2026 Tax Changes & Inflation

Blogs You May Enjoy:

![]()

Source: Is it Worth the Money to Hire a Financial Advisor?, The Balance

Starting to save as early as possible matters. Time on your side means compounding can have significant impacts on your future savings. And, once you’ve started, continuing to increase and maximize your contributions for your 401(k) plan is key.

- Perhaps your company is among those following a similar model to Shell, where the company determines the contribution percentage by looking at specific factors related to each employee.

- In the Shell Retirement Plan, the company's annual contribution is tier based, with higher contributions coming once an employee has passed a years of service threshold.

- In the Shell Retirement Plan, the company's annual contribution is tier based, with higher contributions coming once an employee has passed a years of service threshold.

| After Completing... | Company Contribution |

| 1 year of accredited service | 2.5% |

| 6 years of accredited service | 5% |

| 9 years of accredited service | 10% |

- On the other hand, it's possible that your company determines its contribution based on a combination of specific factors, like ExxonMobil.

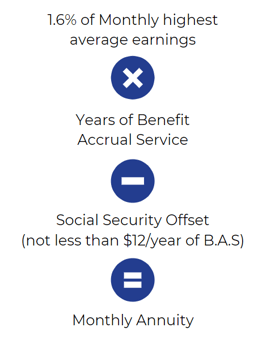

- ExxonMobil's basic pension benefit is determined by:

- Final Average Pensionable Pay x Years of Service x 1.6% = Final Average Pensionable Pay subtotal

- Primary Social Security x Years of Service x 1.5% = Social Security offset

- Final Average Pensionable Pay subtotal - Social Security offset = Basic Pension Monthly Benefit.

- ExxonMobil is just one of many companies using a Social Security offset when calculating Pension Benefits. Various energy companies calculate the offset formula differently, which is why it's important to contact and advisor who knows your specific plan sponsored by your company.

- ExxonMobil's basic pension benefit is determined by:

The applicable interest rate is a separate average of each of the three segment rates for the fifth, fourth and third months preceding your annuity start date. The three segment rates are calculated by the IRS according to regulations that are also part of the Pension Protection Act of 2006 and reflect the yields of short-, mid-, and long-term corporate bonds. (Note: Chevron also has Legacy Unocal and Legacy Texaco Retirement Plans)

AT&T non-management employees have their own Hourly/non-management pension plan. Let's take a look at a pension example for a gentleman by the name of Joe Smith who is hourly and using the Hourly/non-management pension plan.

In 1990, Joe is hired by AT&T and participates in the Hourly Pension Plan:

-

Hourly has a defined benefit plan that uses pension bands.

-

A pension band determines your benefits based on your job title/grade level/occupation.

-

Joe will receive a monthly dollar amount into his account for each year of service.

-

Joe's benefit (pension band may change yearly).

-

-

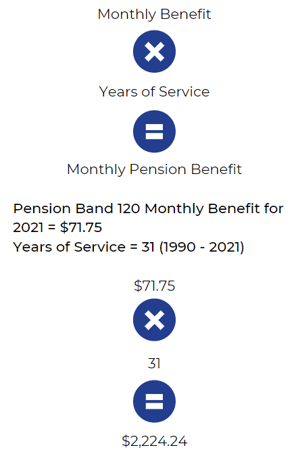

Hourly Pension Example

Let's assume Joe is working as a Cable Splicing Technician and is in Pension Band 120. Joe is retiring in 2021 and wants to calculate his Hourly Pension benefit.

While this formula calculates a monthly pension benefit, you can determine the lump sum equivalent by using the annuity to lump sum conversion table on Fidelity's website.

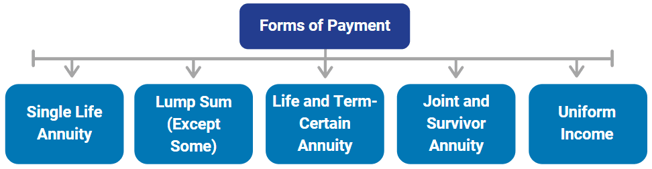

If a Pension is offered, your company's retirement plan will generally allow for different forms of payment:

Single Life Annuity

- The monthly Single Life Annuity is the benefit from which all of the optional forms of payment under the plan are derived.

- Pays a fixed amount each month for retiree’s lifetime.

- A death benefit may be payable to your beneficiary.

- A death benefit is payable if vested and the employee dies before employment with their company.

Lump-Sum Option (Most Oil Companies Offer a Lump Sum)

- Lump-sum payment is actuarially equivalent to the total annuity you would have received as a Single Life Annuity during your lifetime.

- Calculated using actuarial factors based on your age and the interest rate in effect on your annuity starting date.

- No death benefits are payable.

NOTE: Lump-Sum vs. Annuity - With decreasing interest rates, your lump-sum payout will increase.

Life & Term-Certain Annuity Option

- Smaller than the Single Life Annuity.

- 5, 10, or 15 year period certain.

- If you have multiple beneficiaries or if your beneficiary is your estate or trust, remaining payments converted actuarially to a lump-sum.

- No death benefits are payable.

Check out this article by our partner company The Wealth Enhancement Group to learn more about estate planning and trusts:

5 Essential Documents for Crafting a Good Estate Plan

4 Common Types of Spousal Trusts

Looking for a second opinion about your retirement from your company? Click here to speak to financial advisor today or call (800) 200-9838.

Joint & Survivor Annuity

Upon your death, a percentage of your monthly benefit is paid to your joint annuitant for his or her lifetime

Reduction factors may apply depending on your company's policy.

Uniform Income

Receive same level of income before and after receiving Social Security benefits

The level of income may change at a certain age. For example, in the Chevron Uniform Income policy:

- Before age 62, employees receive a larger monthly annuity from the plan

- After age 62, when Social Security benefit is available, employees receive a smaller monthly annuity from the plan.

- Each company has varying rules in regards to Uniform Income. Review your company's SPD or talk to an advisor to find out the rules for your specific plan.

*These are examples and your company's plan may be different.

Lump-Sum vs. Annuity

Retirees who are eligible for a pension are often offered the choice of whether to actually take the pension payments for life, or receive a lump-sum dollar amount for the “equivalent” value of the pension – with the idea that you could then take the money (rolling it over to an IRA), invest it, and generate your own cash flows by taking systematic withdrawals throughout retirement from your company.

The upside of keeping the pension itself is that the payments are guaranteed to continue for life (at least to the extent that the pension plan itself remains in place and solvent and doesn’t default). Thus, whether you live 10, 20, or 30 (or more!) years after leaving your company, you don’t have to worry about the risk of outliving the money.

In contrast, selecting the lump-sum gives you the potential to invest, earn more growth, and potentially generate even greater retirement cash flow. Additionally, if something happens to you, any unused account balance will be available to a surviving spouse or heirs. However, if you fail to invest the funds for sufficient growth, there’s a danger that the money could run out altogether and you may regret not having held onto the pension’s “income for life” guarantee.

Ultimately, the “risk” assessment that should be done to determine whether or not you should take the lump sum or the guaranteed lifetime payments that your company pension offers depends on what kind of return must be generated on that lump-sum to replicate the payments of the annuity. After all, if it would only take a return of 1% to 2% on that lump-sum to create the same pension cash flows for a lifetime, there is little risk that you will outlive the lump-sum after leaving your company, even if you withdraw from it for life(10). However, if the pension payments can only be replaced with a higher and much riskier rate of return, there is, in turn, a greater risk those returns won’t manifest and you could run out of money.

Interest Rates and Life Expectancy

In many defined benefit plans, like the ExxonMobil pension plan, current and future retirees are offered a lump-sum payout or a monthly pension benefit. Sometimes these plans have billions of dollars worth of unfunded pension liabilities, and in order to get the liability off the books, your company may offer a lump-sum.

Depending on life expectancy, the initial lump-sum is typically less money than regular pension payments over a normal retirement time frame. However, most individuals that opt for the lump-sum plan to invest the majority of the proceeds, as most of the funds aren't needed immediately after retirement from your company.

Something else to keep in mind is that current interest rates, as well as your life expectancy at retirement, have an impact on lump-sum payout options of your company's defined benefit pension plans. Lump-sum payouts are typically higher in a low interest rate environment, but be careful because lump-sums decrease in a rising interest rate environment.

Additionally, projected pension lump-sum benefits for active corporate employees will often decrease as an employee ages and their life expectancy decreases. This can potentially be a detriment of continuing to work, so it is important that you run your pension numbers often and thoroughly understand the impact that timing has on your benefit. Other factors such as income needs, need for survivor benefits, and tax liabilities often dictate the decision to take the lump-sum over the annuity option on the pension.

Over half of plan participants admit they don’t have the time, interest or knowledge needed to manage their 401(k) portfolio. But the benefits of getting help goes beyond convenience. Studies like this one, from Charles Schwab, show those plan participants who get help with their investments tend to have portfolios that perform better: The annual performance gap between those who get help and those who do not is 3.32% net of fees. This means a 45-year-old participant could see a 79% boost in wealth by age 65 simply by contacting an advisor. That’s a pretty big difference.

Getting help can be the key to better results across the 401(k) board.

A Charles Schwab study found several positive outcomes common to those using independent professional advice. They include:

- Improved savings rates – 70% of participants who used 401(k) advice increased their contributions.

- Increased diversification – Participants who managed their own portfolios invested in an average of just under four asset classes, while participants in advice-based portfolios invested in a minimum of eight asset classes.

- Increased likelihood of staying the course – Getting advice increased the chances of participants staying true to their investment objectives, making them less reactive during volatile market conditions and more likely to remain in their original 401(k) investments during a downturn. Don’t try to do it alone.

Get help with your company's 401(k) plan investments. Your nest egg will thank you.

Net Unrealized Appreciation (NUA)

When you qualify for a distribution you have three options:

- Roll-over your qualified plan to an IRA and continue deferring taxes.

- Take a distribution and pay ordinary income tax on the full amount.

- Take advantage of NUA and reap the benefits of a more favorable tax structure on gains.

How does Net Unrealized Appreciation work?

First an employee must be eligible for a distribution from their qualified company-sponsored plan. Generally at retirement or age 59 1⁄2, the employee takes a 'lump-sum' distribution from the plan, distributing all assets from the plan during a 1 year period. The portion of the plan that is made up of mutual funds and other investments can be rolled into an IRA for further tax deferral. The highly appreciated company stock is then transferred to a non-retirement account.

The tax benefit comes when you transfer the company stock from a tax-deferred account to a taxable account. At this time you apply NUA and you incur an ordinary income tax liability on only the cost basis of your stock. The appreciated value of the stock above its basis is not taxed at the higher ordinary income tax but at the lower long-term capital gains rate, currently 15%. This could mean a potential savings of over 30%.

As a corporate employee, you may be interested in understanding NUA from a financial advisor.

IRA Withdrawal

When you qualify for a distribution you have three options:

Your retirement assets may consist of several retirement accounts: IRAs, 401(k)s, taxable accounts, and others.

So, what is the most efficient way to take your retirement income after leaving your company?

You may want to consider meeting your income needs in retirement by first drawing down taxable accounts rather than tax-deferred accounts.

This may help your retirement assets with your company last longer as they continue to potentially grow tax deferred.

You will also need to plan to take the required minimum distributions (RMDs) from any company-sponsored retirement plans and traditional or rollover IRA accounts.

Under current IRS rules, many account owners must begin taking required minimum distributions from these types of accounts at age 73. SECURE 2.0 reduced the excise tax for each under-distributed RMD dollar from 50% to 25%, with a further reduction possible when corrected timely.

There is new legislation that allows account owners to delay taking their first RMD until April 1 following the later of the calendar year they reach age 73 or, in a workplace retirement plan, retire.

Two flexible distribution options for your IRA

When you need to draw on your IRA for income or take your RMDs, you have a few choices. Regardless of what you choose, IRA distributions are subject to income taxes and may be subject to penalties and other conditions if you’re under 59½.

Partial withdrawals: Withdraw any amount from your IRA at any time. If you’re 73 or over, you’ll have to take at least enough from one or more IRAs to meet your annual RMD.

Systematic withdrawal plans: Structure regular, automatic withdrawals from your IRA by choosing the amount and frequency to meet your income needs after retiring from your company. If you’re under 59½, you may be subject to a 10% early withdrawal penalty (unless your withdrawal plan meets Code Section 72(t) rules).

Your tax advisor can help you understand distribution options, determine RMD requirements, calculate RMDs, and set up a systematic withdrawal plan.

You and your Medicare-eligible dependents must enroll in Medicare Parts A and B when you first become eligible. Medical and MH/SA benefits payable under the company's-sponsored plan will be reduced by the amounts Medicare Parts A and B would have paid whether you actually enroll in them or not.