/General/General%202.png?width=1280&height=853&name=General%202.png)

Healthcare Provider Update: Healthcare Provider for Union Pacific Union Pacific provides healthcare coverage primarily through its management benefits program, which may include options such as insurance plans, Medicare, and Medicaid for retirees. The specific providers associated with Union Pacific's healthcare offerings can vary and are typically outlined in their employee and retiree benefit guides. Potential Healthcare Cost Increases in 2026 As 2026 approaches, healthcare costs are expected to rise significantly, particularly for those enrolled in the Affordable Care Act (ACA) marketplace. Record premium hikes are anticipated, with over 22 million enrollees facing potential increases exceeding 75%-a consequence of expiring federal subsidies and aggressive rate hikes by major insurers. With employers also planning to shift more healthcare costs to employees through higher deductibles and out-of-pocket maximums, individuals may find themselves grappling with substantial financial burdens in their healthcare expenses next year. Click here to learn more

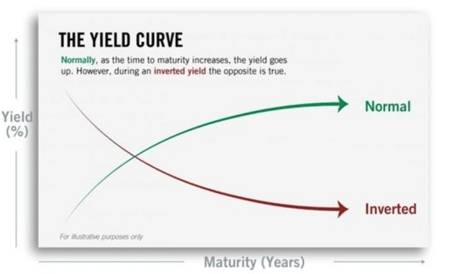

As a Union Pacific employee or retiree, you may have recently seen some headlines talking about an 'inverted yield curve' and what it may mean for the economy. An inverted yield curve is just one indicator of the economy's possible direction, and putting these headlines into context is valuable to those affiliated with Union Pacific.

First, what is the yield curve, and what does it show? The yield curve is a graphical representation of interest rates (yields) paid out by US Treasury bonds. A normal yield curve shows increasingly higher yields for longer-dated bonds, creating an upward swing. An inverted curve has a downward slope, indicating that shorter-dated bonds yield more than longer-dated bonds, which isn't typical. As a Union Pacific employee, being able to distinguish between these yield curves is important as it will allow better comprehension of interest rates paid out by U.S Treasury bonds.

Does an inverted yield curve mean we’re headed for a recession? Based on the historical track record of this indicator, yes, an inverted yield suggests a recession may be coming. As a Union Pacific employee, it might be advantageous to do some financial planning to be fully prepared for unexpected events. Since 1976, a recession has followed an inverted curve every time. However, there are some important caveats that you, as a Union Pacific employee, might benefit from reading here:

An inverted yield curve needs to remain inverted to be considered an indicator. It’s normal for markets to fluctuate as conditions and investor sentiment ebb and flow. But, according to the experts, for an inverted curve to be a recession indicator it needs to stay inverted for a month or more, historically. As a Union Pacific employee, it is imperative to keep track of indicators and their trends as to be better versed in current market situations.

As a Union Pacific employee it is also worthy to consider how recessions aren’t instantaneous. An inverted yield curve doesn’t mean a recession is just around the corner. Since 1976, the average time between an inverted yield curve and an official recession has been around 18 months; the longest was nearly three years. That’s plenty of time to prepare for what's to come, especially for those living in Texas!

As a Union Pacific employee, It’s also worthy to note how an inverted yield curve doesn’t cause a recession. The yield curve reflects bond market sentiment – it doesn’t drive it. The yield curve inverts when bond market investors feel like something may be up and, in response, favor shorter-term bonds over longer-term ones. For a Union Pacific employee, keeping track of bond market sentiment and the yield curve's response to changes in market is beneficial as it promotes better understanding of future market movements.

Featured Video

Articles you may find interesting:

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

It’s a deceptive signal for your portfolio. An inverted yield curve doesn’t mean it’s time to sell! Historically, the market continues to advance following an inverted yield curve, gaining an average of 11.5% real return (net of inflation) since 1976. As a Union Pacific employee, it is important to not let one indicator spook you!

The takeaway here is that while an inverted yield curve may be unnerving, it’s by no means cause to panic. For fortune 500 employees, it’s an opportunity to assess your specific situation. Our team of retirement-focused advisors are closely monitoring the economic conditions and will proactively alert you should we feel action needs to be taken. In the meantime, feel free to call us if you have any questions or concerns.

What are the specific eligibility requirements for employees of Union Pacific Corporation to participate in the pension plan, and how might these requirements evolve as IRS regulations change? Understanding how Union Pacific Corporation aligns its eligibility criteria with broader IRS regulations can help employees assess their own eligibility for the pension plan, particularly in light of any new IRS guidelines issued for 2024.

Eligibility Requirements for Pension Plan Participation: Eligibility to participate in the Union Pacific Corporation pension plan is governed by specific criteria set forth in the plan documents. As of January 1, 2018, the plan was closed to new participants, meaning individuals hired on or after this date are not eligible. For existing employees, eligibility to accrue benefits continued provided they were active participants as of December 31, 2017, and remained in covered employment. Changes in IRS regulations could potentially alter these eligibility criteria by requiring adjustments to maintain compliance with legal standards, potentially affecting who can accrue benefits in the future.

How does Union Pacific Corporation calculate an employee's final average compensation for pension benefits? Given the potential for changes in compensation structures, it is essential for employees at Union Pacific Corporation to comprehend how their average compensation is determined and how this figure might impact their retirement planning.

Calculation of Final Average Compensation: The pension plan calculates an employee's final average compensation based on the average monthly compensation over the 36-consecutive month period out of the last 120 months of active participation that yields the highest average. This includes base pay, overtime, and certain incentive and bonus payments. Understanding this calculation is crucial for employees to appreciate how raises, bonuses, and other compensation changes might impact their pension benefits.

What forms of payment options are available to employees of Union Pacific Corporation when they choose to retire, and how do these options influence the total benefit received? Employees need detailed information on the different payment structures to make informed decisions that suit their financial needs in retirement.

Payment Options Available at Retirement: Union Pacific offers various payment options for pension benefits upon retirement. Employees can choose a lifetime annuity or opt for joint and survivor annuities, providing continued benefits to a designated beneficiary. Other options include certain annuities that guarantee payments for a set period, regardless of the employee's lifespan. These choices allow employees to tailor retirement benefits to their financial needs and family circumstances.

In what ways does Union Pacific Corporation integrate Social Security and Railroad Retirement benefits into the pension plan, and how does this integration affect the overall retirement income for employees? Employees should explore the implications of these benefits on their pensions to develop a comprehensive retirement income strategy.

Integration of Social Security and Railroad Retirement Benefits: The pension benefits are coordinated with Social Security or Railroad Retirement benefits through an offset formula in the pension plan. This integration reduces the pension benefit by a portion of the government retirement benefits projected at the time of retirement, reflecting that some of the funding for these benefits comes from Union Pacific. Employees need to understand how this interaction affects their total retirement income to plan effectively.

What strategies can employees of Union Pacific Corporation employ to maximize their pension benefits prior to retirement while adhering to IRS limits? Employees must be informed of practical steps they can take to enhance their benefits within the framework established by IRS guidelines.

Maximizing Pension Benefits: To maximize pension benefits under the IRS limits, Union Pacific employees can ensure they maximize their earnings during the final average compensation period, continue employment as long as possible to increase credited service, and make strategic decisions about retirement age and benefit commencement. Understanding the interplay of these factors with IRS contribution and benefit limits is essential for optimizing pension payouts.

How does the vesting schedule work within Union Pacific Corporation's pension plan, and what implications does this have for employees who leave the company before full vesting? An understanding of the vesting schedule is crucial for employees at Union Pacific Corporation to grasp the long-term benefits they might forfeit by leaving before they are fully vested.

Vesting Schedule: The vesting schedule is crucial as it determines an employee's entitlement to pension benefits upon leaving the company before retirement age. Union Pacific's plan requires employees to complete five years of vesting service to qualify for a vested benefit, which is payable as early as age 55. Employees considering leaving Union Pacific should be aware of how their vesting status might affect their pension entitlements.

What responsibilities do employees have to keep Union Pacific Corporation informed about their earnings records, particularly when claims for benefits arise, and what might happen if these records are not accurately reported? Employees should be aware of their duties to maintain their benefits and the potential consequences of noncompliance within the pension plan.

Responsibilities for Reporting Earnings: Employees are responsible for ensuring that Union Pacific has accurate records of their earnings to calculate pension benefits accurately. Failure to report or correct discrepancies in earnings records can lead to miscalculations in pension benefits, affecting retirement income. It's vital for employees to regularly review their earnings records and report any inaccuracies.

How does Union Pacific Corporation ensure compliance with ERISA regulations as they relate to employee retirement benefits, and what rights do employees have under these regulations? Employees of Union Pacific Corporation should familiarize themselves with their rights under ERISA to ensure they are adequately protected when claiming pension benefits.

Compliance with ERISA Regulations: Union Pacific ensures compliance with the Employee Retirement Income Security Act (ERISA) regulations, which protect employees' rights to their pension benefits. Employees have specific rights under these regulations, including the right to receive information about their pension plan, appeal denials of benefits, and sue for benefits or breaches of fiduciary duty. Awareness of these rights is important for employees to safeguard their benefits.

What happens to the pension benefits of employees of Union Pacific Corporation in the event of a company merger or acquisition, and how can employees prepare for these changes? Understanding the potential impacts of organizational changes on their pension benefits can enable employees to safeguard their retirement plans.

Impact of Company Mergers or Acquisitions: In the event of a merger or acquisition, employees' pension benefits could be affected. Union Pacific's pension plan provisions include terms for handling benefits under such circumstances. Employees should be proactive in understanding how these corporate changes might impact their pension benefits and seek clarity on their rights and options.

How can employees of Union Pacific Corporation contact the Benefits Group to inquire further about the pension plan and related questions? Clear guidance on contacting the Benefits Group will assist employees in accessing the information necessary to navigate their retirement options effectively.

Contacting the Benefits Group: Employees with questions or who need assistance regarding their pension plan can contact Union Pacific's Benefits Group. Having the contact information handy ensures that employees can promptly address concerns or seek guidance about their retirement benefits, aiding in effective retirement planning.

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

.webp?width=300&height=200&name=office-builing-main-lobby%20(27).webp)

-2.png)

.webp)