/General/General%207.png?width=1280&height=853&name=General%207.png)

Duke Energy employees may have realized how falling sick in this country can become considerably expensive. Pharmaceutical companies raised list prices of 983 arthritis, cancer and other prescription drugs by an average of 5.6% at the start of this year. Furthermore, CalPERS announced an average rate increase of 7% for basic products. While healthcare itself may seem costly, it can be even more expensive to be healthy over the long term. The reasoning behind said statement is the increase in medical prices at a higher pace than inflation. Furthermore, retirees increase their consumption of healthcare as they age, which turns out to become more and more expensive with time. CEO of HealthView Services Ron Mastrogiovanni claims that “Longevity is the big driver of healthcare costs, not conditions.” If you take a healthy 65-year-old woman set to live until 89 as an example, she will incur an estimated $175,000 more in lifetime healthcare costs than a same age woman with type 2 diabetes who lives until 81.

Duke Energy employees should consider how over the past few years we have only experienced moderate increases in medical prices. Despite that, healthcare inflation is expected to revert to trend increases or higher, due to cost pressures from the pandemic. National Health spending is projected to grow 5.1% year over year starting 2021 and ending 2030 according to projections by the Centers for Medicare and Medicaid Services. With this taken into account, Duke Energy employees must plan carefully in order to effectively manage future medical needs, including the uncertain values of long-term care.

Get Ready for Healthcare Inflation

Employers expect to pay 6.5% more for employee healthcare coverage, according to an Aon report. When it comes to healthcare inflation, Duke Energy employees should note how health inflation tends to lag behind other price increases in the economy. The reasoning behind this is due to pricing being set in multiyear contracts between insurers and providers. As contracts expire and require renewal, providers will ask for a higher price to make up for their increased labor costs, supply chain issues, and other challenges brought on by the pandemic. With medicare being a government program, there is some bargaining power to limit remuneration for doctors and hospitals. Duke Energy employees should be aware of how despite passing some of its increased costs to beneficiaries, the people with commercial medical insurance are the ones affected from rising prices charged by providers.

Featured Video

Articles you may find interesting:

- 8 Tenets of Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Section 303 Stock Redemption Buy-Sell Agreement

- Medicare Open Enrollment Is Here: How Are Costs Changing for 2023?

- 2022 High Net Worth Tax Planning

- Policy Roadmap

- Section 179 Deductions

- Learn About the Path to Retirement

- Contemplating Change: 7 Key Factors When Considering a Transition from Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Advice for Retirees Trying to Survive a Bear Market

- 5 Most Important Things to do Before Leaving Your Company

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- 8 Tenets of Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Section 303 Stock Redemption Buy-Sell Agreement

- Medicare Open Enrollment Is Here: How Are Costs Changing for 2023?

- 2022 High Net Worth Tax Planning

- Policy Roadmap

- Section 179 Deductions

- Learn About the Path to Retirement

- Contemplating Change: 7 Key Factors When Considering a Transition from Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Advice for Retirees Trying to Survive a Bear Market

- 5 Most Important Things to do Before Leaving Your Company

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

COBRA, or continuing coverage from a previous employer usually costs 102% of the total premium. Duke Energy employees should note however, that workers generally pay between 20% - 30% of total premiums. According to the Kaiser Family Foundation, an average unsubsidized, high-deductible silver plan premium for a 60 year-old-couple can cost upwards of 1,900 a month in 2023. Due to increases in healthcare costs, early retirees may consider claiming Social Security benefits at the age of 62 in order to have more money available prior to becoming medicare eligible at 65. What Duke Energy employees should consider however, is that opting for those reduced benefits to have money available early on might wind up leaving you shortchanged in late retirement. The reason behind this is due to the permanently reduced payments not being able to keep up with the constantly increasing medical costs. For individuals born in 1960 or after, claiming Social Security benefits at the age of 62 receive an estimated 30% less than what would be attributed if taken at age 67.

Medicare Isn’t a Solution

Duke Energy employees should note how Medicare Part A costs are increasing by an overall average of 3% for 2023, which is lower than last year's increase. a majority of individuals believe healthcare costs will significantly decrease upon enrolling in medicare. The truth is, although medicare provides decent coverage, people believe it to be cheaper than it actually is.

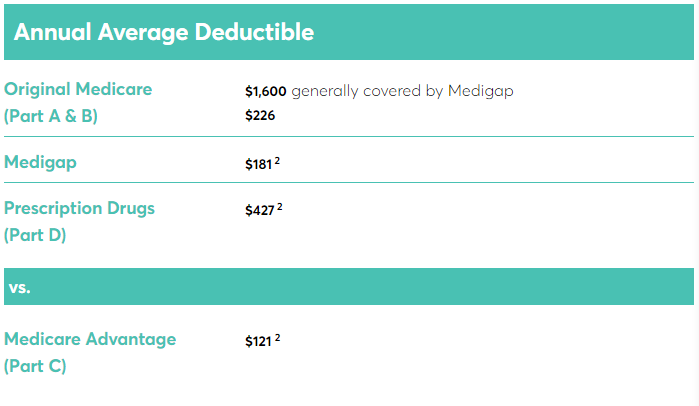

Duke Energy retirees who are new to medicare must recognize the multiple “parts” to it. As of 2023, medicare part B premium costs 164.90, and to consult a doctor or visit a hospital, there are copayments, deductibles, and coinsurance. Essentially this means that although medicare makes it cheaper for individuals to afford healthcare, it doesn't make it free. With that taken into account, Duke Energy retirees may benefit from Medigap coverage. Medicare supplement (Medigap) insurance helps protect more than 14.5 million people eligible for Medicare from high out-of-pocket costs not covered by Medicare. Medicare Supplement also provides seniors the flexibility to budget for those costs and avoid multiple complex bills from their doctors and hospitals. Medigap offers coverage, at varying levels, for the significant out-of-pocket costs that are not covered by Medicare, such as deductibles, coinsurance, and copayments. Medigap coverage allows seniors and younger Medicare enrollees with disabilities – many of whom are on fixed incomes – to budget for medical costs and avoid the confusion and inconvenience of handling complex medical bills. Medicare enrollees with Medicare Supplement coverage were three times less likely to have problems paying medical bills compared to enrollees without Medicare Supplement policies.

For Duke Energy employees wondering whether they need medigap, it is important to note how medicare only covers roughly 80% of total costs, rendering you accountable for the remaining 20%. Additionally, with out-of-pocket spending having no limit with only medicare, a serious accident or illness could result in a tremendous financial responsibility. A supplement plan will address your remaining liability and limit out-of-pocket costs in a catastrophic situation, leading to much more predictability for your budget.

Medicare cost breakdown for Duke Energy employees will depend on the elected coverage: Medicare Advantage plans provide the benefits of Parts A, B, and often D, usually for about the same amount, with lower copays, so there’s no need for Medigap. Some also offer benefits not in Original Medicare, such as fitness classes or some vision and dental care. Advantage plans, run by private insurers, can involve high out-of-pocket costs if you get sick or seek care outside the plan’s network. plans can carry hidden risks, especially for people with major health issues. “Some people in Medicare Advantage end up paying unexpectedly high costs when they become ill or find their network lacks the providers they need,” says Tricia Neuman, senior vice president at Kaiser.

With traditional Medicare, Duke Energy employees will have the option of buying a stand-alone Part D drug plan and a Medigap supplement. This is where longevity risk is of great concern: Many Medigap policies raise their premium prices annually based on a beneficiary’s “attained age.” Premiums start low and increase periodically. A 65-year-old woman who pays $1,517 in annual premiums for her Plan G Medigap plan will pay $9,512 for the same coverage at age 89 in the year 2047, according to HealthView Services’ projections.

As the annual cost-of-living adjustment to Social Security falls short of compounding medical inflation, healthcare costs consume an increasing portion of retirees’ benefit checks. For a 65-year-old couple with $250,000 in modified adjusted gross income in 2023, who pay the Medicare high-income surcharges, healthcare costs will devour 29% of their Social Security checks today and 57% at age 85, according to HealthView Services. Not surprisingly, these numbers look worse as incomes fall.

HealthView Services’ projections exclude potential long-term care costs, so the actual numbers will be higher for those who move into a nursing home or assisted-living facility, or receive care at home.

Shocked at these costs? That may be because previous generations were much more likely to have retiree medical benefits from their employer, which functioned like a Medigap plan and often included drug coverage. Some employers shouldered the full cost, and others covered part, but either way, they greatly reduced retirees’ out-of-pocket expenses in old age. Plus, previous generations had shorter life spans on average, so they incurred fewer long-term care costs.

For people who actually run out of money in old age, Medicaid will step in to cover long-term care costs at facilities that accept it (and many of the best don’t). You would need to completely deplete your assets and have almost no income to qualify. Plus, the government conducts what’s known as a “five-year look back” to make sure assets weren’t handed off to heirs. This program is a true safety net, not a planning opportunity.

Yes, There Are Real Solutions

Under the current structure of Social Security, about 85% of the funds that are paid into the program are distributed to retirees or qualifying individuals. That ensures those who may need an income during their retirement years are able to have one. Although Social Security is not a complete income replacement for most retirees, it does provide supplemental income that can help individuals, couples, and families maintain their lifestyle. Social Security is essentially a form of longevity insurance, with the fattest payouts going to those who wait the longest to claim. If people born in 1960 or later can delay until 70, they’ll receive 124% of what they’d receive at their full retirement age of 67, which is 100% of their earned benefit (people born before then receive an even higher percentage).

Beyond that, annuities can be a good option. According to a study by The Phoenix Companies, nearly three-quarters (71 percent) of Americans would consider using annuities to establish predictable income in retirement, as a vehicle to protect inheritances, or as a way to protect money for health and chronic care expenses. Despite that, 53 percent said they are “not familiar with annuities,” according to Phoenix Companies, and only 20 percent are actually planning to use an annuity to convert retirement savings into a set income stream. Carolyn McClanahan, founder of Life Planning Partners in Jacksonville, Fla., and a Certified Financial Planner/medical doctor often recommends fixed-income annuities for clients in danger of outliving their assets. That determination centers more on spending needs than overall wealth. Retirees with $3 million in assets plus Social Security who have $80,000 in annual expenses won’t have to worry about outliving their money, but a couple with $200,000 in annual spending needs could, McClanahan says.

Fixed-income annuities are the simplest type: an insurance policy where consumers pay a lump sum to a carrier in return for guaranteed income for life or a fixed time frame. The longer you wait, the higher the payout. For a single life policy in Florida with a cash refund (so beneficiaries get cash back in the event of an early death) and a $100,000 premium, a 65-year-old man would get $585 in monthly income as of late 2022, versus $648 if purchased at age 70 and $842 if purchased at age 80, according to Cannex Financial Exchanges, a provider of annuity data. A woman would receive slightly less because of her longer projected life span.

Many advisors use an annuity like this to supplement other sources of retirement income, including drawing down a portfolio of stocks and bonds held in a retirement account. Many different types of annuities are available. When investors have annuities explained to them, particularly the variety of annuities designed to protect income for specific purposes in retirement, such as long-term health care costs, people show a strong interest, said Mark Fitzgerald. “The annuities available today are not your grandfather’s annuity.” About half of respondents to the Phoenix study said they would use annuities to establish an income stream. Forty-one percent said they would use an annuity as an inheritance vehicle, and 36 percent said they’d use an annuity to establish reserves for health-care expenses. One-quarter of respondents said they would not consider purchasing an annuity for any reason.

Ideally, McClanahan advises clients in excellent health to hold off purchasing an annuity until their 80s. If cash is an issue, she urges them to work as long as they can, even if it’s just at a part-time job. Clients in average health might purchase an annuity in their 70s. Depending on their income needs, McClanahan might buy more than one annuity and then ladder them, staggering purchases over a number of years for a higher payout with each subsequent year.

Considering Long-Term Care Insurance

There are about 65,600 regulated long-term care facilities in the United States, according to a 2019 study from the National Center for Health Statistics. Together, these institutions serve over 8.3 million residents, including: 286,300 people in day-based caregiving, 1,347,600 people in nursing homes, and 811,500 people in assisted living facilities. Over the next 10 years, the number of residents in each of these facilities is expected to grow sharply. If trends hold up, the number of nursing home residents could double by 2030. This has the potential to not only put a strain on the existing network of long-term care facilities but also contribute to the ballooning cost of healthcare for individuals over 65. The issue with this is that Medicare doesn’t cover long-term care, regardless of where it’s provided. The program will cover a rehabilitative stay in a care facility following, say, a hip replacement, but it doesn’t cover the kind of help that many older adults eventually need: assistance with activities of daily living such as bathing, dressing, and eating. Someone turning 65 today has about a 70% chance of eventually needing some long-term care, with an average duration of 2.2 years for men and 3.7 years for women.

Josh Strange, a Certified Financial Planner with Good Life Financial Advisors of NOVA in Alexandria, VA., says clients will often try to skirt the topic when he raises it with them. “They say, ‘Someone will take me behind the woodshed and shoot me,’ which I have never seen happen,” Strange says.

Because of its high cost, common wisdom holds that long-term care insurance is most appropriate for the mass affluent, those with $500,000 to about $2 million in investable assets. Anything lower than that, and you might exhaust your savings even before the need for long-term care arises. Anything higher than about $2 million, the thinking goes, and you can afford to self-insure against potential long-term care costs.

Yet Strange challenges that thinking, recommending that even higher-net-worth clients consider coverage. He likes hybrid life and long-term care products that offer long-term care coverage with a death benefit. They’re an easier sell for many consumers than traditional long-term care insurance, where premiums are forfeited if there is no claim, just like with home or auto insurance.

This coverage will typically defray just a portion of the costs if care is needed. (Note: The insurance company defines the eligibility criteria, not the family; usually the policyholder must demonstrate the need for assistance with at least two of the six activities of daily living.) If care isn’t required, it becomes a way to transfer wealth tax-free to heirs.

Prior iterations of hybrid life and long-term care policies optimized the death benefit and offered a small long-term care rider, but some policies today prioritize the long-term care benefit. One example is Lincoln Financial Group’s MoneyGuard Fixed Advantage, which has an average claim age of 83, according to the company. At that age, a married woman who bought a $100,000 policy at age 55 would have a long-term care pool of $916,607, a death benefit of $123,872, and a surrender value (the amount you get if you cancel your policy at any time) of $70,000, according to an illustration provided to Barron’s .

These policies are medically underwritten, which means the carrier will review your health status to determine your eligibility for coverage. That’s one reason to consider these policies in your early 50s, when you’re more likely to be in good health.

Whether you end up buying coverage or not, it’s important to consider your options when it comes to long-term care. With there being approximately 267 million life insurance policies in the United States, Duke Energy employees may benefit from seeking professional financial advice when uncertain about what decision to make. By contacting The Retirement Group, you may partake in a complimentary cash flow analysis that will help you better understand which option best suits your needs.

Reference(s):

- https://www.consumerreports.org/medicare/pros-and-cons-of-medicare-advantage-a6834167849/

- https://vittana.org/14-chief-pros-and-cons-of-social-security

- https://www.benefitspro.com/2014/07/24/most-americans-not-familiar-with-annuities/

- https://www.benefitspro.com/2014/07/24/most-americans-not-familiar-with-annuities/

- https://www.consumeraffairs.com/health/long-term-care-statistics.html

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

-2.png)