/General/General%202.png?width=1280&height=853&name=General%202.png)

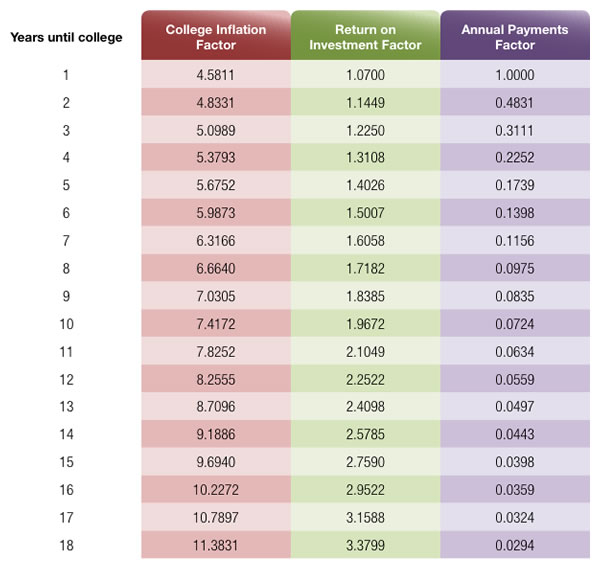

It doesn’t take a degree in finance to see the cost of college continues to rise.

In its 2017 report, the College Board showed that public four-year institutions raised prices an average of 3.2% annually between the 2007-08 and 2017-18 school years. Put another way, a $5,000 education in 2007-08 would cost $6,851 in 2017-18.

For a few families, the lion’s share of education costs falls on parents and, in some cases, on grandparents. For our Nationwide clients who are parents you may already know, generally, the majority of families rely on a combination of scholarships, grants, financial aid, part-time jobs, and parent support to help pay the cost.

For Nationwide employees who have children approaching college age, a good first step is estimating the potential costs. The accompanying worksheet can help you get a better idea about the cost of a four-year college.

For Nationwide employees who already put money away for college, the worksheet will take that amount into consideration. For Nationwide employees who haven’t, it’s never too late to start.

Resources

There are a number of resources that can help individuals prepare for college. The U.S. government distributes certain information on colleges and costs. Here are two sites for these Nationwide employees to consider reviewing:

www.studentaid.ed.gov

The government’s college and financial aid portal.

Featured Video

Articles you may find interesting:

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

- Corporate Employees: 8 Factors When Choosing a Mutual Fund

- Use of Escrow Accounts: Divorce

- Medicare Open Enrollment for Corporate Employees: Cost Changes in 2024!

- Stages of Retirement for Corporate Employees

- 7 Things to Consider Before Leaving Your Company

- How Are Workers Impacted by Inflation & Rising Interest Rates?

- Lump-Sum vs Annuity and Rising Interest Rates

- Internal Revenue Code Section 409A (Governing Nonqualified Deferred Compensation Plans)

- Corporate Employees: Do NOT Believe These 6 Retirement Myths!

- 401K, Social Security, Pension – How to Maximize Your Options

- Have You Looked at Your 401(k) Plan Recently?

- 11 Questions You Should Ask Yourself When Planning for Retirement

- Worst Month of Layoffs In Over a Year!

www.collegeboard.org

The group that administers the SAT test.

Estimating the Cost of College

What are the unique benefits provided by the Nationwide Retirement Plan that differentiate it from other retirement plans? How does Nationwide Mutual Insurance Company ensure the plan meets the regulatory requirements while still addressing the needs of its employees?

Unique Benefits of Nationwide Retirement Plan: Nationwide’s Retirement Plan provides both a Final Average Pay (FAP) Benefit and an Account Balance Benefit, which allows flexibility for employees hired at different times. The plan is qualified under Section 401(a) of the Internal Revenue Code, ensuring compliance with federal tax laws. Nationwide ensures regulatory compliance while addressing employee needs through ongoing contributions, actuarial evaluations, and options like lifetime income for retirees and survivors.

How can employee participation in the Nationwide Retirement Plan impact their overall retirement savings strategy? What role does the defined benefit pension plan play in conjunction with Social Security and personal savings for employees of Nationwide Mutual Insurance Company?

Employee Participation Impact: Participation in the Nationwide Retirement Plan enhances employees' overall retirement savings strategy by integrating Social Security, personal savings, and the defined benefit plan. The FAP benefit, based on final average compensation, works alongside Social Security to offer a stable income, while the Account Balance Benefit adds flexibility in retirement income options.

What options do employees of Nationwide Mutual Insurance Company have when they retire before the age of 55, and how do these options compare to those available for employees who retire after reaching that age? What factors influence the choices employees make regarding timing and type of benefit commencement?

Retirement Options Before and After Age 55: Employees retiring before age 55 can start receiving their benefits immediately, but they face early retirement reductions. Those retiring after age 55 may choose from more benefit options like annuities and receive higher, less-reduced payments. The choice to retire before or after age 55 depends on factors like financial need and health, and affects the timing and size of the benefit commencement(Nationwide Mutual Insur…).

In what ways does the structure of the benefit formulas—Final Average Pay (FAP) Benefit and Account Balance Benefit—affect the retirement income of employees at Nationwide Mutual Insurance Company? What are the implications for employees considering different retirement timings?

Effect of Benefit Formulas on Income: The FAP Benefit is based on Final Average Pay and Social Security coordination, offering a larger benefit for those with higher incomes, while the Account Balance Benefit is based on accumulated contributions and interest. The timing of retirement plays a crucial role in determining income, as early retirement results in reduced benefits, while late retirement allows for continued service accrual and potentially higher payouts.

How does the Nationwide Mutual Insurance Company address spousal benefits under the retirement plan, particularly regarding the Qualified Preretirement Survivor Annuity (QPSA)? What are the actions that employees need to take to ensure their spouses receive these benefits?

Spousal Benefits and QPSA: Nationwide offers a Qualified Preretirement Survivor Annuity (QPSA) to ensure that a spouse receives benefits if the participant dies before retirement. Employees must name their spouse as a beneficiary or obtain notarized consent if they wish to designate someone else. To ensure the spouse receives the QPSA, employees must take the appropriate legal steps outlined in the plan.

What steps must employees of Nationwide Mutual Insurance Company take to successfully file a claim for retirement benefits, and what is the timeframe for processing these claims? How does the company ensure that employees understand their rights under the Employee Retirement Income Security Act (ERISA)?

Steps to File a Claim for Retirement Benefits: To file a claim, employees must notify the Nationwide Retirement Center at Fidelity and submit the required paperwork. Claims are typically processed within 60 days, and Nationwide ensures that employees understand their rights under ERISA through detailed communications and support from Fidelity Investments.

What are the situations that might cause delays or loss of benefits for employees retiring from Nationwide Mutual Insurance Company? How can employees proactively manage these risks to ensure they receive their entitled benefits?

Situations Leading to Delays or Loss of Benefits: Delays can occur if employees fail to submit necessary paperwork, keep their contact information updated, or if they are not vested at the time of severance. Employees should proactively manage these risks by completing forms timely and maintaining communication with the Plan Administrator to avoid disruptions in benefits.

Can employees at Nationwide Mutual Insurance Company alter their distribution choices after commencing their retirement benefits? What regulatory frameworks influence their ability to change benefit elections, and under what circumstances might these changes be permitted?

Changing Distribution Choices After Retirement: Once retirement benefits commence, changes to distribution elections are limited. For example, lump-sum payments and annuity selections are typically irrevocable after commencement, and spousal consent is required for certain changes. Federal regulations, such as IRS rules, further restrict post-retirement changes in benefit elections(Nationwide Mutual Insur…).

How does the Nationwide Mutual Insurance Company plan for automatic post-retirement benefit increases, and what factors determine the percentage increase? How do these increases impact the long-term financial security of retirees?

Post-Retirement Benefit Increases: Nationwide offers automatic post-retirement benefit increases for participants with service before 1996, with annual increases between 0% and 3% based on fund performance. These increases help to protect retirees’ long-term financial security by adjusting their pension income for inflation.

How can employees contact NDPERS for more information regarding their retirement options, and what specific resources are available for personalized assistance? Clear communication channels and support services are essential for helping employees navigate their retirement planning effectively with NDPERS.

Contacting the Nationwide Retirement Center: Employees can reach the Nationwide Retirement Center at Fidelity by calling 1-800-238-4015 for inquiries about their retirement plan. Fidelity provides detailed support, including benefit estimates, plan information, and assistance with filing claims and selecting benefit distribution options(Nationwide Mutual Insur…).

-2.png?width=300&height=200&name=office-builing-main-lobby%20(52)-2.png)

.webp?width=300&height=200&name=office-builing-main-lobby%20(27).webp)

-2.png)

.webp)