New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for The Boeing Company Employees and Retirees

/General/General%2013.png?width=1280&height=853&name=General%2013.png)

Energy market instability persists, with crude prices fluctuating between $50 and $120 per barrel and annualized volatility running around 80%. The effects reach well beyond the energy sector. Jet fuel costs, petrochemical composite materials, and fixed-price contract structures mean elevated crude prices create margin pressure across the aerospace supply chain. For The Boeing Company employees building retirement savings, oil-driven inflation and market volatility make disciplined saving and diversified allocation more important, as energy cycles can disrupt both portfolio values and purchasing power. Professional guidance can help you navigate the indirect effects of oil volatility on your retirement planning and ensure your strategy accounts for these dynamics.

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

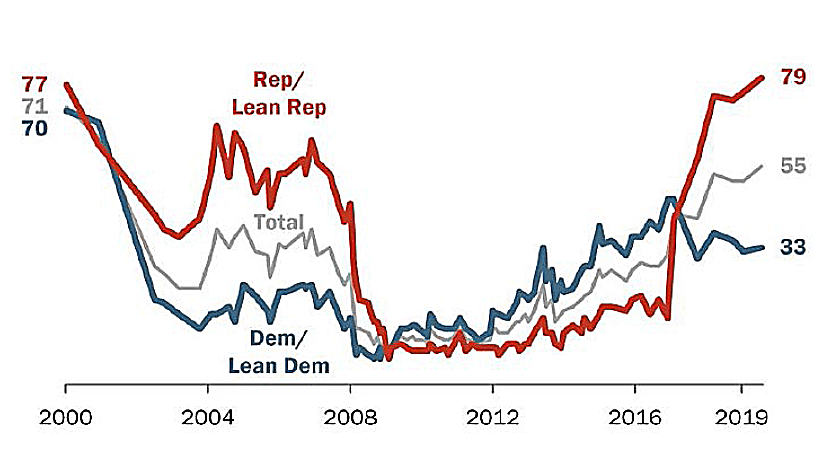

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how The Boeing Company's employer-sponsored benefits fit into the broader picture. According to publicly available information, The Boeing Company maintains an active defined benefit pension plan, which provides retirement income based on factors such as years of service and compensation history. The Boeing Company also offers retiree healthcare benefits to eligible employees, which can provide meaningful coverage for those who retire before reaching Medicare eligibility at age 65. Because the specifics of your pension formula, vesting schedule, and benefit eligibility depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with The Boeing Company's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

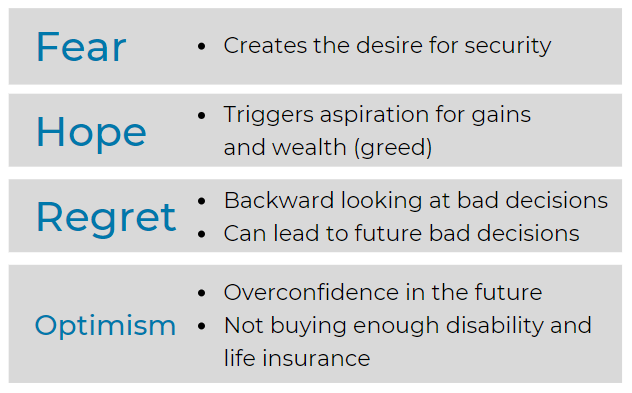

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

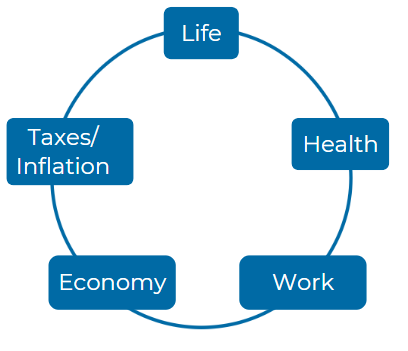

Consider these five Elements:

Â

Â

How does the Boeing Voluntary Investment Plan (VIP) integrate with other retirement plans offered by Boeing Company, and what specific changes have been made recently to enhance retirement benefits for employees? Discuss the implications these changes might have on employees planning their retirement.

The Boeing Voluntary Investment Plan (VIP) integrates with other Boeing retirement plans, such as the Boeing Pension Value Plan and other defined benefit plans. Recently, changes like the addition of a Roth contribution option and a shift toward enhanced defined contributions have been made to improve benefits for certain employees, particularly those who previously participated in both defined benefit and defined contribution plans. These changes enhance retirement planning flexibility but may require employees to adjust their strategies depending on their long-term financial goals.

What are the key eligibility requirements for participation in the Boeing Voluntary Investment Plan, and how do these requirements align with industry standards for retirement plans within large corporations? Specifically, address how the eligibility criteria impact various groups of employees within Boeing Company.

Key eligibility requirements for the Boeing VIP include no minimum age or service requirements, though certain groups, such as union employees and non-resident aliens, may be excluded. These criteria align with industry standards, making the plan accessible to a broad range of employees. The inclusivity of eligibility supports employees at various career stages, though exclusions may affect unionized employees or contractors differently from their non-union counterparts(Boeing_Voluntary_Invest…).

In what ways does the Boeing Voluntary Investment Plan support employees who wish to make catch-up contributions, particularly for those nearing retirement age? Examine the financial benefits and potential challenges associated with these contributions for Boeing employees.

Boeing VIP allows catch-up contributions for employees aged 50 and over, aligning with IRS guidelines for retirement savings. This option benefits employees nearing retirement by enabling them to contribute more toward their savings. However, the increased financial burden of larger contributions could pose a challenge for employees with tighter budgets, potentially limiting their ability to maximize catch-up contributions(Boeing_Voluntary_Invest…).

How does the investment allocation strategy within the Boeing Voluntary Investment Plan reflect the principles of risk management and diversification? Evaluate the types of investment options available and their relevance for Boeing employees planning for retirement.

The investment strategy of Boeing VIP emphasizes risk management and diversification, offering a wide range of options, including lifecycle funds, index funds, and company stock. These choices provide flexibility for employees with varying risk tolerances, helping them manage retirement savings effectively. The availability of different fund types ensures that employees can align their investment choices with their retirement timelines and risk preferences(Boeing_Voluntary_Invest…).

What options does the Boeing Voluntary Investment Plan provide for loans and withdrawals, and how do these options affect employees’ financial planning? Analyze the conditions under which Boeing employees can access their funds and the implications of these conditions on long-term retirement savings.

Boeing VIP offers loans and withdrawal options, including hardship withdrawals and in-service distributions at age 59½. These features provide flexibility in accessing retirement funds but come with conditions that could affect long-term savings. For example, taking a loan or withdrawal may reduce the funds available for retirement and may lead to penalties, making it important for employees to carefully consider the implications before accessing their funds(Boeing_Voluntary_Invest…).

How can Boeing employees effectively utilize the resources available through the Boeing Retirement Service Center to optimize their retirement planning? Discuss the types of support services provided and how they can aid employees in making informed decisions regarding their retirement benefits.

Boeing employees can utilize resources through the Boeing Retirement Service Center, which provides support for retirement planning. The center offers tools, counseling, and online resources to help employees understand their options and optimize their benefits. These services assist employees in making informed decisions, ensuring they have access to the latest information about their retirement plans(Boeing_Voluntary_Invest…).

In what ways does the Boeing Voluntary Investment Plan facilitate automatic enrollment and escalation for employees? Assess the impact of these features on employee participation rates and retirement savings at Boeing Company.

Automatic enrollment and escalation features in the Boeing VIP encourage higher participation rates and increased savings. Employees are automatically enrolled at 4% pre-tax contributions, with an option for annual increases of 1% up to 8%. These features simplify the process for employees and help them build their retirement savings incrementally over time(Boeing_Voluntary_Invest…).

How does Boeing Company ensure that its pension and retirement plans remain compliant with current IRS regulations and requirements? Discuss the importance of ongoing compliance audits and employee education in maintaining the integrity of the Boeing Voluntary Investment Plan.

Boeing ensures compliance with IRS regulations by regularly updating its plans and conducting compliance audits. Maintaining adherence to regulations is essential for protecting the plan's tax-qualified status, and Boeing also focuses on employee education to ensure they understand the requirements and benefits of the plan(Boeing_Voluntary_Invest…).

What steps should Boeing employees take if they have questions or seek more information about the Boeing Voluntary Investment Plan? Outline the available channels for communication and the types of inquiries that can be directed to Boeing's human resources department.

Boeing employees with questions about the VIP can contact the Boeing Retirement Service Center or their human resources department. These channels provide assistance with inquiries related to plan features, contributions, and withdrawals, offering personalized guidance to help employees manage their retirement planning effectively(Boeing_Voluntary_Invest…).

How does the recent shift from traditional defined-benefit pensions to a defined-contribution model, as seen in the Boeing Voluntary Investment Plan, influence the financial security of future retirees from Boeing? Explore the long-term effects this transition may have on employee savings behavior and retirement readiness.

The shift from traditional defined-benefit pensions to a defined-contribution model, like the Boeing VIP, changes the way employees plan for retirement. Employees are now more responsible for managing their own investments and savings, which may lead to varying levels of financial security depending on their decisions. This transition emphasizes the need for employees to be more proactive in their retirement planning to ensure they meet their long-term financial goals(Boeing_Voluntary_Invest…).

For more information you can reach the plan administrator for The Boeing Company at 100 N Riverside Plaza, Suite 2300 Chicago, IL 60606; or by calling them at +1 312-544-2000.

https://www.boeing.com/docs/benefits/pension_plan2023.pdf - Page 11 https://www.boeing.com/docs/benefits/401k_plan2024.pdf - Page 14 https://www.boeing.com/docs/benefits/rsu_plan2022.pdf - Page 16 https://www.boeing.com/docs/benefits/stock_options2023.pdf - Page 22 https://www.boeing.com/docs/benefits/healthcare2024.pdf - Page 25 https://www.boeing.com/docs/benefits/annual_report2023.pdf - Page 35 https://www.boeing.com/docs/benefits/employee_handbook2022.pdf - Page 40 https://www.boeing.com/docs/benefits/retirement_guide2023.pdf - Page 12 https://www.boeing.com/docs/benefits/benefit_highlights2024.pdf - Page 37 https://www.boeing.com/docs/benefits/benefit_summary2023.pdf - Page 29

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.