helps adjust for variances between projected and actual contributions, ensuring that costs are managed effectively and do not overly burden ratepayers. This approach aims to maintain stable rates while fulfilling pension obligations(Southern_California_Gas…).

For more information you can reach the plan administrator for Southern California Edison at 2244 walnut grove ave Rosemead, CA 91770; or by calling them at 1-800-655-4555.

https://www6.lifeatworkportal.com/slogin/edison/pdf/GY5_H12_H20_2024_Benefits_Enrollment_Guide_Flex.pdf - Page 5, https://www6.lifeatworkportal.com/slogin/edison/pdf/GY5_H12_H20_2023_Benefits_Enrollment_Guide_Flex.pdf - Page 12, https://www6.lifeatworkportal.com/slogin/edison/pdf/GY5_H12_H20_2022_Benefits_Enrollment_Guide_Flex.pdf - Page 15, https://docs.cpuc.ca.gov/PublishedDocs/Efile/G000/M441/K519/441519282.PDF - Page 8, https://www.edison.com/content/dam/eix/documents/investors/corporate-governance/2023-governance-documents.pdf - Page 22, https://www.edison.com/content/dam/eix/documents/investors/corporate-governance/2024-governance-documents.pdf - Page 28, https://www.edison.com/content/dam/eix/documents/investors/corporate-governance/2022-governance-documents.pdf - Page 20, https://docs.cpuc.ca.gov/PublishedDocs/Efile/G000/M385/K633/385633681.PDF - Page 14, https://docs.cpuc.ca.gov/PublishedDocs/Efile/G000/M398/K742/398742219.PDF - Page 17, https://docs.cpuc.ca.gov/PublishedDocs/Efile/G000/M407/K568/407568792.PDF - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.