Claiming Social Security is one thing—understanding how your claim works is something else entirely. Understanding Social Security is a difficult but crucial step in assessing your retirement paycheck. For many Americans, Social Security benefits are core to their retirement income strategy. However, when and why you claim them depends on your overall withdrawal strategy.

To help you make an informed decision, let's explore three main steps you should follow to solidify your Social Security strategy at PG&E:

Step 1. Decide when to claim your Social Security benefits

Social Security benefits can be significant, but at the end of the day, they're just one part of your overall financial picture. When considering the timing of your claim, keep this general principle in mind: The later you begin receiving benefits, the larger those benefits will be.

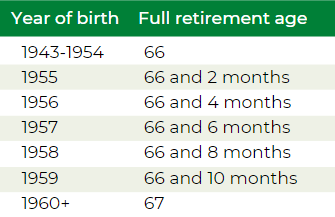

The full monthly Social Security retirement benefit is based on applying at the Full Retirement Age (FRA), which is age 67 for those born 1960 or later. For every year you wait after you reach the FRA, your benefit amount increases 8%. It reaches a maximum at age 70. If we do the math, we can determine that, if you start claiming at age 70, your monthly benefit will be 124% the full benefit.

However, you can also apply before you reach FRA, as early as age 62. You will receive a reduced benefit if you do so, but this option could make sense for those who want to start claiming their benefit earlier for longevity reasons.

Step 2. Understand the tax implications

For all but the lowest-income retirees, Social Security benefits are actually taxable. Only individuals with provisional income under $25,000, or $32,000 if married filing jointly, receive their benefits tax-free. Otherwise, up to 85% of your benefits will be treated as taxable income.

Furthermore, depending on where you live, your Social Security benefits may even be taxed at the state level. If you plan to move for retirement, the tax regime in the state you're moving to can be a relevant consideration.

Step 3. Start preparing today

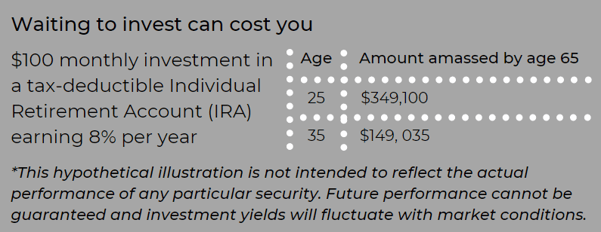

Even if your retirement is right around the corner, you can make decisions today that will impact you for years, or decades, to come. For instance, delaying your Social Security claiming date even a year or two can snowball into a significant benefit. To bridge the gap between their retirement date and their claiming date, some people create a "slush fund" while they're working to take the place of the Social Security benefits they would receive from claiming at FRA. Whether these funds come from a 401k, IRA, or brokerage account, integrating a bit of extra padding in your planning can pay off in the long run.

.png)

.png)

6.png)