/General/General%2013.png?width=1280&height=853&name=General%2013.png)

Healthcare Provider Update: Healthcare Provider for DaVita DaVita is primarily a healthcare provider specializing in kidney care and dialysis services. It operates approximately 2,800 outpatient dialysis clinics in the United States and provides acute inpatient dialysis services in around 790 hospitals. Given its significant scale, DaVita serves over 200,000 patients annually, making it one of the largest providers in the country. Potential Healthcare Cost Increases in 2026 In 2026, healthcare costs are expected to see significant increases, primarily due to escalating insurance premiums linked to the Affordable Care Act (ACA). The loss of enhanced federal premium subsidies could lead to out-of-pocket costs rising by over 75% for many consumers who rely on ACA marketplace plans. Additionally, overall medical costs are projected to surge, driven by factors such as higher hospital and physician fees and a sweeping trend of premium hikes requested by major insurers across various states, many exceeding 60%. These changes present substantial financial challenges for consumers, especially those reliant on dialysis services from providers like DaVita, necessitating proactive financial planning and healthcare strategies for the upcoming year. Click here to learn more

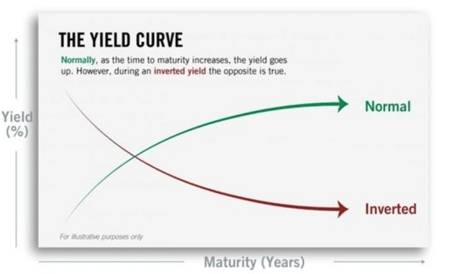

As a DaVita employee or retiree, you may have recently seen some headlines talking about an 'inverted yield curve' and what it may mean for the economy. An inverted yield curve is just one indicator of the economy's possible direction, and putting these headlines into context is valuable to those affiliated with DaVita.

First, what is the yield curve, and what does it show? The yield curve is a graphical representation of interest rates (yields) paid out by US Treasury bonds. A normal yield curve shows increasingly higher yields for longer-dated bonds, creating an upward swing. An inverted curve has a downward slope, indicating that shorter-dated bonds yield more than longer-dated bonds, which isn't typical. As a DaVita employee, being able to distinguish between these yield curves is important as it will allow better comprehension of interest rates paid out by U.S Treasury bonds.

Does an inverted yield curve mean we’re headed for a recession? Based on the historical track record of this indicator, yes, an inverted yield suggests a recession may be coming. As a DaVita employee, it might be advantageous to do some financial planning to be fully prepared for unexpected events. Since 1976, a recession has followed an inverted curve every time. However, there are some important caveats that you, as a DaVita employee, might benefit from reading here:

An inverted yield curve needs to remain inverted to be considered an indicator. It’s normal for markets to fluctuate as conditions and investor sentiment ebb and flow. But, according to the experts, for an inverted curve to be a recession indicator it needs to stay inverted for a month or more, historically. As a DaVita employee, it is imperative to keep track of indicators and their trends as to be better versed in current market situations.

As a DaVita employee it is also worthy to consider how recessions aren’t instantaneous. An inverted yield curve doesn’t mean a recession is just around the corner. Since 1976, the average time between an inverted yield curve and an official recession has been around 18 months; the longest was nearly three years. That’s plenty of time to prepare for what's to come, especially for those living in Texas!

As a DaVita employee, It’s also worthy to note how an inverted yield curve doesn’t cause a recession. The yield curve reflects bond market sentiment – it doesn’t drive it. The yield curve inverts when bond market investors feel like something may be up and, in response, favor shorter-term bonds over longer-term ones. For a DaVita employee, keeping track of bond market sentiment and the yield curve's response to changes in market is beneficial as it promotes better understanding of future market movements.

Featured Video

Articles you may find interesting:

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

It’s a deceptive signal for your portfolio. An inverted yield curve doesn’t mean it’s time to sell! Historically, the market continues to advance following an inverted yield curve, gaining an average of 11.5% real return (net of inflation) since 1976. As a DaVita employee, it is important to not let one indicator spook you!

The takeaway here is that while an inverted yield curve may be unnerving, it’s by no means cause to panic. For fortune 500 employees, it’s an opportunity to assess your specific situation. Our team of retirement-focused advisors are closely monitoring the economic conditions and will proactively alert you should we feel action needs to be taken. In the meantime, feel free to call us if you have any questions or concerns.

What steps should DaVita employees take to prepare for retirement within the context of the DaVita Retirement Savings Plan? How does the structure of this plan align with common retirement strategies, and what resources does DaVita provide to help employees understand their options when they are considering retirement?

DaVita employees preparing for retirement within the context of the DaVita Retirement Savings Plan should review their savings, evaluate their retirement goals, and ensure they are maximizing contributions. The plan aligns with common retirement strategies by offering diversified investment options and matching contributions, making it easier for employees to grow their retirement funds. DaVita provides resources, such as the Voya website and a dedicated retirement service center, to help employees understand their retirement options and plan effectively.

How does the DaVita Retirement Savings Plan accommodate employees who have previously held jobs with different retirement plans? What documentation is necessary for these employees to successfully roll over their funds to the DaVita Retirement Savings Plan, and how does DaVita ensure compliance with IRS regulations in these situations?

The DaVita Retirement Savings Plan accommodates employees who have held jobs with other retirement plans by allowing rollovers from qualified plans, including 401(k)s, 403(b)s, and IRAs. Employees need to obtain proof of plan qualification and taxability from their previous employer or financial institution. DaVita ensures compliance with IRS regulations by requiring proper documentation, including an IRS Letter of Determination or rollover distribution statement, as noted in the Rollover Contribution Form(DaVita_08_11_2016_Rollo…).

In what ways can DaVita employees maximize their contributions to the DaVita Retirement Savings Plan, particularly considering the IRS contribution limits for 2024? What strategies should employees consider when determining how much to contribute, and how can DaVita support employees in achieving their retirement savings goals?

DaVita employees can maximize their contributions to the Retirement Savings Plan by taking advantage of the IRS contribution limits for 2024. The limit for employee deferrals is expected to be around $23,000, with an additional catch-up contribution of $7,500 for those aged 50 and above. Strategies include contributing enough to receive the full employer match and adjusting contributions to meet future goals. DaVita provides support through educational resources and financial tools available on the Voya platform.

How does DaVita address the investment options available through its Retirement Savings Plan? Specifically, what guidance is provided to employees regarding the selection of investment funds, and how can employees access information about their investment choices within the DaVita Retirement Savings Plan?

DaVita offers a range of investment options in its Retirement Savings Plan, including target date funds, stock funds, and bond funds. The company provides guidance to employees through the Voya website and customer service center, where they can access detailed information about available investment funds. Employees can tailor their portfolios based on their retirement timeline and risk tolerance, and they are encouraged to review their investment choices regularly.

What are the tax implications of withdrawing funds from the DaVita Retirement Savings Plan, and how can employees prepare for this? How does DaVita provide clarity around the tax obligations faced by employees when they begin to access their retirement savings, particularly for those who are unfamiliar with tax rules relating to retirement distributions?

Withdrawing funds from the DaVita Retirement Savings Plan can have significant tax implications. Withdrawals before age 59½ may incur early withdrawal penalties, and all withdrawals are subject to income tax unless they are from a Roth account. DaVita educates employees on these tax rules through its Voya platform, providing clarity on how to manage taxes when accessing retirement savings. Employees are encouraged to consult tax professionals for specific guidance.

How does DaVita educate its employees about the importance of understanding their retirement plan features? What programs or resources are available for employees to learn about financial wellness and retirement readiness, and how frequently does DaVita conduct educational initiatives related to its Retirement Savings Plan?

DaVita educates its employees on retirement plan features through webinars, financial wellness programs, and resources available on the Voya website. These initiatives focus on retirement readiness, savings strategies, and understanding the investment options within the plan. DaVita regularly updates employees through newsletters, and webinars are conducted periodically to keep employees informed about the plan.

In the event of unexpected financial hardships, what options do DaVita employees have regarding loans or early withdrawals from the DaVita Retirement Savings Plan? What do employees need to know about the process and potential penalties associated with accessing their funds early?

In the case of financial hardships, DaVita employees can take loans or early withdrawals from their Retirement Savings Plan. However, early withdrawals may be subject to penalties and taxes, depending on the circumstances. DaVita's Voya service center provides guidance on the process, explaining the potential costs and consequences. Employees are encouraged to explore alternative solutions before opting for early withdrawals to avoid unnecessary penalties.

What role do employees' personal financial goals play when determining their participation in the DaVita Retirement Savings Plan? How can DaVita assist employees in aligning their savings plan with their individual financial objectives, and what external financial consulting resources might they recommend?

Employees' personal financial goals play a key role in determining their participation in the DaVita Retirement Savings Plan. DaVita helps employees align their retirement savings with their broader financial objectives by offering planning tools and resources on the Voya platform. Additionally, external financial advisors or consulting services may be recommended for those needing personalized financial advice.

How can DaVita employees contact the company for more information regarding the Retirement Savings Plan? What specific channels, such as phone numbers or online resources, are available, and what types of inquiries can employees expect to address when contacting DaVita about their retirement savings?

DaVita employees seeking more information about the Retirement Savings Plan can contact the plan’s service center through the Voya website or by calling the dedicated support line. Customer service representatives are available to assist with inquiries related to contributions, investment options, rollovers, and withdrawals. Online resources and account management tools are also accessible for employees who prefer digital support.

How does DaVita ensure that it stays current with regulatory changes that impact employee retirement savings, particularly with respect to IRS limits set for 2024? What processes does DaVita have in place to update employees about these changes, and how does the company maintain transparency regarding its compliance with retirement regulations?

DaVita ensures it stays up to date with regulatory changes, including IRS contribution limits and distribution rules, through regular collaboration with financial service providers and legal experts. The company updates employees via email, webinars, and its Voya platform when changes occur, maintaining transparency about compliance with retirement regulations and keeping employees informed of any adjustments to the plan.

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

.webp?width=300&height=200&name=office-builing-main-lobby%20(27).webp)

-2.png)

.webp)