/General/General%205.png?width=1280&height=853&name=General%205.png)

Healthcare Provider Update: Offers three medical plan options including UHC PPO and Surest, with 100% preventive care coverage. Employees also receive dental, vision, HSAs, FSAs, and wellness incentives 7. With ACA premiums rising and subsidies expiring, Equitys employer-sponsored plans may provide better value and predictability for employees. Click here to learn more

In March 2022, the Consumer Price Index for All Urban Consumers (CPI-U), the most common measure of inflation, rose at an annual rate of 8.5%, the highest level since December 1981.

1

It's not surprising that a Gallup poll at the end of March found that one out of six Americans considers inflation to be the most important problem facing the United States.

2

When inflation began rising in the spring of 2021, many economists, including policymakers at the Federal Reserve, believed the increase would be transitory and subside over a period of months. The inflation surge ultimately proved more stubborn than expected. It is helpful to understand the forces behind those rising prices, the Fed's response to combat them, and how the situation ultimately resolved.

Hot Economy Meets Russia and China

The fundamental cause of rising inflation continues to be the growing pains of a rapidly opening economy — a combination of pent-up consumer demand, supply-chain slowdowns, and not enough workers to fill open jobs. Loose Federal Reserve monetary policies and billions of dollars in government stimulus helped prevent a deeper recession but added fuel to the fire when the economy reopened.

The Russian invasion of Ukraine placed additional upward pressure on already high global fuel and food prices.

3

At the same time, a COVID resurgence in China led to strict lockdowns that closed factories and tightened already struggling supply chains for Chinese goods. The volume of cargo handled by the port of Shanghai, the world's busiest port, dropped by an estimated 40% in early April.

4

Behind the Headlines

Although the 8.5% year-over-year 'headline' inflation in March 2022 was a striking number for clients to consider at the time, monthly numbers provided a clearer picture of the trend. The month-over-month increase of 1.2% was extremely high, but more than half of it was due to gasoline prices, which rose 18.3% in March alone.

5

Despite the Russia-Ukraine conflict and increased seasonal demand, U.S. gas prices dropped in April, but the trend was moving upward by the end of the month.

6

The federal government's decision to release one million barrels of oil per day from the Strategic Petroleum Reserve for the next six months and allow summer sales of higher-ethanol gasoline may help moderate prices.

7

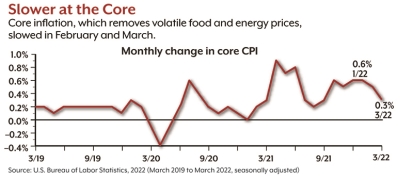

Core inflation, which strips out volatile food and energy prices, rose 6.5% year-over-year in March, the highest rate since 1982. However, it's important that our Equity Residential clients consider that the month-over-month increase from February to March was just 0.3%, the slowest pace in six months. Another positive sign was the price of used cars and trucks, which rose more than 35% over the last 12 months (a prime driver of general inflation) but dropped 3.8% in March.

8

Articles you may find interesting:

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

Wages and Consumer Demand

In March, average hourly earnings increased by 5.6% — but not enough to keep up with inflation and blunt the effects that impacted a variety of businesses, as well as many Equity Residential employees and retirees around the country. Lower-paid service workers received higher increases, with wages jumping by almost 15% for non-management employees in the leisure and hospitality industry. Although inflation cut deeply into wage gains over the prior year, wages have increased at about the same rate as inflation over the two-year period of the pandemic.

9

One of the central questions at the time was whether rising wages would enable consumers to continue to pay higher prices, which can lead to an inflationary spiral of ever-increasing wages and prices. Signals were mixed: consumer spending rose 1.1% in March 2022, but an early April 2022 poll found that two out of three Americans had already cut back on spending due to inflation.

10-11

Soft or Hard Landing?

The inflationary situation raised many questions about the path forward. The Federal Open Market Committee (FOMC) of the Federal Reserve laid out a plan to fight inflation by raising interest rates and tightening the money supply. After dropping the benchmark federal funds rate to near zero to stimulate the economy at the onset of the pandemic, the FOMC raised the rate by 0.25% at its March 2022 meeting and projected the equivalent of six more quarter-percent increases by the end of 2022 and three or four more in 2023.

12

That path was projected to bring the rate to around 2.75%, just above what the FOMC considered a 'neutral rate' that would neither stimulate nor restrain the economy.

13

Those rate increases successfully brought the Fed's preferred measure of inflation, the Personal Consumption Expenditures (PCE) Price Index, down toward the Fed's 2% target -- a gradual disinflation that played out through 2023 and 2024.

14

PCE inflation -- which had reached 6.6% in March 2022 -- tends to run below CPI; as the Fed's tightening took hold, both measures declined meaningfully through 2023 and 2024.

15

The FOMC went on to raise the fund's rate by 0.5% at its May 2022 meeting -- the first half-percent increase since May 2000 -- and continued hiking aggressively through 2022 and into 2023. The FOMC also reduced the Fed's bond holdings to tighten the money supply.

16

The question facing the FOMC is how fast it can raise interest rates and tighten the money supply while maintaining optimal employment and economic growth. The ideal is a 'soft landing,' similar to what occurred in the 1990s, when inflation was tamed without damaging the economy. At the other extreme is the 'hard landing' of the early 1980s, when the Fed raised the fund's rate to almost 20% in order to control runaway double-digit inflation, throwing the economy into a recession. 18

Fed Chair Jerome Powell acknowledges that a soft landing will be difficult to achieve, but he believes the strong job market may help the economy withstand aggressive monetary policies. Supply chains are expected to improve over time, and workers who have not yet returned to the labor force might fill open jobs without increasing wage and price pressures. 19

March 2022 did in fact represent the peak of that inflationary surge. Inflation trended lower through 2023 and 2024, though the descent was gradual. Employees and retirees are encouraged to revisit their financial plans in light of the current interest rate environment.

We'd like to remind our clients from Equity Residential that projections are based on current conditions, are subject to change, and may not come to pass.

1, 5, 8-9) U.S. Bureau of Labor Statistics, 2022

2) Gallup, March 29, 2022

3, 7) The New York Times, April 12, 2022

4) CNBC, April 7, 2022

6) AAA, April 25 & 29, 2022

10, 15) U.S. Bureau of Economic Analysis, 2022

11) CBS News, April 11, 2022

12, 14, 16) Federal Reserve, 2022

13, 17) The Wall Street Journal, April 18, 2022

18) The New York Times, March 21, 2022

What are the eligibility requirements for employees to participate in the Equity-League Pension Plan, and how can they ensure compliance with these requirements to maximize their potential benefits during retirement?

Eligibility for the Equity-League Pension Plan: Employees become eligible to participate in the Pension Plan by working at least two weeks in covered employment during a 12-month period. To maximize benefits, employees should ensure they continue working in covered employment to accumulate Years of Vesting Service (YVS), which solidifies their entitlement to benefits even if they leave the industry(Equity-League_Pension_T…).

How do the contribution limits for the Equity-League 401(k) Plan compare to traditional IRAs, and what strategies can employees deploy to make the most of their contribution options as they approach retirement?

Contribution Limits Comparison: The Equity-League 401(k) Plan has higher contribution limits compared to traditional IRAs. Employees can contribute up to $19,000 annually (or $25,000 if over 50), while traditional IRAs are capped at $6,000 (or $7,000 for those over 50). By taking full advantage of catch-up contributions as they near retirement, employees can significantly boost their retirement savings(Equity-League_Pension_T…).

What approaches can participants in the Equity-League Pension Plan take to effectively manage their individual accounts, and how can they adjust their investment strategies based on changes in their employment status or retirement goals?

Managing Individual Accounts in the Pension Plan: Participants in the Equity-League 401(k) Plan can manage their accounts by selecting from various investment options, including age-based and equity funds. Adjusting investments based on career changes or retirement goals can help employees align their portfolios with their risk tolerance and retirement timeline(Equity-League_Pension_T…).

In what ways can employees of the Equity-League Pension Plan benefit from understanding the vesting schedule, and how can this knowledge impact their overall retirement planning and decision-making process?

Vesting Schedule: Understanding the vesting schedule is crucial for employees. Employees become vested by accumulating five YVS or by satisfying other vesting tests, such as the 25-year test. Once vested, employees secure their pension benefits, regardless of future employment changes(Equity-League_Pension_T…).

What are the tax implications for participants in the Equity-League Pension Trust Fund when taking distributions from their retirement accounts, and how can they optimize their withdrawals to minimize tax liabilities?

Tax Implications for Distributions: When taking distributions from their retirement accounts, employees may face a 10% penalty if withdrawals are made before age 59½. However, rolling over distributions into IRAs can help defer taxes. Employees should consult tax professionals to optimize withdrawals and minimize tax liabilities(Equity-League_Pension_T…)(Equity-League_Pension_T…).

How can employees ensure that their beneficiary designations are current within the Equity-League Pension Plan, and what steps should they take in the event of a life change, such as marriage or divorce, to protect their intended beneficiaries?

Beneficiary Designations: It’s important for employees to keep beneficiary designations current. In the event of life changes such as marriage or divorce, updating these designations ensures intended beneficiaries receive the appropriate benefits. Employees can contact the Fund Office to make updates(Equity-League_Pension_T…)(Equity-League_Pension_T…).

What resources are available for employees of the Equity-League Pension Trust Fund to educate themselves about their retirement rights under ERISA, and how can they utilize these resources to advocate for their interests effectively?

ERISA Resources for Employees: Employees are protected under ERISA, which guarantees certain rights regarding their retirement benefits. The Equity-League Pension Trust Fund provides resources such as the Summary Plan Description, and employees can access legal help if they believe their rights have been violated(Equity-League_Pension_T…).

How does the withdrawal process work for employees of the Equity-League Pension Plan, particularly in the context of normal retirement age and circumstances that may lead to early withdrawals?

Withdrawal Process: Employees can take withdrawals as early as age 60, but benefits will be reduced for each year prior to age 65. Early withdrawals may also incur penalties, so employees should consider the long-term financial impact before opting for early retirement(Equity-League_Pension_T…).

Given the significant assets under management in the Equity-League Pension Trust Fund, how do investment choices within the plan impact employees' potential retirement income, and what factors should be considered when selecting these investments?

Investment Choices: Investment options within the 401(k) Plan impact employees' retirement income. With 19 investment choices, including equity and fixed-income investments, participants should select funds that balance growth and risk, keeping in mind the potential long-term returns(Equity-League_Pension_T…).

What is the best way for employees to contact the Equity-League Pension Trust Fund for inquiries about their benefits or the retirement process, and what specific information should they be prepared to provide to facilitate a productive conversation?

Contacting the Fund for Inquiries: Employees can contact the Equity-League Pension Trust Fund by phone, email, or mail. When making inquiries, employees should provide personal details such as their participant ID and questions about specific benefits to ensure efficient assistance(Equity-League_Pension_T…).

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

.webp?width=300&height=200&name=office-builing-main-lobby%20(27).webp)

-2.png)

.webp)