/General/General%2013.png?width=1280&height=853&name=General%2013.png)

Healthcare Provider Update: Healthcare Provider for Bristol-Myers Squibb Bristol-Myers Squibb collaborates with multiple healthcare providers, including major national health insurers and pharmacy benefit managers (PBMs) like CVS Caremark and Express Scripts, to ensure patient access to their medications. Their widespread distribution network encompasses hospitals, clinics, and specialty pharmacies, enabling healthcare professionals to prescribe and dispense their pharmaceutical products effectively. Potential Healthcare Cost Increases in 2026 As we look toward 2026, healthcare consumers should brace for significant cost increases stemming from a combination of factors. Record hikes in premiums for Affordable Care Act (ACA) marketplace plans are anticipated, with some states facing increases over 60% due to higher medical costs and the potential expiration of federal premium subsidies. Reports indicate that nearly 92% of marketplace enrollees could see their out-of-pocket premiums soar by over 75%, putting immense financial strain on families. Coupled with escalating hospital and drug prices, particularly specialty medications like GLP-1 weight loss drugs, the burden of rising healthcare expenses is likely to affect millions as they navigate their insurance options and healthcare needs. Click here to learn more

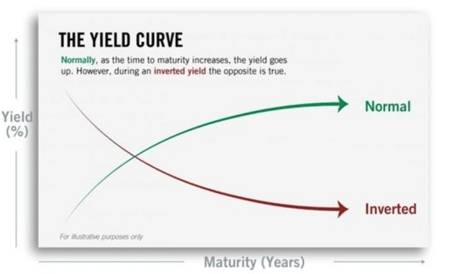

As a Bristol-Myers Squibb employee or retiree, you may have recently seen some headlines talking about an 'inverted yield curve' and what it may mean for the economy. An inverted yield curve is just one indicator of the economy's possible direction, and putting these headlines into context is valuable to those affiliated with Bristol-Myers Squibb.

First, what is the yield curve, and what does it show? The yield curve is a graphical representation of interest rates (yields) paid out by US Treasury bonds. A normal yield curve shows increasingly higher yields for longer-dated bonds, creating an upward swing. An inverted curve has a downward slope, indicating that shorter-dated bonds yield more than longer-dated bonds, which isn't typical. As a Bristol-Myers Squibb employee, being able to distinguish between these yield curves is important as it will allow better comprehension of interest rates paid out by U.S Treasury bonds.

Does an inverted yield curve mean we’re headed for a recession? Based on the historical track record of this indicator, yes, an inverted yield suggests a recession may be coming. As a Bristol-Myers Squibb employee, it might be advantageous to do some financial planning to be fully prepared for unexpected events. Since 1976, a recession has followed an inverted curve every time. However, there are some important caveats that you, as a Bristol-Myers Squibb employee, might benefit from reading here:

An inverted yield curve needs to remain inverted to be considered an indicator. It’s normal for markets to fluctuate as conditions and investor sentiment ebb and flow. But, according to the experts, for an inverted curve to be a recession indicator it needs to stay inverted for a month or more, historically. As a Bristol-Myers Squibb employee, it is imperative to keep track of indicators and their trends as to be better versed in current market situations.

As a Bristol-Myers Squibb employee it is also worthy to consider how recessions aren’t instantaneous. An inverted yield curve doesn’t mean a recession is just around the corner. Since 1976, the average time between an inverted yield curve and an official recession has been around 18 months; the longest was nearly three years. That’s plenty of time to prepare for what's to come, especially for those living in Texas!

As a Bristol-Myers Squibb employee, It’s also worthy to note how an inverted yield curve doesn’t cause a recession. The yield curve reflects bond market sentiment – it doesn’t drive it. The yield curve inverts when bond market investors feel like something may be up and, in response, favor shorter-term bonds over longer-term ones. For a Bristol-Myers Squibb employee, keeping track of bond market sentiment and the yield curve's response to changes in market is beneficial as it promotes better understanding of future market movements.

Featured Video

Articles you may find interesting:

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

It’s a deceptive signal for your portfolio. An inverted yield curve doesn’t mean it’s time to sell! Historically, the market continues to advance following an inverted yield curve, gaining an average of 11.5% real return (net of inflation) since 1976. As a Bristol-Myers Squibb employee, it is important to not let one indicator spook you!

The takeaway here is that while an inverted yield curve may be unnerving, it’s by no means cause to panic. For fortune 500 employees, it’s an opportunity to assess your specific situation. Our team of retirement-focused advisors are closely monitoring the economic conditions and will proactively alert you should we feel action needs to be taken. In the meantime, feel free to call us if you have any questions or concerns.

How does the Broward Health Cash Balance Pension Plan ensure the financial security of its employees upon retirement, and what are the specific benefit options available to employees who retire or terminate employment with Broward Health? Discuss the implications of choosing a lump sum versus a monthly benefit and how these choices affect overall retirement income.

Financial Security and Benefit Options: The Broward Health Cash Balance Pension Plan provides financial security by offering a defined benefit based on hypothetical account balances. Upon retirement or termination, employees can choose between a lump sum payment or a lifetime monthly benefit. The lump sum provides immediate access to funds, but opting for a monthly benefit ensures a steady income throughout retirement, which could lead to a more stable financial situation over time.

How does the retirement savings plan at Bristol-Myers Squibb Company compare to similar plans in the biotech and pharmaceutical industry, particularly regarding company matching contributions and employee deferral options? What factors should employees consider when deciding how much to contribute to their retirement accounts at Bristol-Myers Squibb Company?

Early Retirement Accommodations: Employees can retire early if they are at least 55 years old and have completed 5 years of vesting service. Benefits received upon early retirement are typically smaller compared to those received at the normal retirement age of 65. The normal form of benefit payment for early retirees is an actuarially adjusted life annuity based on the cash balance account at the time of early retirement(Broward Health_June 201…).

Bristol-Myers Squibb Company offers various retirement plans, including 401(k) plans and non-qualified deferred compensation plans. Can employees elaborate on the differences between these plans and how each one impacts their long-term retirement savings? Furthermore, how can an employee evaluate which plan best suits their individual retirement goals?

Vesting Schedule and Rights: The Broward Health Cash Balance Pension Plan uses a vesting schedule that grants full vesting rights after 5 years of service. Employees with fewer than 5 years of service are not eligible for benefits and forfeit their account balance. Vesting means employees gain the right to their accrued benefits, which become payable when employment ends(Broward Health_June 201…).

Based on the changes in IRS regulations for 2024, how might they affect Bristol-Myers Squibb Company's retirement and savings plans? Are there any new contribution limits or eligibility rules that employees should be aware of, and how can they adapt their savings strategies accordingly?

Role of the Pension Plan Committee: The Broward Health Pension Plan Committee administers the Cash Balance Pension Plan, ensuring compliance with laws and the plan’s financial health. The committee is responsible for investment decisions and approving plan changes, and it ensures that benefits are paid accurately and in a timely manner(Broward Health_June 201…).

What are the implications of taking an early withdrawal from retirement funds at Bristol-Myers Squibb Company, and how does it affect an employee's financial future? Employees should also consider what alternatives to early withdrawal exist within the company's policy framework.

Changes or Amendments to the Plan: The plan can be amended or terminated, but employees' vested rights are protected. Changes do not reduce accrued benefits from prior contributions, and the plan's termination follows a specific order to prioritize benefit distributions(Broward Health_June 201…).

Employees often have questions about post-retirement benefits, especially concerning medical coverage. What policies does Bristol-Myers Squibb Company have in place to ensure continued healthcare coverage for retirees, and what are the eligibility criteria for these benefits?

Recognition of Past Service upon Re-employment: If employees return to Broward Health after a break, their prior service may be recognized depending on vesting and benefit conditions at the time of rehire. Those who were vested before leaving can have their prior benefits restored, and contributions can resume after re-employment(Broward Health_June 201…).

How does Bristol-Myers Squibb Company handle the integration of pension benefits during mergers or acquisitions, and what can employees expect if they find themselves in such a situation? It would also be important for employees to understand their rights and options during these transitional phases.

Beneficiary Designations: Employees can designate beneficiaries to receive benefits if they die before or after retirement. Beneficiaries can receive lump sums or monthly payments, depending on the employee's retirement eligibility. Failure to designate a beneficiary may result in benefits going to the surviving spouse, children, or other family members as per the plan's order of priority(Broward Health_June 201…).

In light of recent company performance, what are Bristol-Myers Squibb Company’s future benefits projections, especially regarding pension plans? How can employees utilize this information to better plan for their retirement saving strategies?

Interest Credits on Accounts: The interest credits for cash balance accounts are determined based on U.S. Treasury rates, with a minimum annual interest rate. Interest is applied monthly, enhancing the account value and ensuring that employees' retirement savings grow over time(Broward Health_June 201…).

Given that Bristol-Myers Squibb Company has a robust benefits architecture, what specific programs or platforms are in place for employees to seek clarifications on their retirement benefits? How can Bristol-Myers Squibb company employees efficiently navigate these resources to address their individual inquiries?

Challenges in Filing Claims: The process for filing retirement claims involves notifying Broward Health and submitting the necessary paperwork 30 to 60 days before retirement or termination. In case of a denied claim, employees have the right to request a review and appeal, ensuring fair treatment and timely resolution(Broward Health_June 201…).

For employees looking to gain more information about retirement benefits and other related policies, how can they contact Bristol-Myers Squibb Company effectively? What communication methods are recommended to ensure that their questions are addressed promptly and comprehensively? These questions should provide employees with a deeper insight into their retirement planning while encouraging them to explore the benefits offered by Bristol-Myers Squibb Company further.

Contacting Broward Health for Information: Employees can contact the Employee Benefits department at Broward Health to learn more about the Cash Balance Pension Plan. Resources such as retirement counseling sessions and detailed plan descriptions are available to help employees understand their benefits and make informed decisions(Broward Health_June 201…).

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

.webp?width=300&height=200&name=office-builing-main-lobby%20(27).webp)

-2.png)

.webp)