New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for University of California Employees and Retirees

/General/General%208.png?width=1280&height=853&name=General%208.png)

Oil market turbulence continues to ripple through the broader economy, with crude swinging between $50 and $120 per barrel and annualized volatility near 80%. Oil price volatility ripples through the broader economy by influencing inflation expectations, interest rates, and equity market valuations. For employees at University of California, energy sector holdings within retirement accounts, such as oil stocks in a 401(k), can experience significant price swings that affect portfolio allocation; if sold during downturns, realized losses or gains may create unexpected tax consequences. For University of California employees building retirement savings, oil-driven inflation and market volatility make disciplined saving and diversified allocation more important, as energy cycles can disrupt both portfolio values and purchasing power. In this environment, a financial advisor can help you assess your exposure to oil-driven economic effects and build appropriately diversified strategies.

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

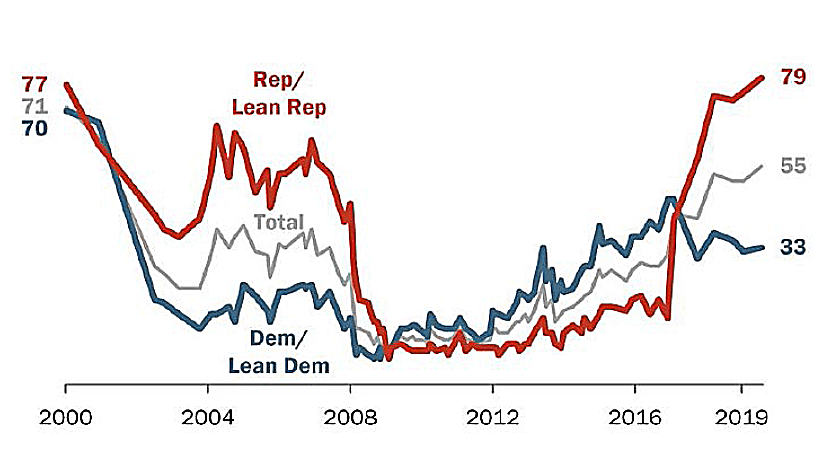

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how University of California's employer-sponsored benefits fit into the broader picture. According to publicly available information, University of California does not maintain a traditional defined benefit pension plan, making your 401(k) plan and personal savings the primary vehicles for retirement income. University of California does not appear to offer a formal retiree healthcare program, so healthcare coverage planning before Medicare eligibility at age 65 is an important consideration. We encourage you to review your Summary Plan Description (SPD) or speak with University of California's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

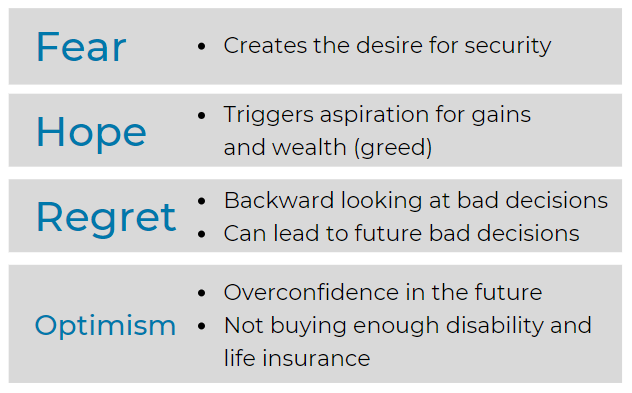

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

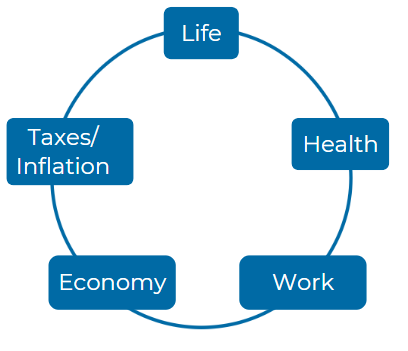

Consider these five Elements:

Â

Â

How does the University of California Retirement Plan (UCRP) define service credit for members, and how does it impact retirement benefits? In what ways can University of California employees potentially enhance their service credit, thereby influencing their retirement income upon leaving the University of California?

Service Credit in UCRP: Service credit is essential in determining retirement eligibility and the amount of retirement benefits for University of California employees. It is based on the period of employment in an eligible position and covered compensation during that time. Employees earn service credit proportionate to their work time, and unused sick leave can convert to additional service credit upon retirement. Employees can enhance their service credit through methods like purchasing service credit for unpaid leaves or sabbatical periods(University of Californi…).

Regarding the contribution limits for the University of California’s defined contribution plans, how do these limits for 2024 compare to previous years, and what implications do they have for current employees of the University of California in their retirement planning strategies? How can understanding these limits lead University of California employees to make more informed decisions about their retirement savings?

Contribution Limits for UC Defined Contribution Plans in 2024: Contribution limits for defined contribution plans, such as the University of California's DC Plan, often adjust yearly due to IRS regulations. Increases in these limits allow employees to maximize their retirement savings. For 2024, employees can compare the current limits with previous years to understand how much they can contribute tax-deferred, potentially increasing their long-term savings and tax advantages(University of Californi…).

What are the eligibility criteria for the various death benefits associated with the University of California Retirement Plan? Specifically, how does being married or in a domestic partnership influence the eligibility of beneficiaries for University of California employees' retirement and survivor benefits?

Eligibility for UCRP Death Benefits: Death benefits under UCRP depend on factors like length of service, eligibility to retire, and marital or domestic partnership status. Being married or in a registered domestic partnership allows a spouse or partner to receive survivor benefits, which might include lifetime income. In some cases, other beneficiaries like children or dependent parents may be eligible(University of Californi…).

In the context of retirement planning for University of California employees, what are the tax implications associated with rolling over benefits from their defined benefit plan to an individual retirement account (IRA)? How do these rules differ depending on whether the employee chooses a direct rollover or receives a distribution first before rolling it over into an IRA?

Tax Implications of Rolling Over UCRP Benefits: Rolling over benefits from UCRP to an IRA can offer tax advantages. A direct rollover avoids immediate taxes, while receiving a distribution first and rolling it into an IRA later may result in withholding and potential penalties. UC employees should consult tax professionals to ensure they follow the IRS rules that suit their financial goals(University of Californi…).

What are the different payment options available to University of California retirees when selecting their retirement income, and how does choosing a contingent annuitant affect their monthly benefit amount? What factors should University of California employees consider when deciding on the best payment option for their individual financial situations?

Retirement Payment Options: UC retirees can choose from various payment options, including a single life annuity or joint life annuity with a contingent annuitant. Selecting a contingent annuitant reduces the retiree's monthly income but provides benefits for another person after their death. Factors like age, life expectancy, and financial needs should guide this decision(University of Californi…).

What steps must University of California employees take to prepare for retirement regarding their defined contribution accounts, and how can they efficiently consolidate their benefits? In what ways does the process of managing multiple accounts influence the overall financial health of employees during their retirement?

Preparation for Retirement: UC employees nearing retirement must evaluate their defined contribution accounts and consider consolidating their benefits for easier management. Properly managing multiple accounts ensures they can maximize their income and minimize fees, thus contributing to their financial health during retirement(University of Californi…).

How do the rules around capital accumulation payments (CAP) impact University of California employees, and what choices do they have regarding their payment structures upon retirement? What considerations might encourage a University of California employee to opt for a lump-sum cashout versus a traditional monthly pension distribution?

Capital Accumulation Payments (CAP): CAP is a supplemental benefit that certain UCRP members receive upon leaving the University. UC employees can choose between a lump sum cashout or a traditional monthly pension. Those considering a lump sum might prefer immediate access to funds, but the traditional option offers ongoing, stable income(University of Californi…)(University of Californi…).

As a University of California employee planning for retirement, what resources are available for understanding and navigating the complexities of the retirement benefits offered? How can University of California employees make use of online platforms or contact university representatives for personalized assistance regarding their retirement plans?

Resources for UC Employees' Retirement Planning: UC offers extensive online resources, such as UCnet and UCRAYS, where employees can manage their retirement plans. Personalized assistance is also available through local benefits offices and the UC Retirement Administration Service Center(University of Californi…).

What unique challenges do University of California employees face with regard to healthcare and retirement planning, particularly in terms of post-retirement health benefits? How do these benefits compare to other state retirement systems, and what should employees of the University of California be aware of when planning for their medical expenses after retirement?

Healthcare and Retirement Planning Challenges: Post-retirement healthcare benefits are crucial for UC employees, especially as healthcare costs rise. UC’s retirement health benefits offer significant support, often more comprehensive than other state systems. However, employees should still prepare for potential gaps and rising costs in their post-retirement planning(University of Californi…).

How can University of California employees initiate contact to learn more about their retirement benefits, and what specific information should they request when reaching out? What methods of communication are recommended for efficient resolution of inquiries related to their retirement plans within the University of California system?

Contacting UC for Retirement Information: UC employees can contact the UC Retirement Administration Service Center for assistance with retirement benefits. It is recommended to request information on service credits, pension benefits, and health benefits. Communication via the UCRAYS platform ensures secure and efficient resolution of inquiries(University of Californi…).

For more information you can reach the plan administrator for University of California at 9500 gilman dr La Jolla, CA 92093; or by calling them at 858-534-2230.

https://www.ucop.edu/ucpath-center/_files/2022-benefits-fair/2022-summary-benefits.pdf - Page 5, https://www.ucop.edu/ucpath-center/_files/2023-benefits-fair/2023-summary-benefits.pdf - Page 12, https://www.ucop.edu/ucpath-center/_files/2024-benefits-fair/2024-summary-benefits.pdf - Page 15, https://www.ucop.edu/ucpath-center/_files/401k-plan-2022.pdf - Page 8, https://www.ucop.edu/ucpath-center/_files/401k-plan-2023.pdf - Page 22, https://www.ucop.edu/ucpath-center/_files/401k-plan-2024.pdf - Page 28, https://www.ucop.edu/ucpath-center/_files/rsu-plan-2022.pdf - Page 20, https://www.ucop.edu/ucpath-center/_files/rsu-plan-2023.pdf - Page 14, https://www.ucop.edu/ucpath-center/_files/rsu-plan-2024.pdf - Page 17, https://www.ucop.edu/ucpath-center/_files/healthcare-plan-2022.pdf - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.