/General/General%203.png?width=1280&height=853&name=General%203.png)

Healthcare Provider Update: Offers four medical plan options, dental and vision coverage, HSAs/FSAs, 401(k) with match, ESPP, wellness programs, and tuition reimbursement. As ACA premiums rise, Coparts customizable plans and employer contributions help employees avoid steep out-of-pocket costs Click here to learn more

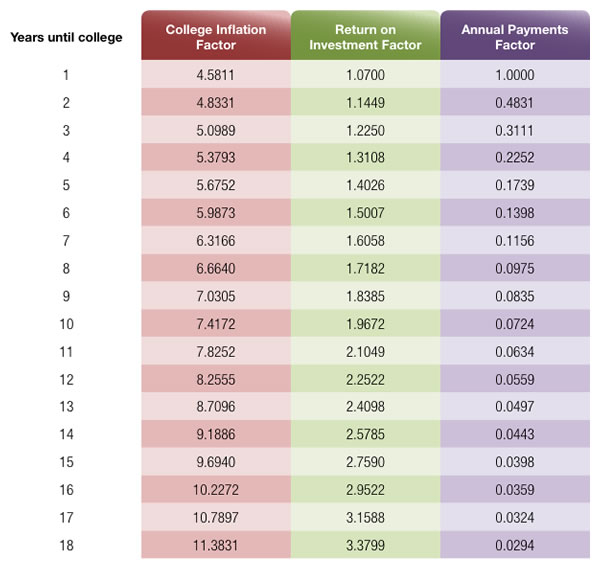

It doesn’t take a degree in finance to see the cost of college continues to rise.

In its 2017 report, the College Board showed that public four-year institutions raised prices an average of 3.2% annually between the 2007-08 and 2017-18 school years. Put another way, a $5,000 education in 2007-08 would cost $6,851 in 2017-18.

For a few families, the lion’s share of education costs falls on parents and, in some cases, on grandparents. For our Copart clients who are parents you may already know, generally, the majority of families rely on a combination of scholarships, grants, financial aid, part-time jobs, and parent support to help pay the cost.

For Copart employees who have children approaching college age, a good first step is estimating the potential costs. The accompanying worksheet can help you get a better idea about the cost of a four-year college.

For Copart employees who already put money away for college, the worksheet will take that amount into consideration. For Copart employees who haven’t, it’s never too late to start.

Resources

There are a number of resources that can help individuals prepare for college. The U.S. government distributes certain information on colleges and costs. Here are two sites for these Copart employees to consider reviewing:

www.studentaid.ed.gov

The government’s college and financial aid portal.

Featured Video

Articles you may find interesting:

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

www.collegeboard.org

The group that administers the SAT test.

Estimating the Cost of College

What is the Copart 401(k) plan?

The Copart 401(k) plan is a retirement savings plan that allows employees to save for their future by contributing a portion of their salary on a pre-tax or after-tax basis.

How can I enroll in Copart's 401(k) plan?

You can enroll in Copart's 401(k) plan by completing the enrollment process through the company’s benefits portal or by contacting the HR department for assistance.

Does Copart match employee contributions to the 401(k) plan?

Yes, Copart offers a matching contribution to the 401(k) plan, which helps employees maximize their retirement savings.

What is the maximum contribution limit for Copart's 401(k) plan?

The maximum contribution limit for Copart's 401(k) plan is determined by the IRS and may change annually; employees should check the latest IRS guidelines for the current limit.

When can I start contributing to Copart's 401(k) plan?

Employees at Copart can start contributing to the 401(k) plan after completing their eligibility period, which is typically outlined in the employee handbook.

What investment options are available in Copart's 401(k) plan?

Copart's 401(k) plan offers a variety of investment options, including mutual funds, stocks, and bonds, allowing employees to choose based on their risk tolerance and retirement goals.

Can I take a loan from my Copart 401(k) account?

Yes, Copart allows employees to take loans from their 401(k) accounts under certain conditions, but it’s important to review the specific terms and repayment requirements.

What happens to my Copart 401(k) if I leave the company?

If you leave Copart, you have several options for your 401(k), including rolling it over to a new employer's plan, transferring it to an IRA, or cashing it out (though this may incur taxes and penalties).

How often can I change my contribution amount to Copart's 401(k) plan?

Employees can typically change their contribution amount to Copart's 401(k) plan at any time, subject to the plan's specific rules regarding frequency and timing.

Is there a vesting schedule for Copart's 401(k) matching contributions?

Yes, Copart has a vesting schedule for matching contributions, meaning that employees must work for a certain period before they fully own the employer contributions.

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

.webp?width=300&height=200&name=office-builing-main-lobby%20(27).webp)

-2.png)

.webp)