Blogs You May Enjoy:

![]()

Source: Is it Worth the Money to Hire a Financial Advisor? The Balance

Starting to save as early as possible matters. Time on your side means compounding can have significant impacts on your future savings. And, once you’ve started, continuing to increase and maximize your contributions for your 401k plan is key.

Lump Sum vs. Annuity

Boeing employees in your city, your state who are eligible for a pension are often given the choice to either receive pension payments for life or take a lump sum dollar amount up front for the "equivalent" value of the pension. The idea for those who choose a lump sum is that you could take the money, roll it over to an individual retirement account (IRA), invest it, and generate your own cash flows that enable you to take systematic withdrawals following your retirement from Boeing.

On the plus side, a lump sum payment gives you complete flexibility over the funds, potentially allowing you to generate a greater retirement cash flow than you would receive with an annuity. Additionally, if something happens to you, any unused account balance will be available to a surviving spouse or heirs. However, if you fail to invest the funds for sufficient growth, there’s a danger that the money could run out during your lifetime - and you may regret not having held onto the pension’s “income for life” guarantee.

For its part, a pension annuity provides you with a steady stream of income guaranteed to continue for life, as long as the pension plan itself remains solvent and doesn’t default. So whether you live 10, 20, 30, or more years after leaving Boeing, you don’t have to worry about the risk of outliving your money.

However, taking an annuity also comes with some drawbacks. Once you annuitize your pension, you can no longer access the lump sum. Additionally, unlike Social Security benefits, not all company pensions contain a cost of living allowance (COLA). That means the dollar amount of your monthly pension will remain the same throughout your retirement, losing its purchasing power in the face of inflation.

Ultimately, your decision will depend on what return must be generated on that lump sum to replicate the payments of the annuity. After all, if a return of only 1% to 2% on your lump sum can create the same lifetime cash flows you'd see with an annuity, you're at less risk of outliving the lump sum after leaving Boeing, even if you withdraw from it for life. However, if the annuity payments can only be matched by earning a much higher and possibly riskier rate of return, there is a greater risk those returns won’t manifest and you could run out of money.

Interest Rates and Life Expectancy

Current interest rates, as well as your life expectancy at retirement, have a significant impact on lump sum payouts of defined benefit pension plans.

Rising interest rates have an inverse relationship to pension lump sum values. All else being equal, a higher interest rate will consequently produce a lower lump sum. The reverse is also true: decreasing or lower interest rates will increase pension lump sum values. This makes interest rates an important consideration when deciding between a lump sum or annuity payout from your pension plan.

Given the current complex interest rate environment, we strongly suggest discussing your options with The Retirement Group. We monitor rates on a daily basis and keep you updated on the monthly changes. We can also provide a complimentary Cash Flow Analysis to show you how various retirement dates may play out.

By knowing where you stand, you can make a more prudent decision regarding the optimal time to retire, and which pension distribution option best meets your needs.

Over half of plan participants in your city, your state admit they don’t have the time, interest, or knowledge needed to manage their 401k portfolio. But the benefits of getting help go beyond convenience.

A Charles Schwab study found several positive outcomes common to those using independent professional advice. They include:

- Improved savings rates – 70% of participants who obtained 401k advice increased their contributions.

- Increased diversification – Participants who managed their own portfolios invested in an average of just under four asset classes, while participants in advice-based portfolios invested in a minimum of eight asset classes.

- Increased likelihood of staying the course – Getting advice raised the odds of participants staying true to their investment objectives, making them less reactive during volatile market conditions and more likely to remain in their original 401k investments during a downturn.

Don't try to do it alone. Get help with your Boeing 401k plan investments. Your nest egg will thank you.

Net Unrealized Appreciation (NUA)

When you qualify for a distribution from your 401k plan, you have three options:

- Roll-over your qualified plan to an IRA and continue deferring taxes.

- Take a distribution and pay ordinary income tax on the full amount.

- Take advantage of NUA and reap the benefits of a more favorable tax structure on gains.

How does Net Unrealized Appreciation work?

First, you must be eligible for a distribution from your qualified company-sponsored plan, which typically happens at retirement age. Generally, you would take a lump sum distribution from the plan, distributing all assets from the plan during a one-year period. The portion of the plan that is made up of mutual funds and other investments can be rolled into an IRA for further tax deferral. The highly appreciated company stock is then transferred to a non-retirement account.

The tax benefit comes when you transfer the company stock from a tax-deferred account to a taxable account. At this time, you apply NUA and you incur an ordinary income tax liability on only the cost basis of your stock. The appreciated value of the stock above its basis is not taxed at the higher ordinary income tax but at the lower long-term capital gains rate, currently 15%. This could mean a potential savings of over 30%.

You may be interested in learning more about NUA with a complimentary one-on-one session with a financial advisor from The Retirement Group.

IRA Withdrawal

Your retirement assets may be spread across several retirement accounts: IRAs, 401ks, taxable accounts, and others.

So, what is the most efficient way to take your retirement income after leaving Boeing?

This question relates to something called withdrawal sequencing, and it's a problem we're well-equipped to handle at The Retirement Group.

You may want to consider meeting your income needs in retirement by first drawing down taxable accounts rather than tax-deferred accounts. This may help your retirement assets with your company last longer as they continue to potentially grow tax deferred.

You will also need to plan to take the required minimum distributions (RMDs) from any company-sponsored retirement plans and traditional or rollover IRA accounts when you reach age 73.

Two flexible distribution options for your IRA

When you need to draw on your IRA for income or to take your RMDs, you have a few choices. Regardless of what you choose, IRA distributions are subject to income taxes and may be subject to penalties and other conditions if you’re under 59½.

Option 1: Partial withdrawals: Withdraw any amount from your IRA at any time. If you’re 73 or over, you’ll have to take at least enough from one or more IRAs to meet your annual RMD.

Option 2: Systematic withdrawal plans: Structure regular, automatic withdrawals from your IRA by choosing the amount and frequency to meet your income needs after retiring from Boeing. If you’re under 59½, you may be subject to a 10% early withdrawal penalty (unless your withdrawal plan meets Code Section 72(t) rules).

Your tax advisor can help you understand distribution options, determine RMD requirements, calculate RMDs, and set up a systematic withdrawal plan.

Claiming Social Security is one thing; understanding how your claim works is something else entirely. Understanding Social Security is a difficult but crucial step in assessing your retirement paycheck. For many Americans, Social Security benefits are core to their retirement income strategy. However, when and why you claim them depends on your overall withdrawal strategy.

To help you make an informed decision, let's explore three main steps you should follow to solidify your Social Security strategy at Boeing:

Step 1. Decide when to claim your Social Security benefits

Social Security benefits can be significant, but at the end of the day, they're just one part of your overall financial picture. When considering the timing of your claim, keep this general principle in mind: The later you begin receiving benefits, the larger those benefits will be.

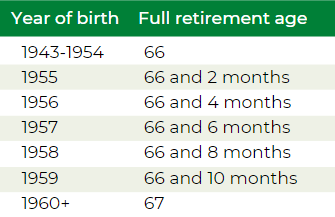

The full monthly Social Security retirement benefit is based on applying at the Full Retirement Age (FRA), which is age 67 for those born 1960 or later. For every year you wait after you reach the FRA, your benefit amount increases 8%. It reaches a maximum at age 70. If we do the math, we can determine that, if you start claiming at age 70, your monthly benefit will be 124% the full benefit.

However, you can also apply before you reach FRA, as early as age 62. You will receive a reduced benefit if you do so, but this option could make sense for those who want to start claiming their benefit earlier for longevity reasons.

Step 2. Understand the tax implications

For all but the lowest-income retirees, Social Security benefits are actually taxable. Only individuals with provisional income under $25,000, or $32,000 if married filing jointly, receive their benefits tax-free. Otherwise, up to 85% of your benefits will be treated as taxable income.

Furthermore, depending on where you live, your Social Security benefits may even be taxed at the state level. If you plan to move for retirement, the tax regime in the state you're moving to can be a relevant consideration.

Step 3. Start preparing today

Even if your retirement is right around the corner, you can make decisions today that will impact you for years, or decades, to come. For instance, delaying your Social Security claiming date even a year or two can snowball into a significant benefit. To bridge the gap between their retirement date and their claiming date, some people create a "slush fund" while they're working to take the place of the Social Security benefits they would receive from claiming at FRA. Whether these funds come from a 401k, IRA, or brokerage account, integrating a bit of extra padding in your planning can pay off in the long run.

Always remember, your Social Security benefit is just one part of your overall financial picture. And when you start to consider tax implications, withdrawal sequencing, and effective diversification (beyond just the asset class), the picture can start to get complicated. That's what we're here to help with. At The Retirement Group, we've been assisting Boeing employees to and through retirement for years. If you're interested in speaking with an experienced advisor who's been through the process before, reach out today.

Medicare Coverage for Retirees

Are you eligible for Medicare or will be soon? If you or your dependents are eligible after you leave Boeing, Medicare generally becomes the primary coverage for you or any of your dependents as soon as they are eligible for Medicare. This will affect your company-provided medical benefits.

It's your responsibility to enroll in Medicare Parts A and B when you first become eligible, and you must stay enrolled to have coverage for Medicare-eligible expenses. This applies to your Medicare-eligible dependents as well.

6.png)