For people in your city, your state, it's important to remain up-to-date about changes made by the IRS, especially as they approach retirement age. Here are some of the main factors currently affecting employees.

Increase in standard deduction:

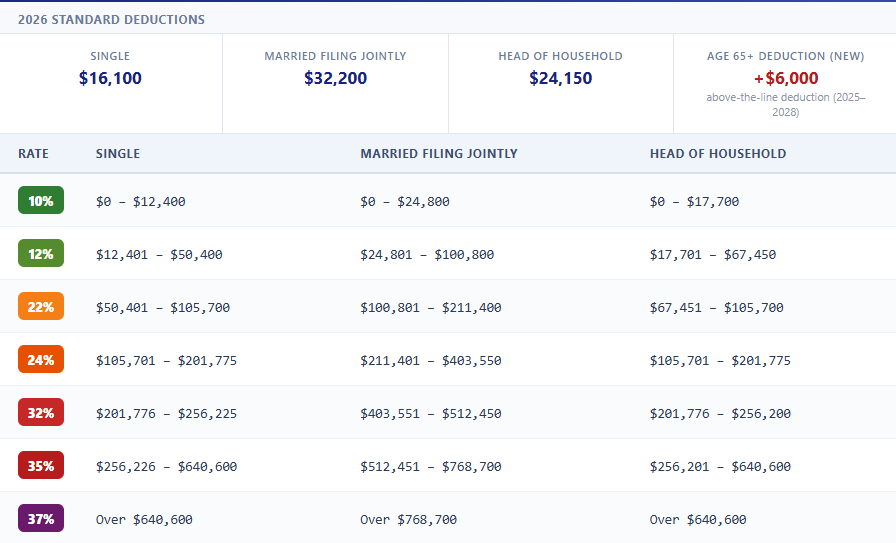

- Under the One Big Beautiful Bill Act (signed July 4, 2025), the standard deduction was made permanent and further increased for 2026: $16,100 for single filers and married filing separately, $32,200 for married filing jointly, and $24,150 for heads of household.

- Taxpayers who are over the age of 65 or blind can add an additional $1,650 per qualifying status to their standard deduction. The additional amount is $2,050 if the taxpayer is also unmarried and not a surviving spouse. A married couple filing jointly with both spouses age 65 or older can therefore claim a total of $3,300 in additional standard deduction.`

Retirement account contributions:

Contributing to your company's 401k plan can cut your tax bill significantly. For 2026, the amount individuals can contribute to their 401(k) plans increased to $24,500, up from $23,500 in 2025. The catch-up contribution limit for employees age 50 and over is $8,000. For those turning 60 - 63 years of age during calendar year 2026, the catch-up provision is $11,250.

Changes to the Earned Income Tax Credit (EITC):

As a taxpayer employed by a corporation, keep in mind that:

- The maximum Earned Income Tax Credit for 2026 is $8,231 for qualifying taxpayers who have three or more qualifying children, up from $8,046 for tax year 2025.

- Married taxpayers filing separately can qualify: You can claim the EITC as married filing separately if you meet other qualifications. This was not available in previous years.

Child Tax Credit changes:

- In 2026, the child tax credit is $2,200 per qualifying child under the age of 17, with a maximum refundable amount of $1,700.

- You may be eligible for the full child tax credit amount if your modified adjusted gross income is $400,000 or below (married filing jointly) or $200,000 or below (all other filers).

- If your income exceeds the limits, the credit is reduced by $50 for each $1,000 of income above the threshold until it phases out completely.

Other notable changes for tax year 2026 include the following:

- Alternative minimum tax exemption amounts: For 2026, the exemption amount for unmarried individuals increases to $90,100 ($70,100 for married individuals filing separately) and begins to phase out at $500,000 for unmarried individuals and $1,000,000 for joint filers. Under the One Big Beautiful Bill Act (§70107), the phase-out rate is 50% (up from 25%), and these thresholds are not indexed for inflation in 2026.

- Qualified transportation fringe benefit: For 2026, the monthly limits for the qualified transportation fringe benefit and for qualified parking rise to $340 per month, up from $325 per month in 2025.

- Health flexible spending cafeteria plans: For tax years beginning in 2026, the dollar limit for employee salary reductions for contributions to health flexible spending arrangements rises to $3,400, up from $3,300 in 2025. For cafeteria plans that permit the carryover of unused amounts, the maximum carryover rises to $680, up from $660 in 2025.

- Medical savings accounts: For 2026, participants with self-only coverage must have an annual deductible of at least $2,900 but not more than $4,400 (compared to $2,850 to $4,300 in 2025). The maximum out-of-pocket expense amount rises to $5,850 (vs. $5,700 in 2025). For family coverage, the annual deductible must fall between $5,850 and $8,750 in 2026, up from $5,700 to $8,550 in 2025. For family coverage, the out-of-pocket expense limit is $10,700 for 2026, rising from $10,500 in 2025.

- Foreign earned income exclusion: For 2026, the foreign earned income exclusion is $132,900, up from $130,000 in 2025.

Addressing inflation in 2026

Inflation reduces purchasing power, with the same basket of goods costing more over time. To mitigate the effect of this erosion, it's important to factor inflation into your retirement plan so you can maintain the same standard of living once you retire from Kaiser Permanente.

While the Federal Reserve strives to achieve a 2% inflation rate each year, in Q1 2026 that rate was 3.3%. Certain expenses, such as health care and housing, also tend to outpace the total inflation rate, which matters more if you are nearing or in retirement. It is crucial to take these factors into account when constructing your holistic plan for retirement.

*Sources: IRS.gov, Yahoo, Bankrate, Forbes

Blogs You May Enjoy:

![]()

Source: Is it Worth the Money to Hire a Financial Advisor? The Balance, 2021

Starting to save as early as possible matters. Time on your side means compounding can have significant impacts on your future savings. And, once you’ve started, continuing to increase and maximize your contributions for your 401k plan is key.

Credited Service

Credited service begins on your date of hire and is based on 2,000 hours of compensated service each calendar year. Proportional credited service is granted for years in which compensated service is less than 2,000 hours.

Benefit Formula

2% of Highest Average Compensation (HAC) per year during first 20 years of credited service, and 1% per year thereafter.

Payment Options

Life annuity, joint and survivor annuity, period certain, or installments.

Permanente Contribution Plan (Plan 2)

TPMG contributes to Plan 2 based upon your eligible compensation (base compensation plus bonus) each pay period. Plan 2 contributions are equal to 5% of the amount of eligible compensation you receive, up to the Social Security Wage Base (SSWB), plus 10% of your eligible compensation over the SSWB up to the maximum IRS compensation limit.

For 2026, the SSWB limit is $184,500. The limit on the amount of compensation that can be taken into account when determining contributions and benefits in retirement plans is $360,000 for calendar year 2026.

Plan 2 contributions begin the first of the month following the completion of 1,000 hours of service within an anniversary year.

Salary Deferral Plan 401k (Plan 3)

Your 401k contributions can be made on a pre-tax or Roth (post-tax) basis. You choose how you want to invest your savings.

Contributions are subject to annual IRS and other limits, as shown in the table below.

Contributions can begin the first of the month following your date of hire. If you do not make an election within 30 days of your hire date, you will be automatically enrolled at an employee pre-tax contribution rate of 6%. If you were automatically enrolled at 6% and do not make a change, your contribution percentage will increase by 1% on your anniversary date each year up to a maximum of 15%.

TPMG (physicians) Pension Plan 2 (2025 maximum)

Sample KP Pension Calculations

TPMG (Salaried Employees)

How Pension Benefit Is Calculated:

Final Average Monthly Compensation

multiplied by

Years of credited service

multiplied by

Pension benefit multiplier

Defined Benefit Pension Plan Features, By Group

There are three parts to the Northern California KFH plan. This is for salaried non-union employees at Kaiser Permanente, which includes pharmacists.

Part 1: Kaiser Permanente Tax Sheltered Annuity Plan (TSA)

This plan offers immediate eligibility, with matching starting after two years of employment. Matching is 2% of your salary up to the Social Security wage base limit, and then an additional 5% on salary above this limit.

Part 2: Kaiser Permanente Supplemental Savings and Retirement Plan

This is a qualified plan where the employer contributes 5% of an employee's base salary after two years of service with the company. The employee can add after-tax contributions into the plan and the employer contribution is immediately vested.

Part 3: Kaiser Permanente Salaried Retirement Plan

This plan is the pension (defined benefit plan) and the company contributes into the plan based on a formula of FAP (last 10 years of employment and the average of the 60 highest consecutive months) multiplied by a pension multiplier of 1.5 minus age penalties of 5% for retirement between the ages of 55-60 and 3% between the ages of 60-65.

Retiree Benefits

You may be eligible for retiree health and welfare benefits when you retire, if you meet certain age and years of service requirements.

Other Benefits

Employee Assistance Program

This program provides free and confidential counseling for personal issues, as well as referrals for child and elder care.

Parent Medical Coverage

Your Medicare-eligible parents, step-parents, parents-in-law, or parents of your domestic partner may have an opportunity to enroll in Kaiser Permanente medical coverage at their own expense.

Voluntary Programs

You may enroll in Benefits by Design Voluntary Programs at your own expense if you are regularly scheduled to work 20 or more hours per week. Programs offered include long-term care, term life, pet, auto, and home insurance, as well as legal services and identity theft protection.

Tuition Reimbursement

Tuition reimbursement helps you continue your education in subjects that will improve your job performance, potential for advancement, and employability. You can be reimbursed up to $3,000 per calendar year for expenses such as tuition and textbooks, including up to $500 for travel expenses.

Additional Resources

As a Kaiser Permanente employee, you also have access to:

-

- Career and development opportunities to help you grow your skills and career, including professional development courses through KP Learn.

-

- Opportunities to volunteer in communities that KP serves.

-

- Employee discounts on entertainment, travel, child care, health and fitness programs, electronics, and more. You also receive discounts on over-the-counter medications and other products purchased from a KP pharmacy.

-

- Healthy Workforce resources and tools to help you keep active, eat well, and thrive. If your region meets the Total Health Incentive Plan’s goals for employees to adopt a healthier lifestyle, you may also have a chance to earn up to $500 per year.

KP Pension Distribution Options

Please note: each KP pension varies; options listed below may not be available with your pension.

Standard Forms of Payment

If you are single: the standard form of payment is the Single Life Annuity.

If you are married: your spouse is entitled by federal law to receive benefits, so your standard form of payment is the 50% Joint and Survivor Annuity. This means you are legally required to obtain your spouse’s consent to elect other forms of payment. The consent must be in writing and notarized no more than 90 days before the benefits begin.

Available Forms of Payment

• Lump Sum: Under this option, you receive a one-time lump sum amount. After you receive the Lump Sum

payment, there are no more payments due under the plan. The Lump Sum can be rolled over into a traditional

IRA, Roth IRA, or another employer’s qualified plan, if that plan accepts rollovers.

• Single Life Annuity: Under this option, you receive a monthly pension benefit until your death. However, all

pension payments stop when you die regardless of marital status. This is the standard form of payment if you

are not married (as defined by federal law) on your Benefit Commencement Date.

• 50%, 66 2/3%, and 75% Joint and Survivor Annuities: Under this option, you receive a reduced monthly benefit until your death. If you die before your beneficiary, 50%, 66 2/3%, or 75% (as elected by you) of the amount you receive will then be paid to your beneficiary as long as he or she lives. However, if your beneficiary dies before you, your monthly benefit will be reduced to the 50%, 66 2/3%, or 75% survivor benefit for the rest of your lifetime after your beneficiary's death. This option requires the designation of one person as your beneficiary, and after your payments begin, you cannot change your beneficiary. The 50% Joint and Survivor Annuity is the standard form of payment if you are married (as defined by federal law). If you are married, you must select this form of payment, with your spouse as your beneficiary, unless your spouse consents to a different election. Your spouse’s consent must be on the appropriate form and notarized. Once you begin receiving payments, you may not change your beneficiary. The monthly pension benefit you or your beneficiary receives under this option will be less than the monthly pension benefit under a Single Life Annuity because payments may continue after death. The actual difference depends on the percentage you elect, as well as the age difference between you and your beneficiary.

• 100% Joint and Survivor Annuity with 15-Year Guarantee Period and Pop-Up: Under this option,

you receive a reduced monthly benefit until your death. If you die before your Joint and Survivor Annuity

beneficiary, 100% of the monthly payment you received will then be paid to that beneficiary as long as he or she lives. Conversely, if your Joint and Survivor Annuity beneficiary dies first, the monthly amount payable to you will "pop up” to the Single Life Annuity monthly amount for the duration of your life. If you and your Joint and Survivor Annuity beneficiary both die before the 180 months (15 years) of guaranteed payments are made, payments equal to the 100% Joint and Survivor Annuity monthly benefit will be made to a designated beneficiary until the expiration of the guaranteed payment period. If your designated beneficiary does not survive to the end of the guaranteed payment period, the present value of the remaining payments will be paid to that beneficiary’s estate. This option requires the designation of both a Joint and Survivor Annuity beneficiary and a beneficiary for the guarantee period benefit. If you and your Joint and Survivor Annuity beneficiary die before 180 payments and there is no surviving designated beneficiary, the remaining payments will be made to your surviving spouse or domestic partner, if any. If there is no surviving spouse or domestic partner, the present value of the remaining payments will be paid to your estate.

• 5-, 10-, 15- and 20-Year Certain and Life Annuity: Under this option, you receive a monthly pension benefit

for your lifetime with payments that will be made for a period of at least 5, 10, 15, or 20 years, whichever you

select. If you die before the end of the specified period, your designated beneficiary will receive the monthly

payments for the remainder of the specified period. If your designated beneficiary dies before the end of the specified period, the present value of the remaining monthly benefits will be paid in accordance with the plan.

For example, if you elect the 10-year option and die after receiving payments for only six years, your beneficiary would receive monthly payments for the remaining four years. If you live longer than 10 years, payments will continue to you for as long as you live, but there are no payments to your beneficiary after your death. The monthly amount paid to you under this option will be less than you would receive under a Single Life Annuity because of the possibility that payments will continue after your death. The actual difference depends on your age at retirement and the length of the specified period. Unlike a Joint and Survivor Annuity, you can change your beneficiary for this form of payment after your payments begin.

• Fixed Monthly Installments: Under this option, you receive a fixed number of monthly payments, and then

all payments stop. You may elect to receive installments for 60, 120, 180, 240, or 360 months, or any months

up to 360. If you die after your payments stop because you have received the fixed number of monthly

payments, there will be no benefit paid to any beneficiary. If you die before you receive the fixed number of

monthly payments, your surviving designated beneficiary will receive monthly installments for the remainder of the fixed period.

• Level Income Annuity Option at Age 62, 65, or your Social Security Normal Retirement Age: Under

this option, you receive an increased monthly payment during your lifetime until age 62, age 65, or your Social

Security Normal Retirement Age (SSNRA), as you elect. That means it provides a reduced monthly payment for

your life to provide an approximate level retirement benefit when the reduced monthly payment is

combined with your estimated benefit from Social Security. This option is only available if your requested

Benefit Commencement Date is before the leveling age. The leveling age is the age at which the payment

decreases. The first decreased payment will be the first month following the leveling age. The plan offers the

following leveling ages: 62, 65, or SSNRA.

• 5-, 10-, 15- and 20-Year Certain and Life Annuity with Level Income Option at Age 62, 65, or your

Social Security Normal Retirement Age: Under this option, you receive an increased monthly payment

during your lifetime until age 62, age 65, or your Social Security Normal Retirement Age (SSNRA), as you elect.

Thereafter, it provides a reduced monthly payment payable for your life to provide an approximate level retirement benefit when the reduced monthly payment is combined with your estimated benefit received from Social Security. If you die during the period you elect (5, 10, 15, or 20 years), your beneficiary will receive the remaining payments until all of the specified payments have been made. This option is only available if your Benefit Commencement Date is before the leveling age. The leveling age is the age at which the payment decreases. The first decreased payment will be the first month following the leveling age. The plan offers the following leveling ages: 62, 65, or SSNRA.

Lump Sum vs. Annuity?

Retirees in your city, your state who are eligible for a pension can typically choose between ongoing annuity payments or a lump sum payout. Choosing an annuity effectively means that you would receive income payments for life, which may be appealing if you're worried about outliving your assets, or fear that market volatility could cause your other investments to underperform. Your annuity will continue as long as the pension plan stays solvent, providing steady, reliable income regardless of how long you live in retirement.

The major downside of choosing to receive a monthly pension is that benefits are often reduced following the early and untimely passing of the retiree and/or joint annuitant. In some cases, the pension ends altogether upon death. Additionally, unlike with Social Security, company pensions rarely contain a cost of living allowance (COLA). As a result, receiving a fixed dollar amount as a monthly pension payment means that sum will lose its purchasing power during the course of your retirement.

In contrast, selecting a lump sum payment provides you with the equivalent present value of your monthly pension income stream all at once. If you roll that money over into an IRA and invest it, the idea is that you could potentially achieve a higher rate of growth over time to generate the cash flow needed to make systematic withdrawals throughout your retirement years. Additionally, if a balance remains upon your death, it can go to your surviving spouse or heirs. The flip side of this equation is risk: you need to invest the funds for sufficient growth or face the danger of generating insufficient returns, or running out of money altogether.

Ultimately, the “risk” assessment that should be done to determine whether to take an annuity or lump sum from your Kaiser Permanente pension plan depends on the return you would need to generate to make your lump sum replicate your annuity payments. For instance, if a modest annual return (like 1% to 2%) would create the same cash flow as your monthly pension payments, there is less risk that you will outlive the lump sum. However, if the equivalent cash flow requires a higher, riskier return, there's a chance that those returns won’t manifest and you could run out of money.

The decision you make matters. If you'd like some guidance, reach out to an advisor from The Retirement Group.

Interest Rates and Life Expectancy

Current interest rates, as well as your life expectancy at retirement, have a large impact on lump sum payouts of defined benefit pension plans. Rising rates hurt your lump sum value. The reverse or opposite is also true. Decreasing or lower interest rates will typically increase the lump sum values.

Interest rates are important for determining your lump sum option within the pension plan. However, they have no impact on the annuity options. The Retirement Group believes all KP employees should have a detailed RetireKit Cash Flow Analysis comparing their lump sum value versus the monthly annuity distribution options before making their pension elections. As enticing as a lump sum may seem, the annuity for all or a portion of the pension may still be the better choice, especially in a higher interest rate environment. Every person’s situation is different, and a Cash Flow Analysis can show you how your pension choices may play out over the course of 30 or more years of retirement.

As we continue to monitor the interest rate environment, we will gain more clarity around how the year is trending. Feel free to reach out to The Retirement Group to receive help calculating and assessing your pension options in light of these shifts. We provide a complimentary Retirement Cash Flow analysis or an update to an existing one. By knowing where you stand, you can make a more prudent decision when to retire in your city, your state.

Over half of plan participants in your city, your state admit they don’t have the time, interest, or knowledge needed to manage their 401k portfolio. But the benefits of getting help go beyond convenience. A Charles Schwab study found that those plan participants who get help with their investments tend to have portfolios that perform better: The annual performance gap between those who get help and those who do not is 3.32% net of fees. This means a 50-to-60-year-old participant could see a 79% boost in wealth by age 65 simply by working with an advisor. That’s a pretty big difference.

Getting help can be the key to better 401k results across the board. According to the study, those who used independent professional advice:

- Improved savings rates – 70% of participants who used 401k advice increased their contributions.

- Increased diversification – Participants who managed their own portfolios invested in an average of just under four asset classes, while participants in advice-based portfolios invested in a minimum of eight asset classes.

- Increased likelihood of staying the course – Getting advice increased the chances of participants staying true to their investment objectives, making them less reactive during volatile market conditions and more likely to remain in their original 401k investments during a downturn.

Don’t try to do it alone. Get help with your Kaiser Permanente 401k plan investments. Your nest egg will thank you.

Net Unrealized Appreciation (NUA)

When you qualify for a distribution from your employer-sponsored retirement plan, you typically have three options:

- Roll over your qualified plan to an IRA and continue deferring taxes.

- Take a distribution and pay ordinary income tax on the full amount.

- Take advantage of the net realized appreciation (NUA) strategy and reap the benefits of a more favorable tax structure on gains.

How does the NUA strategy work?

First, employees must be eligible for a distribution from their qualified company-sponsored plan. Generally, this means reaching retirement or age 59 1⁄2. Second, NUA only applies to company stock that has been offered as part of your 401k plan. In other words, if you have Kaiser Permanente stock that has appreciated over time, the NUA strategy may benefit you.

To leverage NUA, you would start by taking a lump sum distribution from your 401k plan, distributing all assets from the plan within a one-year period. The portion of the plan that is made up of highly appreciated company stock is transferred to a taxable brokerage account. The remaining balance can then be rolled into an IRA for further tax deferral.

The tax benefit comes when you transfer the company stock from a tax-deferred account to a taxable account. At this time, by making a NUA election, you can reduce taxes owing on your stock's appreciation, paying long-term capital gains rates based on the cost basis of the stock. The appreciated value of the stock above its basis is not taxed at ordinary income tax rates but at long-term capital gains rates of 0%, 15%, or 20%, depending on your taxable income. The 3.8% Net Investment Income Tax under §1411 may also apply if your income is above $200,000 (single) or $250,000 (MFJ). This could mean a potential savings of 20% or more.

You may be interested in learning more about NUA with a complimentary one-to-one session with a financial advisor from The Retirement Group.

IRA Withdrawal

Your retirement assets likely span several retirement accounts: IRAs, 401ks, taxable accounts, and others.

So, what is the most efficient way to take your retirement income after leaving Kaiser Permanente in your city, your state?

The One Big Beautiful Bill Act also created a new $6,000 above-the-line deduction for taxpayers age 65 and older (available 2025 through 2028), which reduces taxable income and may lower the portion of Social Security benefits subject to federal income tax for many retirees.

You may want to consider meeting your income needs in retirement by first drawing down taxable accounts rather than tax-deferred accounts. This may help your KP retirement assets last longer as they continue to potentially grow tax deferred.

You will also need to plan to take the required minimum distributions (RMDs) from any company-sponsored retirement plans and traditional or rollover IRA accounts. For those born between 1951 and 1959, RMDs begin at age 73. Under SECURE 2.0, this age is 73 for those born between 1951 and 1959, and 75 for those born in 1960 or later.

Two flexible distribution options for your IRA

When you need to draw on your IRA for income or take your RMDs, you have a few choices. Regardless of what you choose, IRA distributions are subject to income taxes and may be subject to penalties and other conditions if you’re under 59½.

- Partial withdrawals: Withdraw any amount from your IRA at any time. If you’re 73 or over, you’ll have to take at least enough from one or more IRAs to meet your annual RMD.

- Systematic withdrawal plans: Structure regular, automatic withdrawals from your IRA by choosing the amount and frequency to meet your income needs after retiring from Kaiser Permanente. If you’re under 59½, you may be subject to a 10% early withdrawal penalty (unless your withdrawal plan meets Code Section 72(t) rules).

Your tax advisor can help you understand distribution options, determine RMD requirements, calculate RMDs, and set up a systematic withdrawal plan.

.png)

6.png)