/General/General%203.png?width=1280&height=853&name=General%203.png)

Healthcare Provider Update: Healthcare Provider for IAC IAC, officially known as IAC/InterActiveCorp, is known for its diverse portfolio of subsidiaries across various industries, including media, technology, and telecommunications. The primary healthcare provider associated with IAC is UnitedHealthcare, which is the health insurance division of UnitedHealth Group. UnitedHealthcare provides a range of healthcare plans and services, including individual and family coverage through platforms such as the Affordable Care Act (ACA) marketplace. --- Potential Healthcare Cost Increases in 2026 As the healthcare landscape evolves, significant premium hikes are expected for ACA marketplace plans in 2026, with some states reporting increases exceeding 60%. This surge in costs is attributed to rising medical expenses, the potential expiration of enhanced federal subsidies, and aggressive rate hikes from major insurers like UnitedHealthcare. A staggering 92% of policyholders may face an out-of-pocket increase of over 75% if subsidies are not renewed, highlighting a challenging financial outlook for millions relying on affordable healthcare options. It's essential for consumers to be proactive in managing their healthcare decisions amidst this anticipated landscape. Click here to learn more

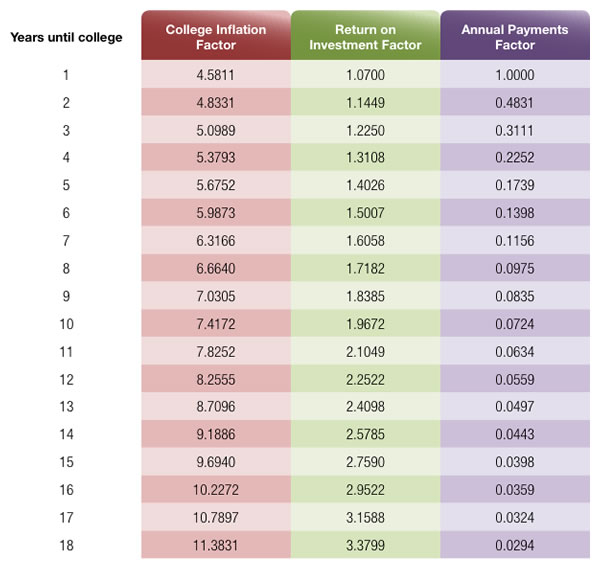

It doesn’t take a degree in finance to see the cost of college continues to rise.

In its 2017 report, the College Board showed that public four-year institutions raised prices an average of 3.2% annually between the 2007-08 and 2017-18 school years. Put another way, a $5,000 education in 2007-08 would cost $6,851 in 2017-18.

For a few families, the lion’s share of education costs falls on parents and, in some cases, on grandparents. For our IAC clients who are parents you may already know, generally, the majority of families rely on a combination of scholarships, grants, financial aid, part-time jobs, and parent support to help pay the cost.

For IAC employees who have children approaching college age, a good first step is estimating the potential costs. The accompanying worksheet can help you get a better idea about the cost of a four-year college.

For IAC employees who already put money away for college, the worksheet will take that amount into consideration. For IAC employees who haven’t, it’s never too late to start.

Resources

There are a number of resources that can help individuals prepare for college. The U.S. government distributes certain information on colleges and costs. Here are two sites for these IAC employees to consider reviewing:

www.studentaid.ed.gov

The government’s college and financial aid portal.

Featured Video

Articles you may find interesting:

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

www.collegeboard.org

The group that administers the SAT test.

Estimating the Cost of College

What is the IAC 401(k) plan?

The IAC 401(k) plan is a retirement savings plan that allows employees to save a portion of their paycheck before taxes are taken out, helping them prepare for retirement.

How can I enroll in the IAC 401(k) plan?

Employees can enroll in the IAC 401(k) plan by accessing the enrollment portal through the company’s HR website or by contacting the HR department for assistance.

Does IAC offer a matching contribution for the 401(k) plan?

Yes, IAC provides a matching contribution to the 401(k) plan, which helps employees maximize their retirement savings.

What is the eligibility requirement to participate in the IAC 401(k) plan?

Employees are generally eligible to participate in the IAC 401(k) plan after completing a specific period of service, as outlined in the plan documents.

What types of investment options are available in the IAC 401(k) plan?

The IAC 401(k) plan offers a variety of investment options, including mutual funds, target-date funds, and other investment vehicles to help employees diversify their savings.

Can I change my contribution rate to the IAC 401(k) plan?

Yes, employees can change their contribution rate to the IAC 401(k) plan at any time by accessing their account online or contacting HR.

What happens to my IAC 401(k) account if I leave the company?

If you leave IAC, you have several options for your 401(k) account, including rolling it over to a new employer’s plan or an individual retirement account (IRA).

Are there any fees associated with the IAC 401(k) plan?

Yes, there may be administrative fees and investment-related fees associated with the IAC 401(k) plan, which are detailed in the plan documents.

How can I access my IAC 401(k) account information?

Employees can access their IAC 401(k) account information through the online portal provided by the plan administrator.

What is the vesting schedule for IAC's matching contributions?

The vesting schedule for IAC's matching contributions is outlined in the plan documents, and it typically requires employees to work for a certain number of years before fully owning the match.

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

.webp?width=300&height=200&name=office-builing-main-lobby%20(27).webp)

-2.png)

.webp)