/General/General%208.png?width=1280&height=853&name=General%208.png)

Healthcare Provider Update: Healthcare Provider for State Street: State Street Corporation collaborates with various healthcare providers to offer employee benefits, typically leveraging its extensive network through insurers. The primary healthcare provider for State Street employees is UnitedHealth Group, which offers services to ensure comprehensive health coverage and support. Potential Healthcare Cost Increases in 2026: As the healthcare landscape evolves, significant cost increases are anticipated in 2026, particularly for those enrolled in Affordable Care Act (ACA) marketplace plans. With the potential expiration of enhanced premium tax credits, many enrollees could face premium hikes exceeding 75%, leading to out-of-pocket costs becoming dangerously unaffordable for millions. Insurers attribute these steep increases to rising medical costs, aggressive premium requests-including New York's staggering 66% increase from UnitedHealthcare-and ongoing pressures from inflation across the healthcare sector. Overall, the combination of these factors underscores a perfect storm of market conditions that could strain consumer budgets significantly come 2026. Click here to learn more

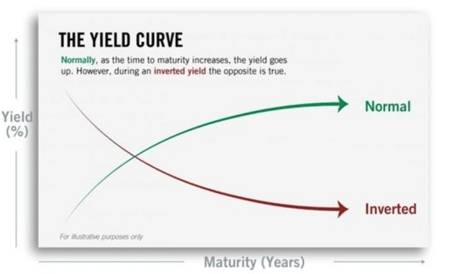

As a State Street employee or retiree, you may have recently seen some headlines talking about an 'inverted yield curve' and what it may mean for the economy. An inverted yield curve is just one indicator of the economy's possible direction, and putting these headlines into context is valuable to those affiliated with State Street.

First, what is the yield curve, and what does it show? The yield curve is a graphical representation of interest rates (yields) paid out by US Treasury bonds. A normal yield curve shows increasingly higher yields for longer-dated bonds, creating an upward swing. An inverted curve has a downward slope, indicating that shorter-dated bonds yield more than longer-dated bonds, which isn't typical. As a State Street employee, being able to distinguish between these yield curves is important as it will allow better comprehension of interest rates paid out by U.S Treasury bonds.

Does an inverted yield curve mean we’re headed for a recession? Based on the historical track record of this indicator, yes, an inverted yield suggests a recession may be coming. As a State Street employee, it might be advantageous to do some financial planning to be fully prepared for unexpected events. Since 1976, a recession has followed an inverted curve every time. However, there are some important caveats that you, as a State Street employee, might benefit from reading here:

An inverted yield curve needs to remain inverted to be considered an indicator. It’s normal for markets to fluctuate as conditions and investor sentiment ebb and flow. But, according to the experts, for an inverted curve to be a recession indicator it needs to stay inverted for a month or more, historically. As a State Street employee, it is imperative to keep track of indicators and their trends as to be better versed in current market situations.

As a State Street employee it is also worthy to consider how recessions aren’t instantaneous. An inverted yield curve doesn’t mean a recession is just around the corner. Since 1976, the average time between an inverted yield curve and an official recession has been around 18 months; the longest was nearly three years. That’s plenty of time to prepare for what's to come, especially for those living in Texas!

As a State Street employee, It’s also worthy to note how an inverted yield curve doesn’t cause a recession. The yield curve reflects bond market sentiment – it doesn’t drive it. The yield curve inverts when bond market investors feel like something may be up and, in response, favor shorter-term bonds over longer-term ones. For a State Street employee, keeping track of bond market sentiment and the yield curve's response to changes in market is beneficial as it promotes better understanding of future market movements.

Featured Video

Articles you may find interesting:

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

It’s a deceptive signal for your portfolio. An inverted yield curve doesn’t mean it’s time to sell! Historically, the market continues to advance following an inverted yield curve, gaining an average of 11.5% real return (net of inflation) since 1976. As a State Street employee, it is important to not let one indicator spook you!

The takeaway here is that while an inverted yield curve may be unnerving, it’s by no means cause to panic. For fortune 500 employees, it’s an opportunity to assess your specific situation. Our team of retirement-focused advisors are closely monitoring the economic conditions and will proactively alert you should we feel action needs to be taken. In the meantime, feel free to call us if you have any questions or concerns.

What is the 401(k) plan offered by State Street?

The 401(k) plan at State Street is a retirement savings plan that allows employees to save a portion of their salary before taxes are deducted.

How can I enroll in State Street's 401(k) plan?

Employees can enroll in State Street's 401(k) plan by accessing the enrollment portal through the company’s HR website or by contacting the HR department for assistance.

What is the company match for State Street's 401(k) plan?

State Street offers a company match for contributions made to the 401(k) plan, typically matching a percentage of employee contributions up to a certain limit.

Are there any eligibility requirements for State Street's 401(k) plan?

Yes, employees must meet specific eligibility criteria, such as length of service and employment status, to participate in State Street's 401(k) plan.

What investment options are available in State Street's 401(k) plan?

State Street's 401(k) plan offers a range of investment options, including mutual funds, target-date funds, and other investment vehicles tailored to different risk tolerances.

Can I change my contribution rate to State Street's 401(k) plan?

Yes, employees can change their contribution rates to State Street's 401(k) plan at any time, subject to the plan's guidelines.

How often can I change my investment choices in State Street's 401(k) plan?

Employees can typically change their investment choices in State Street's 401(k) plan on a regular basis, often quarterly or as specified in the plan documents.

What happens to my 401(k) plan if I leave State Street?

If you leave State Street, you can choose to roll over your 401(k) balance to another retirement account, leave it in the State Street plan, or cash it out, subject to tax implications.

Does State Street offer financial education regarding the 401(k) plan?

Yes, State Street provides resources and educational sessions to help employees understand their 401(k) plan options and make informed investment decisions.

What is the vesting schedule for State Street's 401(k) plan?

The vesting schedule for State Street's 401(k) plan determines how long you must work at the company to fully own the employer contributions, which may vary based on tenure.

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

.webp?width=300&height=200&name=office-builing-main-lobby%20(27).webp)

-2.png)

.webp)