People in the United States need to be aware of changes made by both Bank of America and the IRS, especially as they approach their 50s and 60s. Although the world seems to become more volatile and uncertain each day, there are a few key constants can help you keep your retirement plan on track—no matter where you're starting from. Here are some important updates for 2025:

Tax Code Changes 2025

- Standard deduction. In 2025, the standard deduction increased to $15,000 for single filers and married filing separately, $30,000 for joint filers, and $22,500 for heads of household.

- Additional deduction. Taxpayers who are over the age of 65 or blind can add an additional $1,600 to their standard deduction. This amount jumps to $2,000 if they are also unmarried or not a surviving spouse.

- Cash contributions to charity. The special deduction that allowed non-itemizers to deduct up to $300 in cash donations to charity—or $600 for those married filing jointly—has expired.

Note: Remote workers employed by Bank of America could face double taxation on state taxes. Thanks to the advent of remote work during the COVID-19 pandemic, many employees moved away from core cities. Notably, these movements could have taken them outside the state where they were employed. Some states established temporary relief provisions to avoid double taxation of income, but many of those provisions may have expired. There are only six states that currently have a "special convenience of employer" rule: Connecticut, Delaware, Nebraska, New Jersey, New York, and Pennsylvania. If you work remotely for Bank of America, and if you don't currently reside in those states, consult with your tax advisor to determine if there are other ways to mitigate the potential for double taxation.

Child Tax Credit Updates for 2025

Bank of America employees interested in reducing their tax burdens as much as possible may benefit from the Child Tax Credit. Although it only applies to individuals with children under the age of 18, it can be relevant to those who are approaching retirement if they have minor children—or if their children have children!

Here are the 2025 updates:

- Maximum credit per qualifying child: $2,000 for children aged five and under; $3,000 for children aged six through 17.

- Child Tax Credit eligibility. As a parent or guardian, you are eligible for the Child Tax Credit if your adjusted gross income is less than $200,000, or $400,000 if married filing jointly.

- Partial refundability. If your Child Tax Credit is greater than your tax, you can receive up to $1,600 as a cash refund.

Optimize your retirement contributions

Contributing to Bank of America's 401k plan can cut this year's tax bill significantly. With the right planning, these benefits can be compounded over time. In 2025, the amount you can save increased:

- 2025 limit. Individuals can contribute $23,500 to their 401k plans in 2025.

- Catch-up contributions. Employees age 50 and over can contribute an extra $7,500, bringing their total limit to $31,000. For those who turn 60 - 63 years of age during calendar year 2025, their catch up contribution is $11,250, for a combined total of $34,750.

- A major opportunity. Lowering your taxable income by up to $34,750 means less of your money is immediately taxed. As shown in the table below, this could save you thousands on your current tax bill.

Many investors choose to invest the money they save in taxes for the year. This bonus nest egg then has the opportunity to grow in the market, which can help pay the deferred tax when they make withdrawals from their accounts later in life.

Dealing with Inflation

Inflation—we're all too familiar with it. Inflation degrades purchasing power over time, meaning the same things cost more year after year. While inflation is difficult to deal with as a working adult, managing it becomes harder in retirement.

To maintain the same standard of living in retirement, you need to factor rising costs into your plan. While the Federal Reserve targets 2% inflation each year, the scorching inflation of the early 2020s reminded us that Fed targets are anything but a guarantee.

When nearing retirement, it's important to keep track of the rate of inflation, especially in specific areas like health care. While prices as a whole have risen dramatically, increases in particular categories can outpace inflation, which can lead to unpleasant surprises down the road if you're not prepared. Speak with a qualified financial advisor when constructing your holistic plan to help plan for the impacts of future inflation.

*Source: IRS.gov, Yahoo, Bankrate, Forbes

Blogs You May Enjoy:

![]()

Source: Is it Worth the Money to Hire a Financial Advisor?, the balance, 202

Starting to save as early as possible matters. Time on your side means compounding can have significant impacts on your future savings. And, once you’ve started, continuing to increase and maximize your contributions for your 401k plan is key.

Getting help with your 401k

Over half of plan participants in the United States admit they don’t have the time, interest, or knowledge needed to manage their 401k portfolio. But the benefits of getting help go beyond convenience.

A Charles Schwab study found several positive outcomes common to those using independent professional advice. They include:

- Improved savings rates – 70% of participants who obtained 401k advice increased their contributions.

- Increased diversification – Participants who managed their own portfolios invested in an average of just under four asset classes, while participants in advice-based portfolios invested in a minimum of eight asset classes.

- Increased likelihood of staying the course – Getting advice raised the odds of participants staying true to their investment objectives, making them less reactive during volatile market conditions and more likely to remain in their original 401k investments during a downturn.

Don't try to do it alone. Get help with your company's 401k plan investments. Your nest egg will thank you.

Net Unrealized Appreciation (NUA)

When you qualify for a distribution from your 401k plan, you have three options:

- Roll-over your qualified plan to an IRA and continue deferring taxes.

- Take a distribution and pay ordinary income tax on the full amount.

- Take advantage of NUA and reap the benefits of a more favorable tax structure on gains.

How does Net Unrealized Appreciation work?

NUA is a strategy to help mitigate taxes on the gains you may have realized from owning company stock.

To use this strategy, you must first be eligible for a distribution from your qualified company-sponsored plan, which typically happens at retirement or age 59 1⁄2. Generally, you would take a 'lump-sum' distribution from the plan, distributing all assets from the plan during a one-year period. The portion of the plan that is made up of mutual funds and other investments can be rolled into an IRA for further tax deferral. The highly appreciated company stock is then transferred to a non-retirement account.

The tax benefit comes when you transfer the company stock from a tax-deferred account to a taxable account. At this time, you apply NUA and you incur an ordinary income tax liability on only the cost basis of your stock. The appreciated value of the stock above its basis is not taxed at the higher ordinary income tax rate but at the lower long-term capital gains rate, currently 15%. This could mean a potential savings of over 30%.

As a Bank of America employee, you may be interested in understanding NUA from a financial advisor. Reach out today to schedule a complimentary meeting.

IRA Withdrawal

Your retirement assets may be spread across several retirement accounts: IRAs, 401ks, taxable accounts, and others.

So, what is the most efficient way to take your retirement income after leaving Bank of America?

This question relates to something called withdrawal sequencing, and it's a problem we're well-equipped to handle at The Retirement Group.

You may want to consider meeting your income needs in retirement by first drawing down taxable accounts rather than tax-deferred accounts. This may help your company-sponsored retirement assets last longer as they continue to potentially grow tax deferred.

You will also need to plan to take the required minimum distributions (RMDs) from any company-sponsored retirement plans and traditional or rollover IRA accounts when you reach age 73.

Two flexible distribution options for your IRA

When you need to draw on your IRA for income or to take your RMDs, you have a few choices. Regardless of what you choose, IRA distributions are subject to income taxes and may be subject to penalties and other conditions if you’re under 59½.

Option 1. Partial withdrawals: Withdraw any amount from your IRA at any time. If you’re 73 or over, you’ll have to take at least enough from one or more IRAs to meet your annual RMD.

Option 2. Systematic withdrawal plans: Structure regular, automatic withdrawals from your IRA by choosing the amount and frequency to meet your income needs after retiring from Bank of America. If you’re under 59½, you may be subject to a 10% early withdrawal penalty (unless your withdrawal plan meets Code Section 72(t) rules).

Your tax advisor can help you understand distribution options, determine RMD requirements, calculate RMDs, and set up a systematic withdrawal plan.

To help you make an informed decision, let's explore three main steps you should follow to solidify your Social Security strategy:

Step 1. Decide when to claim your Social Security benefits

Social Security benefits can be significant, but at the end of the day, they're just one part of your overall financial picture. When considering the timing of your claim, keep this general principle in mind: The later you begin receiving benefits, the larger those benefits will be.

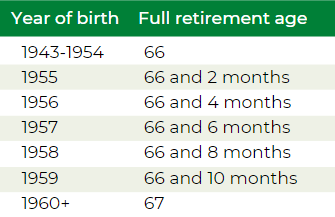

The full monthly Social Security retirement benefit is based on applying at the Full Retirement Age (FRA), which is age 67 for those born 1960 or later. For every year you wait after you reach the FRA, your benefit amount increases 8%. It reaches a maximum at age 70. If we do the math, we can determine that, if you start claiming at age 70, your monthly benefit will be 124% the full benefit.

However, you can also apply before you reach FRA, as early as age 62. You will receive a reduced benefit if you do so, but this option could make sense for those who want to start claiming their benefit earlier for longevity reasons.

Step 2. Understand the tax implications

For all but the lowest-income retirees, Social Security benefits are actually taxable. Only individuals with provisional income under $25,000, or $32,000 if married filing jointly, receive their benefits tax-free. Otherwise, up to 85% of your benefits will be treated as taxable income.

Furthermore, depending on where you live, your Social Security benefits may even be taxed at the state level. If you plan to move for retirement, the tax regime in the state you're moving to can be a relevant consideration.

Step 3. Start preparing today

Even if your retirement is right around the corner, you can make decisions today that will impact you for years, or decades, to come. For instance, delaying your Social Security claiming date even a year or two can snowball into a significant benefit. To bridge the gap between their retirement date and their claiming date, some people create a "slush fund" while they're working to take the place of the Social Security benefits they would receive from claiming at FRA. Whether these funds come from a 401k, IRA, or brokerage account, integrating a bit of extra padding in your planning can pay off in the long run.

Always remember, your Social Security benefit is just one part of your overall financial picture. And when you start to consider tax implications, withdrawal sequencing, and effective diversification (beyond just the asset class), the picture can start to get complicated. That's what we're here to help with. At The Retirement Group, we've been assisting Bank of America employees to and through retirement for years. If you're interested in speaking with an experienced advisor who's been through the process before,reach out today.

Medicare Coverage for Retirees

Are you eligible for Medicare or will be soon? If you or your dependents are eligible after you leave Bank of America, Medicare generally becomes the primary coverage for you or any of your dependents as soon as they are eligible for Medicare. This will affect your company-provided medical benefits.

It's your responsibility to enroll in Medicare Parts A and B when you first become eligible—and you must stay enrolled to have coverage for Medicare-eligible expenses. This applies to your Medicare-eligible dependents as well.

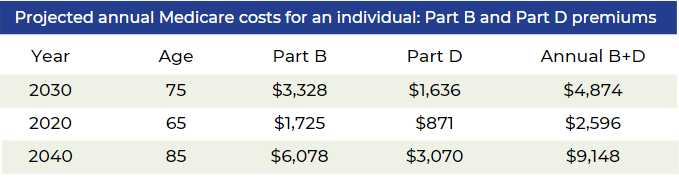

The Reality of Medical Costs in Retirement