Remote workers employed by ExxonMobil might face double taxation on state taxes. Here's what you need to know.

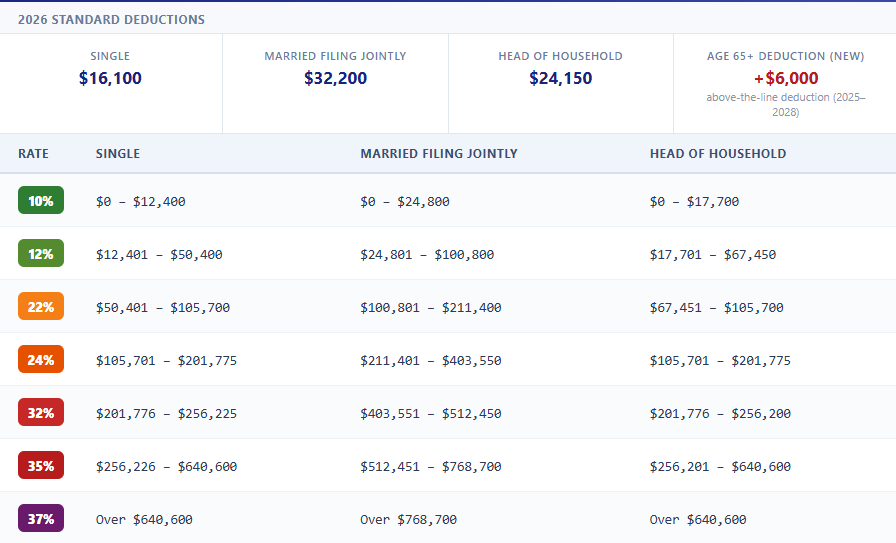

The One Big Beautiful Bill Act also created a new $6,000 above-the-line deduction for taxpayers age 65 and older (available 2025 through 2028), which reduces taxable income and may lower the portion of Social Security benefits subject to federal income tax for many retirees.

Thanks to the advent of remote work during and after the COVID-19 pandemic, many employees moved away from core cities. Notably, these moves may have taken them outside the state where they were employed. Some states established temporary relief provisions to avoid double taxation of income, but many of those provisions may have expired. There are only six states that currently have a "special convenience of employer" rule: Connecticut, Delaware, Nebraska, New Jersey, New York, and Pennsylvania. If you work remotely for ExxonMobil, and you don't currently reside in those states, consult with your tax advisor to determine if there are other ways to mitigate the risk of double taxation.

How ExxonMobil employees can optimize their retirement contributions

Contributing to your company's 401k plan can cut this year's tax bill significantly. With the right planning, these benefits can compound over time. In 2026, the amount you can save increased:

- 2026 limit. Individuals can contribute $24,500 to their 401k plans in 2026.

- Catch-up contributions. Employees age 50 and over can contribute an extra $8,000, bringing their total limit to $32,500. Those who are 60 - 63 years old during calendar year 2026 have a catch up contribution of $11,250, for a combined total of $35,750.

- A major opportunity. Lowering your taxable income by up to $35,750 means less of your money is immediately taxed. As the table here shows, this could save thousands on your current tax bill.

Many investors choose to invest the money they save in taxes. This bonus nest egg then has the opportunity to grow in the market, which can help pay the deferred tax when you take withdrawals from your accounts later in life.

Following the searing rates of inflation Americans experienced in the early 2020s, the slighltly elevated rate of 3.3% for Q1 2026 seems much more palatable (Source: Bureau of Labor Statistics). Still, inflation remains a volatile source of risk to your portfolio, especially for investors in their 50s or 60s. Whether you like it or not, inflation will reduce the purchasing power of your dollars over time.

The Federal Reserve strives to achieve a 2% inflation rate each year, but the 8.3% inflation rate of 2022 reminded us all that this target is anything but a guarantee. To maintain your standard of living throughout your retirement after leaving ExxonMobil, you will have to factor rising costs into your plan. This is doubly important for costs like health care and housing, which have been known to outpace the total inflation rate, sometimes significantly.

An experienced advisor can help you prepare your portfolio for inflation, while taking into account the rest of your comprehensive plan. Speak with a financial advisor today to start planning for the impacts.

*Source: IRS.gov, Yahoo, Bankrate, Forbes

Blogs You May Enjoy:

![]()

Source: Is it Worth the Money to Hire a Financial Advisor? The Balance, 2021

The benefits of investing in your 401k

Starting to save as early as possible matters. Time on your side means compounding can have significant impacts on your future savings. Once you’ve started, continuing to increase and maximize your contributions for your 401k plan is key.

Waiting to invest in your 401k can cost you. This hypothetical illustration shows the potential risks of waiting just 10 years to start investing in an individual retirement account (IRA). Assuming a $100 monthly investment and an annual return of 8%, an investor who starts at age 25 instead of age 35 would have an extra $200,000 in their account when they reach age 65. This example certainly underscores the importance of starting early, but it also illustrates the importance of repeated, continuous investment. $100 a month might not seem like a lot to start, but by sticking with it, both of the investors in our example amassed a significant retirement nest egg.

While the amount you invest towards your retirement depends on your unique financial situation and goals, a good rule of thumb is to consider investing at least 10% of your salary toward retirement through your 30s and 40s. As much as your individual circumstances allow, it should be a goal to maximize your contributions.

Interested in making the most of your 401k strategy at ExxonMobil? The best time to start is today. Click this button to schedule an introductory meeting with one of our ExxonMobil-focused advisors.

What the ExxonMobil "Performance Improvement Plan" (PIP) means for you

ExxonMobil has been issuing PIPs to employees for some time. A PIP is essentially a severance offer to leave the company, with an option to enroll in an improvement program and potentially keep your job. When an employee receives a PIP, it means they fell into ExxonMobil’s “Needs Significant Improvement” (NSI) performance evaluation category. ExxonMobil has raised the number of employees who fall into the NSI category from 3% to as high as 10% of salaried U.S. workers. For employees in their 50s and 60s, understanding these shifts in policy is crucial for planning your future with the company.

Age Penalty Reductions

If you are a pre-65 terminee, you stand to face severe age penalties for each year before 65.

Pension Distribution Options

- Lump Sum. You take the entire value of your pension as a one-time payment.

- Annuity Options.

- Single Life Annuity (SLA). Payments for your lifetime only.

- Joint & Survivor Annuity (J&S). Payments continue for your lifetime, and a portion (often 50%, 75%, or 100%) goes to a designated survivor after your death.

- Period Certain (10/15/20 years). Payments are guaranteed for a specific number of years.

- Partial Lump Sum with Partial Annuity (75%, 50%, 25%). Split the payout into some combination of a lump sum and an annuity.

Important! If you are a "terminee" (a terminated employee who has not yet retired), only the Annuity Options will be available to you.

Pension Protection Act (PPA) Rate Transition

The PPA rate (prescribed by the Pension Protection Act of 2006) is transitioning in. High-quality corporate bond rates, and updated mortality assumptions as prescribed by the IRS, are being used.

Lump-Sum vs. Annuity

ExxonMobil retirees in your state who are eligible for a pension are often given the choice to either receive pension payments for life or take a lump-sum dollar amount upfront for the “equivalent” value of the pension. The idea for those who choose a lump sum is that you could take the money, roll it over to an IRA, invest it, and generate your own cash flows that enable you to take systematic withdrawals following your retirement from ExxonMobil.

On the plus side, a lump sum payment gives you complete flexibility over the funds, potentially allowing you to generate a greater retirement cash flow than you would receive with an annuity. Additionally, if something happens to you, any unused account balance will be available to a surviving spouse or heirs. However, if you fail to invest the funds for sufficient growth, there's a danger that the money could run out during your lifetime, and you may regret not having held onto the pension's "income for life" guarantee.

For its part, a pension annuity provides you with a steady stream of income throughout your lifetime, as long as the pension plan itself remains solvent and doesn’t default. So whether you live 10, 20, or 30 (or more!) years after leaving ExxonMobil, you don’t have to worry about the risk of outliving your money.

However, taking an annuity also comes with some drawbacks. Once you annuitize your pension, you can no longer access the lump sum. Additionally, unlike Social Security benefits, not all company pensions contain a cost of living allowance (COLA). That means the dollar amount of your monthly pension will remain the same throughout your retirement, losing its purchasing power in the face of inflation.

Ultimately, your decision will depend on what kind of return must be generated on that lump sum to replicate the payments of the annuity. After all, if a return of only 1% to 2% on your lump sum can create the same lifetime cash flows you'd see with an annuity, you're at less risk of outliving the lump sum after leaving ExxonMobil, even if you withdraw from it for life. However, if the annuity payments can only be matched by earning a much higher and possibly riskier rate of return, there is a greater risk those returns won’t manifest and you could run out of money.

Interest Rates and Life Expectancy

Current interest rates, as well as your life expectancy at retirement, have a large impact on lump sum payouts from the ExxonMobil pension plan. The Blended Interest Rates is staying steady for retirees who started receiving their ExxonMobil Pension payments in Q4 of 2025 through Q1 2026, Rising rates hurt your lump sum value. The reverse is also true. Decreasing or lower interest rates will increase lump sum values.

Interest rates are important for determining your lump sum option within the pension plan. However, they have no impact on the annuity options. The Retirement Group believes all ExxonMobil employees in the United States should run a detailed RetireKit Cash Flow Analysis comparing their lump sum value to their monthly annuity distribution options, before making a pension election. As enticing as a high lump sum may be, taking an annuity for all or part of your pension may be the better option, especially in a higher interest rate environment. Every person’s situation is different, and a Cash Flow Analysis will show you how your pension choices may play out over the course of 30 years or more.

Grandfathered ExxonMobil Employees

For grandfathered employees, the Q4 of 2025 and Q1 2026 pension rates are 4.00% For non-grandfathered employees, the second and third quarter blended segments also decreased. If these rates continue to fall, lump sum payments may rise in value, but there are no guarantees that rates will decline further in the current interest rate environment.

As we continue to monitor the interest rate environment, we will gain more clarity on how rates are moving. If rates continue to trend lower, lump sum values will increase. However, if rates go higher, lump sums will decline. If you need help determining whether or not you are grandfathered, let us know. Feel free to reach out to The Retirement Group to receive help calculating and assessing your pension options, whether it be the annuity or lump sum. We provide a complimentary Retirement Cash Flow analysis or an update to an existing one.

As we continue to monitor the interest rate environment, we will gain more clarity on how rates are moving. If rates continue to trend lower, lump sum values will increase. However, if rates go higher, lump sums will decline. If you need help determining whether or not you are grandfathered, let us know. Feel free to reach out to The Retirement Group to receive help calculating and assessing your pension options, whether it be the annuity or lump sum. We provide a complimentary Retirement Cash Flow analysis or an update to an existing one.

By knowing where you stand in your 50s and 60s, you can make a more prudent decision when determining whether to retire soon, work longer, or delay the commencement of your pension benefit. For instance, working longer will generate more earned income, but this may be offset by a reduction in a future lump sum benefit, which could translate into working for less money.

The benefits of working with a financial advisor for your 401k

When faced with a problem or challenge, many of us are programmed to try to figure it out on our own rather than ask for help. But with 401k investing, choosing to go it alone can significantly impact your outcomes, especially as you approach your 60s.

Over half of plan participants in the United States admit they don’t have the time, interest, or knowledge needed to manage their 401k portfolio. But the benefits of getting help go beyond convenience.

According to a study from Charles Schwab, the annual performance gap between those who get help and those who do not is 3.32% net of fees. This means a 45-year-old participant could see a 79% boost in wealth by age 65 simply by working with an advisor. That’s a big difference.

That's why it's important to consult with an advisor experienced with ExxonMobil's retirement benefits. If you're looking for guidance from an advisor who's been through it before, reach out to an advisor from The Retirement Group today.

Seeing Results

Getting help can be the key to better results across the 401k board.

A Charles Schwab study found several positive outcomes common to those using independent professional advice. They include:

- Improved savings rates – 70% of participants who relied on 401k advice increased their contributions.

- Increased diversification – Participants who managed their own portfolios invested in an average of just under four asset classes, while participants in advice-based portfolios invested in a minimum of eight asset classes.

- Increased likelihood of staying the course – Getting advice increased the chances of participants staying true to their investment objectives, making them less reactive during volatile market conditions and more likely to remain in their original 401k investments during a downturn. Don’t try to do it alone.

Get help with your company's 401k plan investments. Your nest egg will thank you.

It’s important to know that certain withdrawals are subject to regular federal income tax and you may also be subject to an additional 10% penalty tax depending on your age.

You can determine if you’re eligible for a withdrawal, and request one, online or by calling the ExxonMobil Benefits Center in the United States. Your plan summary outlines more information and possible restrictions on rollovers and withdrawals.

You should also know that the plan administrator reserves the right to modify the rules regarding withdrawals at any time, and may further restrict or limit the availability of withdrawals for administrative or other reasons. All plan participants will be advised of any such restrictions, which apply equally to all ExxonMobil employees.

The Net Unrealized Appreciation (NUA) Strategy

When you qualify to withdraw funds from your 401k plan, you have three options:

- Roll over your qualified plan to an IRA and continue deferring taxes.

- Take a distribution and pay ordinary income tax on the full amount.

- Take advantage of NUA and reap the benefits of a more favorable tax structure on gains.

How does Net Unrealized Appreciation work?

First, you must be eligible for a distribution from your qualified company-sponsored plan, which typically happens at retirement age. Generally, you would take a lump sum distribution from the plan, distributing all assets from the plan during a one-year period. The portion of the plan that is made up of mutual funds and other investments can be rolled into an IRA for further tax deferral. The highly appreciated company stock is then transferred to a non-retirement account.

The tax benefit comes when you transfer the company stock from a tax-deferred account to a taxable account. At this time, you apply NUA and you incur an ordinary income tax liability on only the cost basis of your stock. The appreciated value of the stock above its basis is not taxed at ordinary income tax rates but at long-term capital gains rates of 0%, 15%, or 20%, depending on your taxable income. The 3.8% Net Investment Income Tax under §1411 may also apply if your income is above $200,000 (single) or $250,000 (MFJ). This could mean a potential savings of over 30%.

Example: Net Unrealized Appreciation (NUA) Tax Savings

As an ExxonMobil employee residing in the United States, you may be interested in learning more about NUA. Reach out today to schedule a complimentary one-to-one session with a financial advisor from The Retirement Group.

IRA Withdrawal

Your retirement assets may be spread across several retirement accounts: IRAs, 401ks, taxable accounts, and others.

What is the most efficient way to take your retirement income after leaving ExxonMobil?

This question relates to something called withdrawal sequencing, and it's a problem we're well-equipped to handle at The Retirement Group.

You may want to consider meeting your income needs in retirement by first drawing down taxable accounts rather than tax-deferred accounts. This may help your retirement assets with your company last longer as they continue to potentially grow tax deferred.

You will also need to plan to take the required minimum distributions (RMDs) from any company-sponsored retirement plans and traditional or rollover IRA accounts when you reach age 73. Under SECURE 2.0, this age is 73 for those born between 1951 and 1959, and 75 for those born in 1960 or later.

Two flexible distribution options for your IRA

When you need to draw on your IRA for income or to take your RMDs, you have a few choices. Regardless of what you choose, IRA distributions are subject to income taxes and may be subject to penalties and other conditions if you’re under 59½.

Option 1. Partial withdrawals: Withdraw any amount from your IRA at any time. If you’re 73 or over, you’ll have to take at least enough from one or more IRAs to meet your annual RMD.

Option 2. Systematic withdrawal plans: Structure regular, automatic withdrawals from your IRA by choosing the amount and frequency to meet your income needs after retiring from ExxonMobil. If you’re under 59½, you may be subject to a 10% early withdrawal penalty (unless your withdrawal plan meets Code Section 72(t) rules).

Your tax advisor can help you understand distribution options, determine RMD requirements, calculate RMDs, and set up a systematic withdrawal plan.

Using an HSA for retirement health care

Health care costs are increasing drastically. According to the Centers for Medicare & Medicaid Services, health care in 2025 accounted for over 17% of the United State's GDP, which amounted to $4.5 trillion.

This raises the question: How will you be paying for health care in retirement?

Health Savings Accounts (HSAs) are tax-advantaged accounts designed for individuals with high-deductible insurance plans. For 2026, the IRS defines high-deductible plans as those with a minimum deductible of $1,700 for individuals, or $3,400 for families.

HSAs are often celebrated for their utility in managing health care expenses in a tax-smart way, with three primary benefits:

- HSAs allow contributions to be made pre-tax.

- Investments within HSAs grow tax-free.

- Withdrawals are tax-free for qualified medical expenses.

Thanks to this triple tax advantage, HSAs are a potent retirement savings vehicle, especially after you've maxed out the employer match to your 401k in the United States.

HSA Contribution Limits & Retirement Strategy

In 2026, individuals can contribute $4,400 to an HSA, and families can contribute $8,750. Those aged 55 and older can contribute an additional $1,000.

When it comes to its place in your retirement toolbelt, HSAs really shine after you reach your employer's maximum match in 401k contributions. While 401ks offer tax-deductible contributions and tax-deferred growth, their withdrawals are taxable. HSAs bypass the withdrawal tax for qualified medical expenses, which are a significant (and increasing!) portion of retirement costs.

However, after age 65, the HSA flexes its muscles even more. After this age, funds can be withdrawn for any purpose, and subject to only regular income tax if used for non-medical expenses. This flexibility offers the benefits of traditional retirement accounts, but with the added advantage of tax-free withdrawals for qualified medical costs.

Further, HSAs do not have required minimum distributions (RMDs) like 401ks and traditional IRAs do, offering more control over tax planning in retirement. This makes HSAs particularly relevant for those who don't anticipate needing all of their funds right away in retirement, or who want to reduce their taxable income, perhaps as a part of a deferred compensation strategy.

HSA Investment Strategy Insights: Initially, conservative investment within an HSA is prudent. Early on, it's important to focus on maintaining sufficient liquid funds to cover near-term deductibles and out-of-pocket medical expenses. However, once you've established a solid financial cushion, treating an HSA like a retirement account by investing in a diversified mix of assets can significantly boost long-term opportunity and flexibility.

What can an HSA cover?

In retirement, HSAs can cover a range of expenses:

- Medical expenses. You can use HSA funds tax-free for qualified medical expenses, which include most doctor visits, prescriptions, and dental or vision care.

- Medicare premiums. HSA funds can pay for Medicare Part B, Part D, and Medicare Advantage premiums.

- Long-term care. HSA funds can cover some amount of qualified long-term care insurance premiums or services.

- Non-medical expenses. After age 65, you can withdraw HSA funds for non-medical expenses without penalty, although these withdrawals will be taxed as regular income.

HSAs are a powerful retirement tool, with unique advantages that can augment your ExxonMobil health care benefits. By making strategic contributions and considerate withdrawals, you can optimize your financial health in retirement, while also prioritizing your physical health.

Short-Term & Long-Term Disability Coverage

- Short-Term: Depending on your plan, you may have access to short-term disability (STD) benefits through ExxonMobil.

- Long-Term: Your plan's long-term disability (LTD) benefits are designed to provide you with income if you are absent from employment for six consecutive months or longer due to an eligible illness or injury.

ExxonMobil Life Insurance in Retirement

At ExxonMobil, if you have 10 years of service and are at least 50 years of age, you may be able to continue your employee-paid coverage into retirement. No action is required by you to maintain your coverage, but the cost of your coverage may increase. Check with ExxonMobil for more details.

Generally, your contributions as a retiree will be higher than those you pay as an employee. After you retire, you can reduce the amount of supplementary coverage you have at any time. The change will take effect on the first of the following month. In some cases, you may be able to purchase additional supplementary coverage of one times pay (within 31 days of retirement) if your retiree basic life insurance is less than one times your active pay.

Important Note: If you stop paying supplementary contributions, your coverage will end. You will not be able to reinstate it. Please read the ExxonMobil SPD for more details.

Claiming Social Security is one thing, understanding how your claim works is something else entirely. Understanding Social Security is a difficult but crucial step in assessing your retirement paycheck. For many Americans, Social Security benefits are core to their retirement income strategy. However, when and why you claim them depends on your overall withdrawal strategy.

To help you make an informed decision, let's explore three main steps you should follow to solidify your Social Security strategy at ExxonMobil:

Step 1. Decide when to claim your Social Security benefits.

Social Security benefits can be significant, but at the end of the day, they're just one part of your overall financial picture. When considering the timing of your claim, keep this general principle in mind: The later you begin receiving benefits, the larger those benefits will be.

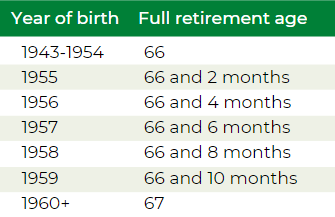

The full monthly Social Security retirement benefit is based on applying at the Full Retirement Age (FRA), which is age 67 for those born 1960 or later. For every year you wait after you reach the FRA, your benefit amount increases 8%. It reaches a maximum at age 70. If we do the math, we can determine that, if you start claiming at age 70, your monthly benefit will be 124% the full benefit.

However, you can also apply before you reach FRA, as early as age 62. You will receive a reduced benefit if you do so, but this option could make sense for those who want to start claiming their benefit earlier for longevity reasons.

Step 2. Understand the tax implications.

For all but the lowest-income retirees, Social Security benefits are actually taxable. Only individuals with provisional income under $25,000, or $32,000 if married filing jointly, receive their benefits tax-free. Otherwise, up to 85% of your benefits will be treated as taxable income.

Furthermore, depending on where you live, your Social Security benefits may even be taxed at the state level. If you plan to move for retirement, the tax regime in the state you're moving to can be a relevant consideration.

Step 3. Start preparing today.

Even if your retirement is right around the corner, you can make decisions today that will impact you for years, or decades, to come. For instance, delaying your Social Security claiming date by even a year or two can snowball into a significant benefit. To bridge the gap between their retirement date and their claiming date, some people create a "slush fund" while they're working to take the place of the Social Security benefits they would receive from claiming at FRA. Whether these funds come from a 401k, IRA, or brokerage account, integrating a bit of extra padding in your planning can pay off in the long run.

Always remember, your Social Security benefit is just one part of your overall financial picture. And when you start to consider tax implications, withdrawal sequencing, and effective diversification (beyond just the asset class), the picture can start to get complicated. That's what we're here to help with. At The Retirement Group, we've been assisting ExxonMobil employees to and through retirement for years. If you're interested in speaking with an experienced advisor who's been through the process before, reach out today.

ExxonMobil Medicare Coverage for Retirees

Are you eligible for Medicare or will be soon? If you or your dependents are eligible after you leave ExxonMobil, Medicare generally becomes the primary coverage for you or any of your dependents as soon as they are eligible for Medicare. This will affect your company-provided medical benefits.

It's your responsibility to enroll in Medicare Parts A and B when you first become eligible, and you must stay enrolled to have coverage for Medicare-eligible expenses. This applies to your Medicare-eligible dependents as well.

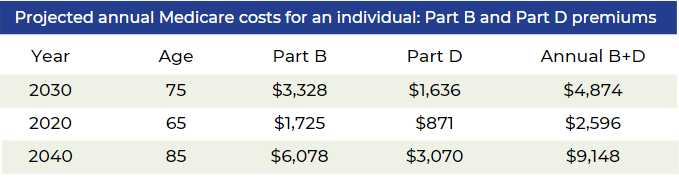

The Reality of Medical Costs in Retirement

Divorce and Retirement Benefits Explained

Social Security Benefits. Divorce can significantly impact retirement benefits, including Social Security. Understanding how divorce affects Social Security is essential for retirement planning, especially if you were married for a long time. In some cases, divorced individuals may be eligible to claim benefits based on their former spouse's work record.

You can apply for a divorced spouse’s benefit if the following criteria are met:

- You’re at least 62 years of age.

- You were married for at least 10 years prior to the divorce.

- You are currently unmarried.

- Your ex-spouse is entitled to Social Security benefits.

- Your own Social Security benefit amount is less than your spousal benefit amount, which is equal to one-half of what your ex’s full benefit amount would be if claimed at Full Retirement Age (FRA).

Unlike a married couple, your ex-spouse doesn’t have to have filed for Social Security before you can apply for your divorced spouse’s benefit. However, this only applies if you’ve been divorced for at least two years, and your ex is at least 62 years of age. If the divorce was less than two years ago, your ex must already be receiving benefits before you can file as a divorced spouse.

Social Security Survivor Benefits.

Many people are surprised that divorce doesn't disqualify you from receiving survivor benefits if your spouse dies. You can claim a divorced spouse's survivor benefit if the following conditions are met:

- Your ex-spouse is deceased.

- You are at least 60 years old.

- You were married for at least 10 years.

- You are single or you remarried after age 60.

If you qualify for survivor benefits and your own Social Security benefits, you can choose to start with survivor benefits and switch to your own later, or vice versa, depending on which option gives you the highest payout over time. If this pertains to you, we recommend speaking to a qualified financial advisor, because planning your Social Security strategy in advance is critical to optimizing your outcomes.

Divorce and ExxonMobil Pension Benefits

In the process of divorcing?

If your divorce isn’t final before your retirement date from your company, you’re still considered married. You have two options:

- Retire from ExxonMobil before your divorce is final and elect a joint pension of at least 50% with your spouse, or get your spouse’s signed, notarized consent to a different election or lump sum.

- Delay your retirement from your company until after your divorce is final and you can provide the required divorce documentation.

6.png)