/General/General%202.png?width=1280&height=853&name=General%202.png)

In March 2022, the Consumer Price Index for All Urban Consumers (CPI-U), the most common measure of inflation, rose at an annual rate of 8.5%, the highest level since December 1981.

1

It's not surprising that a Gallup poll at the end of March found that one out of six Americans considers inflation to be the most important problem facing the United States.

2

When inflation began rising in the spring of 2021, many economists, including policymakers at the Federal Reserve, believed the increase would be transitory and subside over a period of months. The inflation surge ultimately proved more stubborn than expected. It is helpful to understand the forces behind those rising prices, the Fed's response to combat them, and how the situation ultimately resolved.

Hot Economy Meets Russia and China

The fundamental cause of rising inflation continues to be the growing pains of a rapidly opening economy — a combination of pent-up consumer demand, supply-chain slowdowns, and not enough workers to fill open jobs. Loose Federal Reserve monetary policies and billions of dollars in government stimulus helped prevent a deeper recession but added fuel to the fire when the economy reopened.

The Russian invasion of Ukraine placed additional upward pressure on already high global fuel and food prices.

3

At the same time, a COVID resurgence in China led to strict lockdowns that closed factories and tightened already struggling supply chains for Chinese goods. The volume of cargo handled by the port of Shanghai, the world's busiest port, dropped by an estimated 40% in early April.

4

Behind the Headlines

Although the 8.5% year-over-year 'headline' inflation in March 2022 was a striking number for clients to consider at the time, monthly numbers provided a clearer picture of the trend. The month-over-month increase of 1.2% was extremely high, but more than half of it was due to gasoline prices, which rose 18.3% in March alone.

5

Despite the Russia-Ukraine conflict and increased seasonal demand, U.S. gas prices dropped in April, but the trend was moving upward by the end of the month.

6

The federal government's decision to release one million barrels of oil per day from the Strategic Petroleum Reserve for the next six months and allow summer sales of higher-ethanol gasoline may help moderate prices.

7

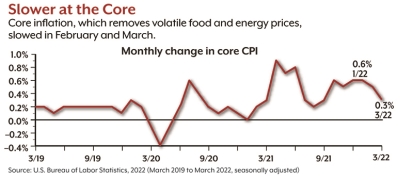

Core inflation, which strips out volatile food and energy prices, rose 6.5% year-over-year in March, the highest rate since 1982. However, it's important that our University of Chicago clients consider that the month-over-month increase from February to March was just 0.3%, the slowest pace in six months. Another positive sign was the price of used cars and trucks, which rose more than 35% over the last 12 months (a prime driver of general inflation) but dropped 3.8% in March.

8

Articles you may find interesting:

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

Wages and Consumer Demand

In March, average hourly earnings increased by 5.6% — but not enough to keep up with inflation and blunt the effects that impacted a variety of businesses, as well as many University of Chicago employees and retirees around the country. Lower-paid service workers received higher increases, with wages jumping by almost 15% for non-management employees in the leisure and hospitality industry. Although inflation cut deeply into wage gains over the prior year, wages have increased at about the same rate as inflation over the two-year period of the pandemic.

9

One of the central questions at the time was whether rising wages would enable consumers to continue to pay higher prices, which can lead to an inflationary spiral of ever-increasing wages and prices. Signals were mixed: consumer spending rose 1.1% in March 2022, but an early April 2022 poll found that two out of three Americans had already cut back on spending due to inflation.

10-11

Soft or Hard Landing?

The inflationary situation raised many questions about the path forward. The Federal Open Market Committee (FOMC) of the Federal Reserve laid out a plan to fight inflation by raising interest rates and tightening the money supply. After dropping the benchmark federal funds rate to near zero to stimulate the economy at the onset of the pandemic, the FOMC raised the rate by 0.25% at its March 2022 meeting and projected the equivalent of six more quarter-percent increases by the end of 2022 and three or four more in 2023.

12

That path was projected to bring the rate to around 2.75%, just above what the FOMC considered a 'neutral rate' that would neither stimulate nor restrain the economy.

13

Those rate increases successfully brought the Fed's preferred measure of inflation, the Personal Consumption Expenditures (PCE) Price Index, down toward the Fed's 2% target -- a gradual disinflation that played out through 2023 and 2024.

14

PCE inflation -- which had reached 6.6% in March 2022 -- tends to run below CPI; as the Fed's tightening took hold, both measures declined meaningfully through 2023 and 2024.

15

The FOMC went on to raise the fund's rate by 0.5% at its May 2022 meeting -- the first half-percent increase since May 2000 -- and continued hiking aggressively through 2022 and into 2023. The FOMC also reduced the Fed's bond holdings to tighten the money supply.

16

The question facing the FOMC is how fast it can raise interest rates and tighten the money supply while maintaining optimal employment and economic growth. The ideal is a 'soft landing,' similar to what occurred in the 1990s, when inflation was tamed without damaging the economy. At the other extreme is the 'hard landing' of the early 1980s, when the Fed raised the fund's rate to almost 20% in order to control runaway double-digit inflation, throwing the economy into a recession. 18

Fed Chair Jerome Powell acknowledges that a soft landing will be difficult to achieve, but he believes the strong job market may help the economy withstand aggressive monetary policies. Supply chains are expected to improve over time, and workers who have not yet returned to the labor force might fill open jobs without increasing wage and price pressures. 19

March 2022 did in fact represent the peak of that inflationary surge. Inflation trended lower through 2023 and 2024, though the descent was gradual. Employees and retirees are encouraged to revisit their financial plans in light of the current interest rate environment.

We'd like to remind our clients from University of Chicago that projections are based on current conditions, are subject to change, and may not come to pass.

1, 5, 8-9) U.S. Bureau of Labor Statistics, 2022

2) Gallup, March 29, 2022

3, 7) The New York Times, April 12, 2022

4) CNBC, April 7, 2022

6) AAA, April 25 & 29, 2022

10, 15) U.S. Bureau of Economic Analysis, 2022

11) CBS News, April 11, 2022

12, 14, 16) Federal Reserve, 2022

13, 17) The Wall Street Journal, April 18, 2022

18) The New York Times, March 21, 2022

What are the eligibility criteria for participation in the SEPP plan for employees of The University of Chicago, and how can factors like years of service and age impact an employee's benefits under this plan? Discuss how these criteria might have changed for new employees post-2016 and what implications this has for retirement planning.

Eligibility Criteria for SEPP: Employees at The University of Chicago become eligible to participate in the SEPP upon meeting age and service requirements: being at least 21 years old and completing one year of service. For employees hired after the plan freeze on October 31, 2016, these criteria have been crucial in determining eligibility for newer employees, impacting their retirement planning as they do not accrue benefits under SEPP beyond this freeze date.

In what ways does the SEPP (Staff Employees Pension Plan) benefit calculation at The University of Chicago reflect an employee's years of service and final average pay? Examine the formulas involved in the benefits determination process, including how outside factors such as Social Security compensation can affect the total pension benefits an employee receives at retirement.

Benefit Calculation Reflecting Service and Pay: The SEPP benefits are calculated based on the final average pay and years of participation, factoring in Social Security covered compensation. Changes post-2016 have frozen benefits accrual, meaning that current employees’ benefits are calculated only up to this freeze date, affecting long-term benefits despite continued employment.

How can employees at The University of Chicago expect their SEPP benefits to be paid out upon their retirement, especially in terms of the options between lump sum distributions and annuities? Analyze the advantages and disadvantages of each payment option, and how these choices can impact an employee's financial situation in retirement.

Payout Options (Lump Sum vs. Annuities): Upon retirement, employees can opt for a lump sum payment or annuities. Each option presents financial implications; lump sums provide immediate access to funds but annuities offer sustained income. This choice is significant for financial stability in retirement, particularly under the constraints post the 2016 plan changes.

Can you elaborate on the spousal rights associated with the pension benefits under the SEPP plan at The University of Chicago? Discuss how marital status influences annuity payments and the required spousal consent when considering changes to beneficiary designations.

Spousal Rights in SEPP Benefits: Spouses have rights to pension benefits, requiring spousal consent for altering beneficiary arrangements under the SEPP. Changes post-2016 do not impact these rights, but understanding these is vital for making informed decisions about pension benefits and beneficiary designations.

As an employee nearing retirement at The University of Chicago, what considerations should one keep in mind regarding taxes on pension benefits received from the SEPP? Explore the tax implications of different types of distributions and how they align with current IRS regulations for the 2024 tax year.

Tax Considerations for SEPP Benefits: SEPP distributions are taxable income. Employees must consider the tax implications of their chosen payout method—lump sum or annuities—and plan for potential tax liabilities. This understanding is crucial, especially with the plan’s benefit accrual freeze affecting the retirement timeline.

What resources are available for employees of The University of Chicago wishing to understand more about their retirement benefits under SEPP? Discuss the types of information that can be requested from the Benefits Office and highlight the contact methods for obtaining more detailed assistance.

Resources for Understanding SEPP Benefits: The University provides resources for employees to understand their SEPP benefits, including access to the Benefits Office for personalized queries. Utilizing these resources is essential for employees, especially newer ones post-2016, to fully understand their retirement benefits under the current plan structure.

How does The University of Chicago address benefits for employees upon their death, and what provisions exist for both spouses and non-spouse beneficiaries under the SEPP plan? Analyze the specific benefits and payment structures available to beneficiaries and the conditions under which these benefits are distributed.

Posthumous Benefits: The SEPP includes provisions for spouses and non-spouse beneficiaries, detailing the continuation or lump sum payments upon the death of the employee. Understanding these provisions is crucial for estate planning and ensuring financial security for beneficiaries.

What factors ensure an employee remains fully vested in their pension benefits with The University of Chicago, and how does the vesting schedule affect retirement planning strategies? Consider the implications of not fulfilling the vesting criteria and how this might influence decisions around employment tenure and retirement timing.

Vesting and Retirement Planning: Vesting in SEPP requires three years of service, with full benefits contingent on meeting this criterion. For employees navigating post-2016 changes, understanding vesting is crucial for retirement planning, particularly as no additional benefits accrue beyond the freeze date.

Discuss the impact of a Qualified Domestic Relations Order (QDRO) on the SEPP benefits for employees at The University of Chicago. How do divorce or separation proceedings influence pension benefits, and what steps should employees take to ensure compliance with a QDRO?

Impact of QDROs on SEPP Benefits: SEPP complies with Qualified Domestic Relations Orders, which can allocate pension benefits to alternate payees. Understanding how QDROs affect one’s benefits is crucial for financial planning, especially in the context of marital dissolution.

How can employees at The University of Chicago, who have questions about their benefits under the SEPP plan, effectively communicate with the Benefits Office for clarity and assistance? Specify the various communication methods available for employees and what kind of information or support they can expect to receive.

Communicating with the Benefits Office: Employees can reach out to the Benefits Office via email or phone for detailed assistance on their SEPP benefits. Effective communication with this office is vital for employees to clarify their benefits status, particularly in light of the post-2016 changes to the plan.

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

.webp?width=300&height=200&name=office-builing-main-lobby%20(27).webp)

-2.png)

.webp)