/General/General%202.png?width=1280&height=853&name=General%202.png)

Selling During a Decline is a Risky Proposition

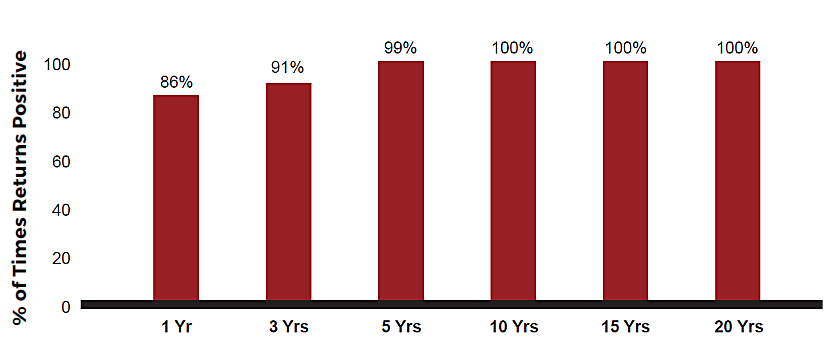

A Balanced Portfolio's Risk of Negative Long-term Returns Has Historically Been Relatively Low

Unpredictability Produces Opportunity

Market Volatility Can Help You Rebalance Your Portfolio

Ask the most experienced investors, and many will tell you that drastic allocation shifts in an effort to time the ups and downs of the market are immensely challenging.

As much as any investor would like to avoid market downturns and take advantage of rallies, to do so means getting out at the right time and knowing exactly when to get back in. Without a crystal ball, those are difficult calls to make with potentially adverse effects on your portfolio. Since no market cycle is the same, it isn't easy to anticipate market movements. All sorts of factors—politics, monetary policy, business activities (such as corporate mergers), and sudden international shocks (such as the global pandemic in 2020, the oil-price shock in the 1970s, and the tech bubble in the early 2000s)—can spark a market reaction.

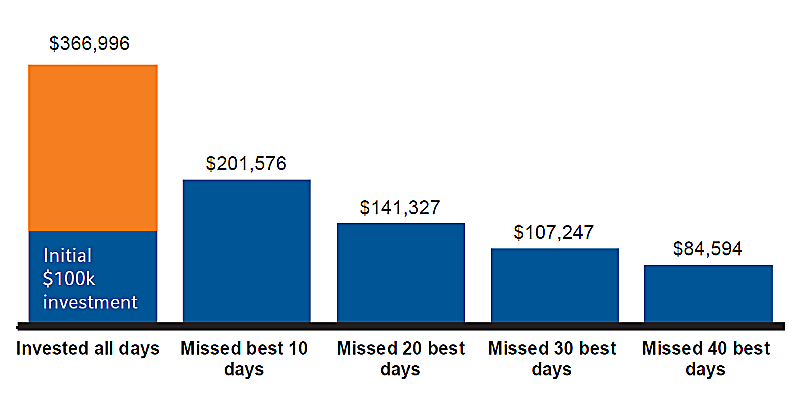

If your timing isn't perfectly accurate, you could miss out on potential rallies, which are virtually impossible to predict. The chart below shows that missing even a few days of positive market activity can impact your portfolio.

Featured Video

Articles you may find interesting:

- 8 Tenets of Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Section 303 Stock Redemption Buy-Sell Agreement

- Medicare Open Enrollment Is Here: How Are Costs Changing for 2023?

- 2022 High Net Worth Tax Planning

- Policy Roadmap

- Section 179 Deductions

- Learn About the Path to Retirement

- Contemplating Change: 7 Key Factors When Considering a Transition from Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Advice for Retirees Trying to Survive a Bear Market

- 5 Most Important Things to do Before Leaving Your Company

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- 8 Tenets of Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Section 303 Stock Redemption Buy-Sell Agreement

- Medicare Open Enrollment Is Here: How Are Costs Changing for 2023?

- 2022 High Net Worth Tax Planning

- Policy Roadmap

- Section 179 Deductions

- Learn About the Path to Retirement

- Contemplating Change: 7 Key Factors When Considering a Transition from Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Advice for Retirees Trying to Survive a Bear Market

- 5 Most Important Things to do Before Leaving Your Company

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

History suggests that periods of sharp declines have often been followed by periods of some of the most favorable returns. Figure 1 shows the strong returns of U.S. markets during the 12- and 24-month periods following some of the sharpest declines of the past 40+ years. The strong historical tendency of markets to rebound provides some evidence that fear-induced dramatic alterations to asset allocation are unnecessary for investors who simply stay the course.

Stocks have historically outperformed bonds when based on average rolling returns over one, three, five, 10, and 20 years. Just as compelling is the traditional ability of a balanced portfolio to produce positive returns. Figure 2 shows that a global balanced portfolio of stocks and bonds has not produced a negative return over any five-year rolling period since 1980. The bottom line is that, although there are no guarantees that the future will resemble the past, history tends to favor long-term investors.

Figure 2: A highly diversified portfolio has performed well over time

% Of time diversified 60/40 mix produced positive returns (Based on rolling returns, January 1980 - December 2020)

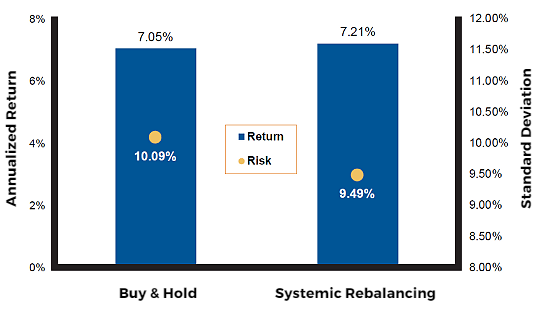

If a crisis creates an opportunity, then portfolio rebalancing is perhaps the best way to take advantage of that opportunity. When comparing assets within a portfolio, rebalancing means selling assets that have gained in value and buying assets that have fallen in value in order to maintain the overall strategic asset allocation of a diversified portfolio. During a market correction, this should result in buying more assets that have decreased in value—an essential part of the process of buying low and selling high.

As Figure 3 highlights, an asset allocation that is systematically rebalanced has produced a modest return advantage, but more importantly, has managed risk over time. Systematic portfolio rebalancing is a crucial aspect of Russell Investments’ portfolio approach. In essence, it provides investors with increased exposure to opportunities that are likely to pay off in the long run.

Figure 3: Rebalancing Vs. Buy & Hold

Potential benefits of hypothetical rebalancing comparison of $500,000

For illustrative purposes only. Not meant to represent any actual investment. Standard deviation is a statistical measure of the degree to which an individual value in a probability distribution tends to vary from the mean of the distribution. The greater the degree of dispersion, the greater the risk. Based on March 2005–December 2020. Source Portfolio: Diversified portfolio consists of 30% U.S. large cap, 5% U.S. small cap, 15% non-U.S. developed, 5% emerging markets, 5% REITs, and 40% fixed income. Returns are based on the following indices: U.S. large cap = Russell 1000 Index; U.S. small cap = Russell 2000 Index; non-U.S. developed = MSCI EAFE Index; emerging markets = MSCI Emerging Markets Index; REITS = FTSE EPRA/NAREIT Developed Index; and fixed income = Bloomberg Barclays U.S. Aggregate Bond Index. Start date corresponds to index start dates (January 1988 is the inception of the MSCI Emerging Markets Index).

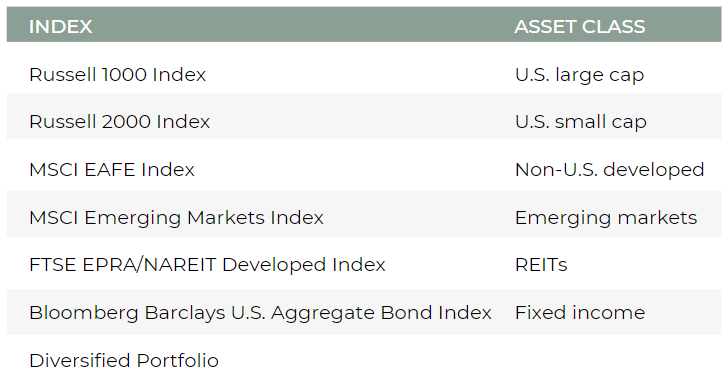

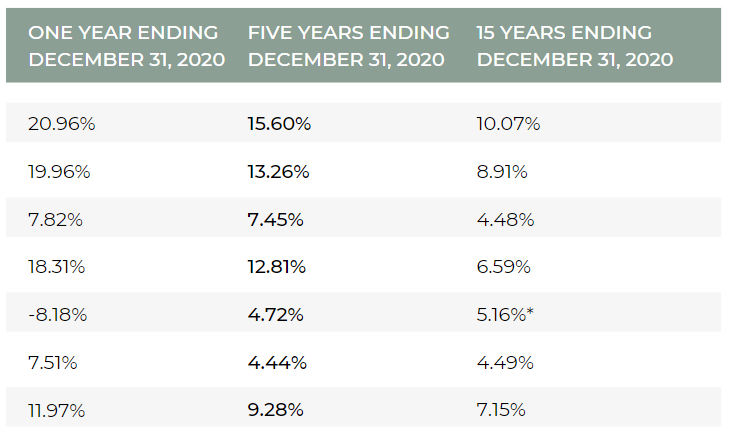

Over time, financial markets deal with numerous crises. To name a few over the last two decades, there was the technology bubble, a credit bubble, the U.S. subprime debt crisis, the sovereign debt crisis in the Eurozone, and the economic impact of the restrictive measures governments around the world have taken in early 2020, attempting to contain the spread of the novel coronavirus COVID-19. One reason to hold a multi-asset portfolio is in part to spread the risk budget across multiple asset classes in order to mitigate market volatility. Having a robust strategic asset allocation with regular rebalancing can potentially enhance returns, but more importantly, manage volatility. However, from a multi-asset investors’ perspective, longer-term returns have been reasonable. For example, the hypothetical globally diversified asset allocation in Table 1 shows solid returns over the long term.

Table 1: Benefits of Diversification – Annualized Returns

Note: Diversified portfolio consists of 30% U.S. large-cap, 5% U.S. small cap, 15% non-U.S. developed, 5% emerging markets, 5% REITs, and 40% fixed income. *The 15-year return of this index is a blended return using FTSE NAREIT Equity REITs TR USD Index through 2/17/2005 and FTSE EPRA/NAREIT Developed Index starting on 2/18/2005. Based on the respective rolling periods. Indexes are unmanaged and cannot be invested in directly. Past performance is not indicative of future results.

Other Articles of Interest

Articles Relevant to Target Employees

-

-

8 Tenets of Choosing a Mutual Fund -

Use of Escrow Accounts: Divorce -

Section 303 Stock Redemption Buy-Sell Agreement -

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

Medicare Open Enrollment Is Here: How Are Costs Changing for 2023? -

2022 High Net Worth Tax Planning -

Policy Roadmap -

Section 179 Deductions -

Learn About the Path to Retirement -

Contemplating Change: 7 Key Factors When Considering a Transition from Your Company -

How Are Workers Impacted by Inflation & Rising Interest Rates? -

Lump-Sum vs Annuity and Rising Interest Rates -

Advice for Retirees Trying to Survive a Bear Market -

5 Most Important Things to do Before Leaving Your Company -

Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

-

8 Tenets of Choosing a Mutual Fund -

Use of Escrow Accounts: Divorce -

Section 303 Stock Redemption Buy-Sell Agreement -

Medicare Open Enrollment Is Here: How Are Costs Changing for 2023? -

2022 High Net Worth Tax Planning -

Policy Roadmap -

Section 179 Deductions -

Learn About the Path to Retirement -

Contemplating Change: 7 Key Factors When Considering a Transition from Your Company -

How Are Workers Impacted by Inflation & Rising Interest Rates? -

Lump-Sum vs Annuity and Rising Interest Rates -

Advice for Retirees Trying to Survive a Bear Market -

5 Most Important Things to do Before Leaving Your Company -

Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

For more information you can reach the plan administrator for Target at 10 South Dearborn Street 48th Floor Chicago, IL 60603; or by calling them at 1-800-440-0680.

Company:

Target*

Plan Administrator:

10 South Dearborn Street 48th Floor

Chicago, IL

60603

1-800-440-0680

*Please see disclaimer for more information

Featured Articles

Articles Relevant to Target Employees

-

-

8 Tenets of Choosing a Mutual Fund

8 Tenets of Choosing a Mutual Fund

-

Use of Escrow Accounts: Divorce

Use of Escrow Accounts: Divorce

-

Section 303 Stock Redemption Buy-Sell Agreement

-

-2.png) Medicare Open Enrollment Is Here: How Are Costs Changing for 2023?

Medicare Open Enrollment Is Here: How Are Costs Changing for 2023?

-

2022 High Net Worth Tax Planning

2022 High Net Worth Tax Planning

-

Policy Roadmap

Policy Roadmap

-

Section 179 Deductions

Section 179 Deductions

-

Learn About the Path to Retirement

Learn About the Path to Retirement

-

Contemplating Change: 7 Key Factors When Considering a Transition from Your Company

Contemplating Change: 7 Key Factors When Considering a Transition from Your Company

-

How Are Workers Impacted by Inflation & Rising Interest Rates?

How Are Workers Impacted by Inflation & Rising Interest Rates?

-

Lump-Sum vs Annuity and Rising Interest Rates

Lump-Sum vs Annuity and Rising Interest Rates

-

Advice for Retirees Trying to Survive a Bear Market

Advice for Retirees Trying to Survive a Bear Market

-

5 Most Important Things to do Before Leaving Your Company

5 Most Important Things to do Before Leaving Your Company

-

Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

-

8 Tenets of Choosing a Mutual Fund

-

Use of Escrow Accounts: Divorce

-

-

Medicare Open Enrollment Is Here: How Are Costs Changing for 2023?

-

2022 High Net Worth Tax Planning

-

Policy Roadmap

-

Section 179 Deductions

-

Learn About the Path to Retirement

-

Contemplating Change: 7 Key Factors When Considering a Transition from Your Company

-

How Are Workers Impacted by Inflation & Rising Interest Rates?

-

Lump-Sum vs Annuity and Rising Interest Rates

-

Advice for Retirees Trying to Survive a Bear Market

-

5 Most Important Things to do Before Leaving Your Company

-

Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)