David Else - Senior Vice President, Financial Advisor RICP®, CKA

Derek Green - Senior Vice President, Financial Advisor

It is imperative for individuals to be aware of new changes made by the IRS. The main factors that will impact employees will be the following:

- The 2024 standard deduction will increase to $14,600 for single filers and those married filing separately, $29,200 for joint filers, and $21,900 for heads of household.

- Taxpayers who are over the age of 65 or blind can add an additional $1,550 to their standard deduction. That amount jumps to $1,950 if also unmarried or not a surviving spouse.

Retirement account contributions: Contributing to your company's 401k plan can cut your tax bill significantly, and the amount you can save has increased for 2024. The amount individuals can contribute to their 401(k) plans in 2024 will increase to $23,000 -- up from $22,500 for 2023. The catch-up contribution limit for employees age 50 and over will increase to $7,500.

There are important changes for the Earned Income Tax Credit (EITC) that you, as a taxpayer employed by a corporation, should know:

- The tax year 2024 maximum Earned Income Tax Credit amount is $7,830 for qualifying taxpayers who have three or more qualifying children, up from $7,430 for tax year 2023.

- Married taxpayers filing separately can qualify: You can claim the EITC as married filing separately if you meet other qualifications. This was not available in previous years.

Deduction for cash charitable contributions: The special deduction that allowed single nonitemizers to deduct up to $300—and married filing jointly couples to deduct $600— in cash donations to qualifying charities has expired.

Child Tax Credit changes:

- The maximum tax credit per qualifying child is $2,000 for children five and under – or $3,000 for children six through 17 years old. Additionally, you can't receive a portion of the credit in advance, as was the case in 2023.

- As a parent or guardian, you are eligible for the Child Tax Credit if your adjusted gross income is less than $200,000 when filing individually or less than $400,000 if you're filing a joint return with a spouse.

- A 70 percent, partial refundability affecting individuals whose tax bill falls below the credit amount.

2024 Tax Brackets

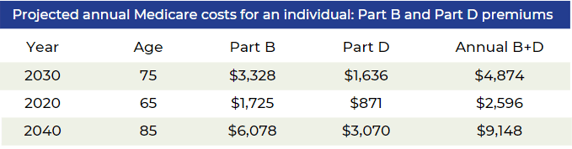

Inflation reduces purchasing power over time as the same basket of goods will cost more as prices rise. In order to maintain the same standard of living throughout your retirement after leaving your company, you will have to factor rising costs into your plan. While the Federal Reserve strives to achieve a 2% inflation rate each year, in 2023 that rate shot up to 4.9% which was a drastic increase from 2020’s 1.4%. While prices as a whole have risen dramatically, there are specific areas to pay attention to if you are nearing or in retirement from your company, like healthcare.

It is crucial to take all of these factors into consideration when constructing your holistic plan for retirement from your company.

*Source: IRS.gov, Yahoo, Bankrate, Forbes

Blogs You May Enjoy:

![]()

Source: Is it Worth the Money to Hire a Financial Advisor? The Balance, 2021

Starting to save as early as possible matters. Time on your side means compounding can have significant impacts on your future savings. And, once you’ve started, continuing to increase and maximize your contributions for your 401(k) plan is key.

Lump-Sum vs. Annuity

Retirees who are eligible for a pension are often offered the choice of receiving their pension payments for life, or receive a lump-sum amount all-at-once. The lump sum is the equivalent present value of the monthly pension income stream – with the idea that you could then take the money (rolling it over to an IRA), invest it, and generate your own cash flow by taking systematic withdrawals throughout your retirement years.

The upside of electing the monthly pension is that the payments are guaranteed to continue for life (at least to the extent that the pension plan itself remains in place and solvent and doesn’t default). Thus, whether you live 10, 20, 30, or more years after retiring from your company, you don’t have to worry about the risk of outliving the monthly pension.

The major downside of the monthly pension are the early and untimely passing of the retiree and joint annuitant. This often translates into a reduction in the benefit or the pension ending altogether upon the passing. The other downside, it that, unlike Social Security, company pensions rarely contain a COLA (Cost of Living Allowance). As a result, with the dollar amount of monthly pension remaining the same throughout retirement, it will lose purchasing power when the rate of inflation increases.

In contrast, selecting the lump-sum gives you the potential to invest, earn more growth, and potentially generate even greater retirement cash flow. Additionally, if something happens to you, any unused account balance will be available to a surviving spouse or heirs. However, if you fail to invest the funds for sufficient growth, there’s a danger that the money could run out altogether and you may regret not having held onto the pension’s “income for life” guarantee.

Ultimately, the “risk” assessment that should be done to determine whether or not you should take the lump sum or the guaranteed lifetime payments that your company pension offers, depends on what kind of return must be generated on that lump-sum to replicate the payments of the annuity. After all, if it would only take a return of 1% to 2% on that lump-sum to create the same monthly pension cash flow stream, there is less risk that you will outlive the lump-sum. However, if the pension payments can only be replaced with a higher and much riskier rate of return, there is, in turn, a greater risk those returns won’t manifest and you could run out of money.

Interest Rates and Life Expectancy

Current interest rates, as well as your life expectancy at retirement, have a significant impact on lump sum payouts of defined benefit pension plans.

Rising interest rates have an inverse relationship to pension lump sum values. The reverse is also true; decreasing or lower interest rates will increase pension lump sum values. Interest rates are important for determining your lump sum option within the pension plan.

The Retirement Group believes all employees should obtain a detailed RetireKit Cash Flow Analysis comparing their lump sum value versus the monthly annuity distribution options, before making their pension elections.

As enticing as a lump sum may be, the monthly annuity for all or a portion of the pension, may still be an attractive option, especially in a high interest rate environment.

Each person’s situation is different, and a complimentary Cash Flow Analysis, from The Retirement Group, will show you how your pension choices stack up and play out over the course of your retirement years which may be two, three, four or more decades in retirement.

By knowing where you stand, you can make a more prudent decision regarding the optimal time to retire, and which pension distribution option meets your needs the best.

Over half of plan participants admit they don’t have the time, interest or knowledge needed to manage their 401(k) portfolio. But the benefits of getting help goes beyond convenience. Studies like this one, from Charles Schwab, show those plan participants who get help with their investments tend to have portfolios that perform better: The annual performance gap between those who get help and those who do not is 3.32% net of fees. This means a 45-year-old participant could see a 79% boost in wealth by age 65 simply by contacting an advisor. That’s a pretty big difference.

Getting help can be the key to better results across the 401(k) board.

A Charles Schwab study found several positive outcomes common to those using independent professional advice. They include:

- Improved savings rates – 70% of participants who used 401(k) advice increased their contributions.

- Increased diversification – Participants who managed their own portfolios invested in an average of just under four asset classes, while participants in advice-based portfolios invested in a minimum of eight asset classes.

- Increased likelihood of staying the course – Getting advice increased the chances of participants staying true to their investment objectives, making them less reactive during volatile market conditions and more likely to remain in their original 401(k) investments during a downturn. Don’t try to do it alone. Get help with your company's 401(k) plan investments. Your nest egg will thank you.

Net Unrealized Appreciation (NUA)

When you qualify for a distribution, you have three options:

- Roll-over your qualified plan to an IRA and continue deferring taxes.

- Take a distribution and pay ordinary income tax on the full amount.

- Take advantage of NUA and reap the benefits of a more favorable tax structure on gains.

How does Net Unrealized Appreciation work?

First an employee must be eligible for a distribution from their qualified company-sponsored plan. Generally, at retirement or age 59 1⁄2, the employee takes a 'lump-sum' distribution from the plan, distributing all assets from the plan during a 1-year period. The portion of the plan that is made up of mutual funds and other investments can be rolled into an IRA for further tax deferral. The highly appreciated company stock is then transferred to a non-retirement account.

The tax benefit comes when you transfer the company stock from a tax-deferred account to a taxable account. At this time, you apply NUA and you incur an ordinary income tax liability on only the cost basis of your stock. The appreciated value of the stock above its basis is not taxed at the higher ordinary income tax but at the lower long-term capital gains rate, currently 15%. This could mean a potential savings of over 30%.

You may be interested in learning more about NUA with a complimentary one-on-one session with a financial advisor from The Retirement Group.

IRA Withdrawal

When you qualify for a distribution, you have three options:

Your retirement assets may consist of several retirement accounts: IRAs, 401(k)s, taxable accounts, and others.

So, what is the most efficient way to take your retirement income after leaving your company?

You may want to consider meeting your income needs in retirement by first drawing down taxable accounts rather than tax-deferred accounts.

This may help your retirement assets with your company last longer as they continue to potentially grow tax deferred.

You will also need to plan to take the required minimum distributions (RMDs) from any company-sponsored retirement plans and traditional or rollover IRA accounts.

That is due to IRS requirements for 2024 to begin taking distributions from these types of accounts when you reach age 73. Beginning in 2024, the excise tax for every dollar of your RMD under-distributed is reduced from 50% to 25%.

There is new legislation that allows account owners to delay taking their first RMD until April 1 following the later of the calendar year they reach age 73 or, in a workplace retirement plan, retire.

Two flexible distribution options for your IRA

When you need to draw on your IRA for income or take your RMDs, you have a few choices. Regardless of what you choose, IRA distributions are subject to income taxes and may be subject to penalties and other conditions if you’re under 59½.

Partial withdrawals: Withdraw any amount from your IRA at any time. If you’re 73 or over, you’ll have to take at least enough from one or more IRAs to meet your annual RMD.

Systematic withdrawal plans: Structure regular, automatic withdrawals from your IRA by choosing the amount and frequency to meet your income needs after retiring from your company. If you’re under 59½, you may be subject to a 10% early withdrawal penalty (unless your withdrawal plan meets Code Section 72(t) rules).

Your tax advisor can help you understand distribution options, determine RMD requirements, calculate RMDs, and set up a systematic withdrawal plan.

You and your Medicare-eligible dependents must enroll in Medicare Parts A and B when you first become eligible. Medical and MH/SA benefits payable under the company's-sponsored plan will be reduced by the amounts Medicare Parts A and B would have paid whether you actually enroll in them or not.

6.png)