Tax Code Updates for 2025

Staying informed about new changes made by the IRS is critically important. For employees in the United States, particularly those in their 50s or 60s, the critical factors to keep track of are the following:

- Standard deduction. In 2025, the standard deduction increased to $15,000 for single filers and married filing separately; $30,000 for joint filers, and $22,500 for heads of household.

- Additional deduction. Taxpayers who are over the age of 65 or blind can add an additional $1,600 to their standard deduction. This amount jumps to $2,000 if they are also unmarried or not a surviving spouse.

- Cash contributions to charity. The special deduction that allowed non-itemizers to deduct up to $300 in cash donations to charity — or $600 for those married filing jointly — has expired.

Many individuals interested in reducing their tax burdens as much as possible are excited to learn about the Child Tax Credit. Although it only applies to those with children under the age of 18, it can be relevant to those who are approaching retirement if they have minor children — or if their children have children!

Child Tax Credit updates for 2025:

- Maximum credit per qualifying child: $2,000 for children 5 and under; $3,000 for children 6 through 17.

- Child Tax Credit eligibility. As a parent or guardian, you are eligible for the Child Tax Credit if your adjusted gross income is less than $200,000, or $400,000 married filing jointly.

- Partial refundability. If your Child Tax Credit is greater than your tax, you can receive up to $1,600 as a cash refund.

Other notable changes for tax year 2025 include the following:

- Alternative minimum tax exemption amounts: For 2025, the exemption amount for unmarried individuals increases to $88,100 ($68,650 for married individuals filing separately) and begins to phase out at $626,350. For married couples filing jointly, the exemption amount increases to $137,000 and begins to phase out at $1,252,700.

- Qualified transportation fringe benefit: For 2025, the monthly limitation for the qualified transportation fringe benefit and the monthly limitation for qualified parking rises to $325 per month, increasing from $315 per month in 2024.

- Health flexible spending cafeteria plans: For the taxable years beginning in 2025, the dollar limitation for employee salary reductions for contributions to health flexible spending arrangements rises to $3,300, increasing from $3,200 in 2024. For cafeteria plans that permit the carryover of unused amounts, the maximum carryover amount rises to $660, increasing from $640 in 2024.

- Medical savings accounts: For 2025, participants who have self-only coverage, the plan must have an annual deductible that is not less than $2,850 (a $50 increase from the previous tax year), but not more than $4,300 (an increase of $150 from the previous tax year). The maximum out-of-pocket expense amount rises to $5,700, increasing from $5,550 in 2024. For family coverage in 2025, the annual deductible is not less than $5,700, increasing from $5,550 in 2024; however, the deductible cannot be more than $8,550, an increase of $200 versus the limit for 2024. For family coverage, the out-of-pocket expense limit is $10,500 for 2025, rising from $10,200 in 2024.

- Foreign earned income exclusion: For 2025, the foreign earned income exclusion increases to $130,000, from $126,500 in 2024.

- Estate tax credits: Estates of decedents who die during 2025 have a basic exclusion amount of $13,990,000, increased from $13,610,000 for estates of decedents who died in 2024.

- Annual exclusion for gifts: This increases to $19,000 for calendar year 2025, rising from $18,000 for calendar year 2024.

- Adoption credits: For 2025, the maximum credit allowed for an adoption of a child with special needs is the amount of qualified adoption expenses up to $17,280, increased from $16,810 for 2024.

How AT&T employees can optimize their retirement contributions

Contributing to your company's 401(k) plan can cut this year's tax bill significantly. With the right planning, these benefits can be compounded over time. In 2025, the amount you can save increased:

- 2025 limit. Individuals can contribute $23,500 to their 401(k) plans in 2025.

- Catch-up contributions. Employees age 50 and over can contribute an extra $7,500, bringing their total limit to $31,000. For those who are 60 - 63 years of age in 2025, their catch-up provision is $11,250 for a combined total of $34,750.

- A major opportunity. Lowering your taxable income by up to $34,750 means less of your money is immediately taxed. As displayed by the table below, this could save you thousands on your current tax bill.

Many investors choose to invest the money that they save in taxes this year. This bonus nest egg then has the opportunity to grow in the market, which can help pay the deferred tax when they make withdrawals from their accounts later in life.

Addressing inflation in 2025

Following the searing rates of inflation Americans experienced in the early 2020s, the inflation rate of 2.9% for calendar year 2024 seems much more palatable (Source: Bureau of Labor Statistics). Still, inflation is still considered a volatile source of risk to your portfolio, and will reduce the purchasing power of your dollars over time whether you like it or not.

The Federal Reserve strives to achieve a 2% inflation rate each year, but the 8.3% inflation rate of 2022 reminded all of us that this target is anything but a guarantee. In order to maintain the same standard of living throughout your retirement after leaving AT&T, you will have to factor rising costs into your plan. This is doubly important for important sectors like health care and housing, which have been known to outpace the total inflation rate, sometimes by significant amounts.

An experienced advisor can help you prepare your portfolio for inflation, while taking into account the rest of your comprehensive plan. Speak with a financial advisor today to start planning for the impacts.

*Source: IRS.gov, Yahoo, Bankrate, Forbes

![]()

Retirement planning isn't a one-and-done activity. But it's not something you can put off forever.

The truth is, most Americans don't know how much they need for retirement. However, when we look at the realities of planning, this may not be too much of a surprise. Retirement planning is a complex activity that must be done regularly, whether you're 30 or 60. And for many of us, the gravity of that complexity leads us to delay planning — sometimes, until it's nearly too late.

No matter where you're at in the planning process now, it's time to reevaluate. You know you need to be saving and investing, because "time in the market" beats "timing the market". But even if you've been investing for years, the game changes entirely once you switch from saving to spending.

That's where The Retirement Group comes in. We've partnered with Wealth Enhancement to offer a wide range of retirement planning resources. With a qualified, competent, and caring advising team by your side, AT&T employees in the United States can make the most of what they've saved, and better plan for what they still need.

Don't leave your retirement transition to chance. Whether you're focused on maximizing the potential of your benefits, planning for rising health care costs, or creating effective tax diversification in your portfolio, The Retirement Group can help.

Source: Is it Worth the Money to Hire a Financial Advisor? The Balance, 2021

Investing in the AT&T 401(k) Program

Compound interest has been referred to as the "8th Wonder of the World". When you invest money, and re-invest the proceeds from those investments, your money compounds. Over time, this compounding can have a significant effect on the value of your portfolio. That's why starting to invest as early as possible matters so much. The AT&T 401(k) program offers a prime opportunity for employees to invest and save, reaping the benefits of compound interest.

The benefits of investing in your 401(k)

401(k)s offer significant benefits for those who invest in them:

- Tax-deferment: When you invest money in a 401(k), it is removed from your taxable income for the year in which you invest. Not only does this reduce your tax bill for this year, it allows you to invest the amount you saved. The potential proceeds from these investments can help you pay the deferred taxes when you make withdrawals in retirement.

- Employer match: Many employers offer what's referred to as a "match", which means they will match up to a certain amount of money that you invest in your 401(k) each year. We'll explain the details later in this section.

- Compound interest: 401(k)s as an investment account allow you to take advantage of compound interest, which we illustrate below.

Waiting to invest in your 401(k) can cost you. This hypothetical illustration shows the potential risks of waiting just 10 years to start investing in an IRA. Assuming a $100 monthly investment and an annual return of 8%, an investor who starts at age 25 instead of age 35 would have an extra $200,000 in their account when they reach age 65. This example certainly underscores the importance of starting early, but it also illustrates the importance of repeated, continuous investment. $100 a month might not seem like a lot to start out with, but by sticking with it, both of the investors in our example amassed a significant nest egg that will be able to support them in retirement.

401(k) investing: Benchmarks by decade

The further you get in your career, the greater your income. This general rule may makes it appear that individuals in their mid to late careers have more money that they can invest. However, retirement saving competes directly with a number of other expenses, like your mortgage, raising children, paying for college, and more.

In the United States, it's important to develop a strategy for 401(k) investing that you can stick to. Strategies always vary from person to person, because everyone's financial situation is unique, but there are some popular benchmarks that you can keep track of:

- If you're in your 30s and 40s, retirement planning often conflicts with saving for college. While many financial planners will tell you to focus on retirement, because financial aid can offset tuition costs, consider investing a minimum of 10% of your income toward retirement during this age range.

- As you enter your 50s and 60s, you'll ideally be in your peak earning years — and with some major expenses behind you. This can be a good time to consider whether or not you can boost your retirement savings goal to 20% or more of your income. For many of us, this is the last time we have to stash away funds.

- Starting at age 50, retirement investors are allowed to make “catch-up” contributions to certain types of accounts. These contributions allow you to save even more as you navigate the home stretch into retirement.

Why are 401(k) matching contributions so popular?

Matching contributions are just what they sound like: Your company matches your own personal 401(k) contributions up to some point, using money that comes from the company. Typically, if your employer offers a match, they will match up to a certain percent of the amount that you invest.

For example, let's say AT&T offers you a 5% match to your 401(k) investments. If your salary is $100,000 and you invest $5,000 in your 401(k), AT&T would then match that amount, also investing $5,000 in your 401(k) — resulting in a $10,000 increase to your 401(k) balance. If you invested $10,000 instead, AT&T would match $5,000 of that amount, bringing your total annual 401(k) investment to $15,000 for that year.

401(k) employer match contributions are so popular because they are effectively "free money". If you don't invest enough to take full advantage of your employer's match, then you are leaving money on the table. Research published by Principal Financial Group in 2022 found that 62% of workers deemed company 401(k) matches significantly important to reaching their retirement goals.

Unfortunately, many people fail to take advantage of these programs. According to Bank of America's "2022 Financial Life Benefit Impact Report", despite 58% of eligible employees participating in a 401(k) plan, 61% of them contributed less than $5,000 during the current year. The study also found that fewer than one in 10 participants’ contributions reached the ceiling on elective deferrals, under IRS Section 402(g) — which is $23,500 for 2025.

A 2020 study from Financial Engines titled “Missing Out: How Much Employer 401(k) Matching Contributions Do Employees Leave on the Table?”, revealed that employees who don’t maximize their company match typically leave $1,336 of extra retirement money on the table each year. That amount of money could make a serious difference to your retirement portfolio.

AT&T employees in the United States stand to benefit from the information in this article! Read Wealth Enhancement's "Complete Guide to Retirement Accounts" article, or speak with an AT&T-focused advisor by clicking the button below.

AT&T Pension Plan Overview & Examples

The AT&T Pension Benefit Plan is a defined benefit pension plan and a defined contribution pension plan, sponsored by AT&T. The company created various pension plans based on different groups of employees. In this guide, we'll be discussing the pension plans specifically for Management and Hourly employees in the United States. These are different plans, and yours may differ, but in general, most plans behave similarly for participants across all ages.

Benefits under the plan are provided through separate programs. A "program" is the portion of the plan that provides benefits to a particular group of participants or beneficiaries. For example

- Management employees are eligible for plans like the Cash Balance Account (although it was frozen in 2002) and the Current Active Management (CAM) Plan.

- Hourly employees are eligible for benefits calculated by the "Pension Band System", which determines payout options based on job role and years of experience.

First, we will cover the eligibility and vesting of benefits.

Management - Cash Balance Account

In 1997 Joe Smith switches to Management and participates in the Cash Balance Account:

- - After 5 years of service Joe will be fully vested with no term age penalties

- - If he receives salary increases, this will affect the calculation of his final benefit

- - Joe will receive his benefit in the form of a Lump Sum, upon retirement

- - In May of 2002 this account type was frozen by AT&T

Now we’ll discuss CAM. This is the plan that the majority of managers fall under today. It was introduced in 2001 and is the only plan that currently isn’t frozen.

In 2001, Joe starts his CAM pension plan:

CAM Pension Plan

- - Assume $0 opening balance as he came from Hourly

- - Joe was hired before 6/12/01 so he is fully vested and eligible immediately

- - Joe's pension benefit may decrease during his early 60's due to life expectancy.

- - (Misconception: When you hit 30 years of service pension benefit decreases)

- - Early retirement discounts & penalties may apply, refer to table A & B (penalties below)

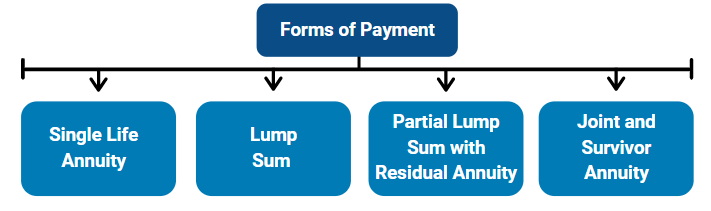

Pension Payment Options

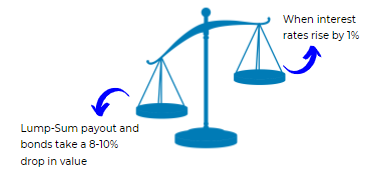

Interest Rates and Life Expectancy

AT&T's pension plan offers a choice between a lump-sum payout or a monthly pension. Plans may offer a lump sum option as a way to reduce their long-term liabilities — which can be beneficial to you, if interest rates are favorable at the time of retirement.

Generally, lower interest rates result in higher lump sum payouts, while rising interest rates can reduce the payouts.

As you approach retirement, monitor interest rates closely. A low-rate environment can increase the initial value of a lump sum, while a higher-rate environment can reduce it.

Additionally, life expectancy plays an important role. Younger retirees or those with longer life expectancies may find the annuity more attractive for its lifetime income guarantee — because they predict that they'll have more life to live. Those with shorter life expectancies, and those who want the potential to leave a lasting legacy to their families, might prefer the flexibility and benefits of a lump sum.

Timing Considerations

For AT&T employees nearing retirement, timing your pension payout can make a difference. AT&T allows employees to defer pension collection to a later date, which may be advantageous to you if you anticipate lower interest rates in the future. For example, if rates are expected to be lower in 2030 and you're planning to retire in 2029, deferring your pension to 2030 could help maximize your lump sum. According to AT&T’s Summary Plan Description, “If you do not wish to immediately elect to receive your Pension Benefit, you may elect to start receiving your Pension Benefit as of the first (1st) day of any month following your Termination of Employment and before reaching your Normal Retirement Age.”

Regularly calculating your pension options based on project interest rates, life expectancy, and personal needs for survivor benefits and tax planning will allow you to make the most of your AT&T retirement benefits. If you need a helpful advisor who's been through the process before, reach out for an introductory meeting today.

Taking strategic distributions from retirement accounts

Your retirement assets likely comprise a complex array several retirement accounts, IRAs, 401(k)s, taxable accounts, and others. What is the most efficient way to take your retirement income?

You may want to consider meeting your income needs in retirement by first drawing down taxable accounts rather than tax-deferred accounts. By taking retirement distributions from taxable accounts first, you'll allow the investments in tax-deferred accounts to grow further, maximizing tax-efficient growth.

However, keep in mind that you'll need to take required minimum distributions (RMDs) from any employer-sponsored retirement plans and traditional or rollover IRA accounts due to IRS requirements. If you don't take your RMDs at age 73, the IRS may assess a stiff penalty on the amount you should have withdrawn.

Two flexible distribution options for your IRA

When you need to draw on your IRA for income or take your RMDs, you have a few choices. Regardless of what you choose, IRA distributions are subject to income taxes and may be subject to penalties and other conditions if you’re under 59½.

- Partial withdrawals: Withdraw any amount from your IRA at any time. If you’re 73 or over, you’ll have to take at least enough from one or more IRAs to meet your annual RMD.

- Systematic withdrawal plans: Structure regular, automatic withdrawals from your IRA by choosing the amount and frequency to meet your retirement income needs. If you’re under 59½, you may be subject to a 10% early withdrawal penalty (unless your withdrawal plan meets Code Section 72(t) rules).

Your financial advisor can help you understand distribution options, determine RMD requirements, calculate RMDs, and set up a systematic withdrawal plan.

Don't have a financial advisor yet, or looking for a fresh start? Reach out to The Retirement Group and set up an appointment with one of our AT&T-focused advisors today.

Example: Net Unrealized Appreciation (NUA) Tax Savings

The 401(k) benefits of working with a financial advisor

When faced with a problem or challenge, many of us are programmed to try to figure it out on our own rather than ask for help. But with 401(k) investing, choosing to go it alone rather than get help can significantly impact your outcomes, especially as you approach your 60s. That's why it's important to work with an advisor experienced with AT&T retirement benefits. According to a study from Charles Schwab, the annual performance gap between those who get help and those who do not is 3.32% net of fees. This means a 45-year-old participant could see a 79% boost in wealth by age 65 simply by contacting an advisor. That’s a big difference.

If you're looking for guidance from an advisor who's been through it before, reach out to a The Retirement Group advisor today. Remember, the benefits of getting help go beyond convenience.

Strategies to leverage your 401(k) before retirement

Did you know that there are ways you can tap into and leverage your 401(k) funds before retirement? Although these strategies may not apply to every situation, you may be able to use your 401(k) to bridge certain gaps in your financial plan.

Strategy #1. In-service withdrawals and 401(k) rollovers

An in-service withdrawal is when an employee takes money from their 401(k) while they're still employed. In-service withdrawals are a way that you can access money from your 401(k) early, and potentially roll it over into a different account type:

- Eligibility. In-service withdrawals are generally available to employees after they reach age 59 and a half, so they avoid the 10% early withdrawal penalty. However, some plans allow for earlier access to 401(k) funds under circumstances such as financial hardship.

- IRA rollover. These withdrawals are often used to roll over funds into an IRA or another retirement account while you're still employed. A direct rollover can avoid the 10% early withdrawal penalty, as well as any mandatory tax withholding. Rolling over your 401(k) into an IRA is a popular option for those looking for more control over their retirement savings. While your 401(k) might limit investment choices, IRAs can offer a broader range of investments.

- Tax implications. If your in-service withdrawal is not rolled over into an IRA, you may face income tax on the amount withdrawn.

It’s important to know that certain withdrawals are subject to regular federal income tax and you may also be subject to an additional 10% penalty tax depending on your age. You can determine if you’re eligible for a withdrawal, and request one, online or by calling your AT&T Benefits Center in the United States. Your plan summary outlines more information and possible restrictions on rollovers and withdrawals. You should also know that the plan administrator reserves the right to modify the rules regarding withdrawals at any time, and may further restrict or limit the availability of withdrawals for administrative or other reasons. All plan participants will be advised of any such restrictions, and they apply equally to all employees at AT&T.

However, you may not be making an in-service withdrawal to roll over your 401(k). If you need the money now, you may be withdrawing because you think you have no better option.

Taking a withdrawal permanently reduces your retirement savings and can be subject to tax. As such, you could consider taking a loan from your 401(k) to meet pressing financial needs, rather than a withdrawal.

Strategy #2. Taking a loan from your 401(k)

If you need money quickly, such as if you lose your job, face a serious health emergency, or need a lot of cash for some other reason, borrowing from your 401(k) can be an option. Banks will make you jump through many hoops for a personal loan, and credit cards charge too much interest... suddenly, your 401(k) balance might start looking like a usable asset.

Unlike an in-service withdrawal, a loan must be paid back. However, they are not taxable (unless you fail to repay them).

While taking a loan from your 401(k) may seem like a quick solution, it's important to consider the potential implications.

- Borrowing from the future. First and foremost, you may be setting your retirement plan back by a some time if you take money from your future and use it today.

- Lost growth potential. Even though you'll repay the loan, those funds will miss out on potential growth through investments during the repayment period. This can create a gap in your portfolio, especially if the market performs well while your money is out of the account.

- Repayment issues. If you leave your employer or lose your job, you may be forced to pay thee full loan within a short time frame. If you're unable to, the loan can be treated as an early withdrawal — and be penalized and taxed as such.

Borrowing from your 401(k) should be considered a last resort. If you're concerned that you may need to take a loan from your 401(k) to make ends meet, reach out to a The Retirement Group advisor today. We can help you integrate your loan into your holistic financial plan.

AT&T Beneficiary Designations

When you're retirement and estate planning, it's important to remember to name someone to receive the proceeds of your benefits programs in the event of your death. These designations, known as "beneficiary designations", are how AT&T will know whom to send your final compensation and benefits to.

Simply stating in your will how you want the money in a retirement account to be distributed is not enough. You must have an up-to-date beneficiary designation to make sure your assets go where you intended.

Beyond just retirement accounts, beneficiary designations are used for life insurance payouts, pension, and even some bank or savings accounts.

Next steps:

- When you retire, make sure that you update your beneficiaries. AT&T has an Online Beneficiary Designation form for life events such as death, marriage, divorce, child birth, adoptions, and more.

- If you are unsure about how to align your AT&T beneficiary designations with your overall financial plan, schedule a call to speak with one of our AT&T-focused advisors.

Claiming Social Security is one thing — understanding the "why" behind your claim is something else entirely. Understanding Social Security is a difficult but crucial step towards your retirement paycheck. For many Americans, Social Security benefits are core to their retirement income strategy. However, when and why you claim them depends on your overall withdrawal strategy.

Next, let's explore three main steps you should follow to solidify your Social Security strategy at AT&T:

Step 1. Decide when to claim your Social Security benefits.

Social Security benefits can be significant, but at the end of the day, they're just one part of your overall financial picture. When considering the timing of your claim, keep this general principle in mind: The later you begin receiving benefits, the larger those benefits will be.

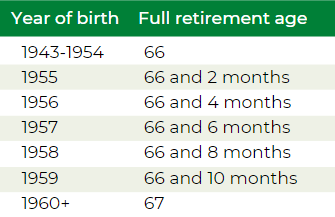

The full monthly Social Security retirement benefit is based on applying at the Full Retirement Age (FRA), which is age 67 for those born 1960 or later. For every year you wait after you reach the FRA, your benefit amount increases 8%. It reaches a maximum at age 70. If we do the math, we can determine that, if you start claiming at age 70, your monthly benefit will be 124% the full benefit.

However, you can also apply before you reach FRA, as early as age 62. You will receive a reduced benefit if you do so, but this option could make sense for those who want to start claiming their benefit earlier for longevity reasons.

Step 2. Understand the tax implications.

For all but the lowest income retirees, Social Security benefits are actually taxable. Only individuals with provisional income under $25,000, or $32,000 if married filing jointly, receive their benefits tax-free. Otherwise, up to 85% of your benefits will be treated as taxable income.

Furthermore, depending on where you live, your Social Security benefits may even be taxed at the state level. If you plan to move for retirement, the tax regime in the state you're moving to can be a relevant consideration.

Step 3. Start preparing today.

Even if your retirement is right around the corner, you can make decisions today that will impact you for years, or decades, to come. For instance, delaying your Social Security claiming date even a year or two can snowball into a significant benefit. To bridge the gap between their retirement date and their claiming date, some people create a "slush fund" while they're working to take the place of the Social Security benefits they would receive from claiming at FRA. Whether these funds come from a 401(k), IRA, or brokerage account, integrating a bit of extra padding in your planning can pay off in the long run.

Always remember, your Social Security benefit is just one part of your overall financial picture. And when you start to consider tax implications, withdrawal sequencing, and effective diversification (beyond just the asset class), the picture can start to get complicated. That's what we're here to help with. At The Retirement Group, we've been assisting AT&T employees to and through retirement for years. If you're interested in speaking with an experienced advisor who's been through the process before, reach out today.

AT&T Medicare Coverage for Retirees

Are you eligible for Medicare or will be soon? If you or your dependents are eligible after you leave AT&T, Medicare generally becomes the primary coverage for you or any of your dependents as soon as they are eligible for Medicare. This will affect your company-provided medical benefits.

It's your responsibility to enroll in Medicare Parts A and B when you first become eligible — and you must stay enrolled to have coverage for Medicare-eligible expenses. This applies to your Medicare-eligible dependents as well.

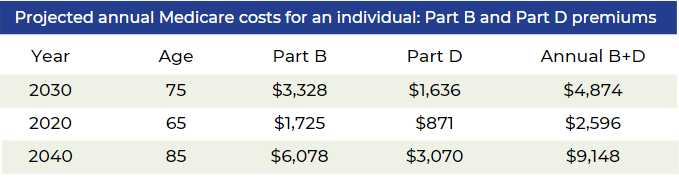

The Reality of Medical Costs in Retirement

Divorce and Retirement Benefits Explained

Social Security Benefits. Divorce can significantly impact retirement benefits, including Social Security. Understanding how divorce affects Social Security is essential for retirement planning, especially if you were married for a substantial period. In some cases, divorced individuals may be eligible to claim benefits based on their former spouse's work record.

You can apply for a divorced spouse’s benefit if the following criteria are met:

- You’re at least 62 years of age.

- You were married for at least 10 years prior to the divorce.

- You are currently unmarried.

- Your ex-spouse is entitled to Social Security benefits.

- Your own Social Security benefit amount is less than your spousal benefit amount, which is equal to one-half of what your ex’s full benefit amount would be if claimed at Full Retirement Age (FRA).

Unlike a married couple, your ex-spouse doesn’t have to have filed for Social Security before you can apply for your divorced spouse’s benefit. However, this caveat only applies if you’ve been divorced for at least two years, and your ex is at least 62 years of age. If the divorce was less than two years ago, your ex must already be receiving benefits before you can file as a divorced spouse.

Social Security Survivor Benefits. Many people are surprised that divorce doesn't disqualify you from receiving survivor benefits if your spouse dies. You can claim a divorced spouse's survivor benefit if the following conditions are met:

- Your ex-spouse is deceased.

- You are at least 60 years old.

- You were married for at least 10 years.

- You are single, or you remarried after age 60.

If you qualify for survivor benefits and your own Social Security benefits, you can choose to start with survivor benefits and switch to your own later, or vice versa, depending on which option gives you the highest payout over time. If this pertains to you, we recommend speaking to a qualified financial advisor — because planning your Social Security strategy in advance is critical to maximizing your outcomes.

Your AT&T Pension and Divorce

If you're getting a divorce near or in retirement, there are a number of steps you must take before starting your AT&T pension. For each former spouse who may have an interest in your pension benefit, you'll need to provide AT&T with the following documentation:

- A copy of the court-filed Judgment of Dissolution or Judgment of Divorce along with any Marital Settlement Agreement (MSA)

- A copy of the court-filed Qualified Domestic Relations Order (QDRO)

You must provide AT&T with any requested documentation to avoid having your pension benefit delayed or suspended. To find out more information on strategies if divorce is affecting your retirement benefits, please give us a call.

Note: You’ll need to submit this documentation to your company’s online pension center regardless of how old the divorce or how short the marriage.

Are you in the process of divorcing close to retirement?

If your divorce isn’t final before your retirement date, you’re still considered married. You have two options regarding your AT&T pension:

- Retire before your divorce is final and elect a joint pension of at least 50% with your spouse — or get your spouse’s signed, notarized consent to a different election or lump sum.

- Delay your retirement until after your divorce is final and you can provide the required divorce documentation.

7.png)