New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Retirement Guide for Blue Cross Blue Shield Employees: Tax Rates & Inflation

The sustained volatility in crude oil markets, with a closing futures price of $68.75 for WTI and $72.22 for Brent as of July 06, 2026 and annualized swings near 80%, creates economic effects that extend far beyond energy companies. Energy price swings affect insurer investment portfolios and the broader economic conditions that drive policy demand and claims patterns. Tax planning at Blue Cross Blue Shield benefits from understanding how energy-driven market movements create opportunities for timing capital gains, Roth conversions, and strategic loss harvesting. Working with a financial advisor can help you position your planning strategy for sustained energy price uncertainty.

Source: Yahoo Finance

Blue Cross Blue Shield is distributing $2.6 billion in class action settlement checks to resolve a significant legal claim, marking a major financial commitment to plan participants and claimants. The company has also faced operational challenges, including a recent insurance denial for breast cancer reconstruction coverage that prompted public scrutiny from both patients and healthcare providers regarding coverage decisions. Meanwhile, a former Blue Cross Blue Shield facility in Eagan, Minnesota has become the focus of development activity, with 3M's health care spinoff Solventum pursuing the site as a future operational hub with support from local government and state assistance, while real estate developer Trammell Crow was selected to oversee the project. Additionally, Blue Cross and Blue Shield of Alabama reached an agreement to keep Jackson Hospital open in Montgomery, demonstrating the insurers' continued commitment to healthcare access in their service regions.

Source: Currents API / Google News

With wrapped up and going into the new year, the IRS just released Revenue Procedure -45 and Notice -61 which detail the tax changes and cost of living adjustments for . The main points of this new release that will most likely affect Blue Cross Blue Shield employees would be:

- This year, the tax filing deadline is on April 18, instead of the typical April 15.

- The standard deduction for married couples filing jointly for the current tax year rises to $32,200 up $800 from the prior year.

- For single taxpayers and married individuals filing separately, the standard deduction rises to $12,950 for , up $400, and for heads of households, the standard deduction will be $19,400 for the current tax year up $600.

Also, the personal exemption for the current tax year remains at 0, as it was for . This elimination of the personal exemption was a provision in the Tax Cuts and Jobs Act.

If you experienced a job change, retirement or lapse in employment from Blue Cross Blue Shield, the “lookback†rule may be an important option to consider when filing taxes this year. You’ll also have the option to use your earned income for your return thanks to changes from the American Rescue Plan Act. This rule is mainly used for calculation of the Earned Income Tax Credit and the Child Tax Credit.

Remote workers employed by Blue Cross Blue Shield might face double taxation on state taxes. Due to the pandemic, many employees moved back home which could have been outside of the state where they were employed. Last year, some states had temporary relief provisions to avoid double taxation of income, but many of those provisions have expired. There are only six states that currently have a ‘special convenience of employer’ rule: Connecticut, Delaware, Nebraska, New Jersey, New York, and Pennsylvania. If you work remotely for Blue Cross Blue Shield, and if you don't currently reside in those states, consult with your tax advisor if there are other ways to mitigate the double taxation.

Retirement account contributions: Contributing to your Blue Cross Blue Shield 401k plan can cut your tax bill significantly, and the amount you can save has increased for . In , the IRS has raised the contribution limit for a 401k to $24,500 - up by $1,000. Meanwhile, Blue Cross Blue Shield workers who are older than 50 years old are eligible for an extra catch-up contribution of $6,500.

There are important changes for the Earned Income Tax Credit (EITC) that you, as a taxpayer employed by Blue Cross Blue Shield, should know:

- The income threshold has been increased for single filers with no children; the American Rescue Plan Act temporarily boosted it from $543 to $1,502 in ; this expansion has not been carried over to the tax year.

- Married taxpayers filing separately can qualify: You can claim the EITC as a married filing separately if you meet other qualifications. This wasn't available in previous years.

Increased deduction for cash charitable contributions: In years past, the threshold was $300 for both single and joint filers, but in that changed to $300 for single filers and up to $600 for joint filers.

Child Tax Credit changes:

- A $2,000 credit per dependent under age seventeen..

- Income thresholds of $400,000 for married couples and $200,000 for all other filers (single taxpayers and heads of households).

- A 70 percent, partial refundability affecting individuals whose tax bill falls below the credit amount.

Tax Brackets

-png.png?width=575&name=image%20(18)-png.png)

Inflation reduces purchasing power over time as the same basket of goods will cost more as prices rise. In order to maintain the same standard of living throughout your retirement after leaving Blue Cross Blue Shield, you will have to factor rising costs into your plan. While the Federal reserve strives to achieve 2% inflation rate each year, in that rate shot up to 7% a drastic increase from ’s 1.4%. While prices as a whole have risen dramatically, there are specific areas to pay attention to if you are nearing or in retirement from Blue Cross Blue Shield, like healthcare. Many Blue Cross Blue Shield corporate retirees depend on Medicare as their main health care provider and in that healthcare out-of-pocket premium is set to increase by 14.5%. In addition to Medicare increases, the cost of over-the-counter medications is also projected to increase by at least 10%. The Employee Benefit Research Institute (ERBI) found in their report that couples with average drug expenses would need $296,000 in savings just to cover those expenses in retirement. It is crucial to take all of these factors into consideration when constructing your holistic plan for retirement from Blue Cross Blue Shield.

*Source: IRS.gov, Yahoo, Bankrate

Blogs You May Enjoy:

Source: Is it Worth the Money to Hire a Financial Advisor?, the balance, 202

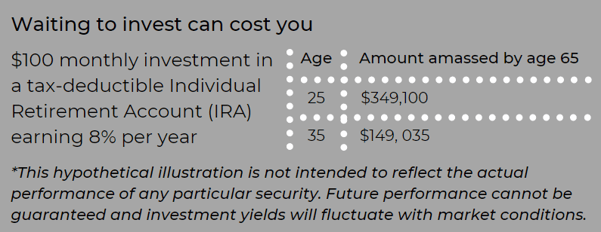

Starting to save as early as possible matters. Time on your side means compounding can have significant impacts on your future savings. And, once you’ve started, continuing to increase and maximize your contributions for your Blue Cross Blue Shield 401(k) plan is key.

Highest Average Earnings is the monthly average of your regular earnings for the 36 consecutive months in which they’re the highest.

In most cases, this will be the sum of your last 36 months divided by 36.

The applicable interest rate is a separate average of each of the three segment rates for the fifth, fourth and third months preceding your annuity start date. The three segment rates are calculated by the IRS according to regulations that are also part of the Pension Protection Act of and reflect the yields of short-, mid-, and long-term corporate bonds. (Note: Chevron also has Legacy Unocal and Legacy Texaco Retirement Plans)

Different Plans

Similar to Chevron, AT&T has many different plans available. With AT&T, they have different pension plan formulas for management & non-management. Lets look at a sample non-management plan.

AT&T non-management employees have their own Craft/non-management pension plan. Let's take a look at a pension example for a gentleman by the name of Joe Smith who is hourly and using the Craft/non-management pension plan.

In 1990, Joe is hired by AT&T and participates in the Craft Pension Plan:

Craft Pension Plan

- Craft has a defined benefit plan that uses pension bands.

- A pension band determines your benefits based on your job title/grade level/occupation.

- Joe will receive a monthly dollar amount into his account for each year of service.

- Joe's benefit (pension band may change yearly).

- A pension band determines your benefits based on your job title/grade level/occupation.

Craft Pension Example

Let's assume Joe is working as a Cable Splicing Technician and is in Pension Band 120. He is interested in retiring this year, in and wants to calculate his Craft Pension benefit.

If a Pension is offered, Blue Cross Blue Shield's retirement plan will generally allow for different forms of payment:

Single Life Annuity

- The monthly Single Life Annuity is the benefit from which all of the optional forms of payment under the plan are derived.

- Pays a fixed amount each month for retiree’s lifetime.

- A death benefit may be payable to your beneficiary.

- A death benefit is payable if vested and employee dies before employment with Blue Cross Blue Shield ends or start of receiving benefits.

Lump-Sum Option (Most Oil Companies Offer a Lump Sum)

- Lump-sum payment is actuarially equivalent to the total annuity you would have received as a Single Life Annuity during your lifetime.

- Calculated using actuarial factors based on your age and the interest rate in effect on your annuity starting date.

- No death benefits are payable.

NOTE: Lump-Sum vs. Annuity -Â With decreasing interest rates, your lump-sum payout will increase.

Life & Term-Certain Annuity Option

- Smaller than the Single Life Annuity.

- 5, 10, or 15 year period certain.

- If you have multiple beneficiaries or if your beneficiary is your estate or trust, remaining payments converted actuarially to a lump-sum.

- No death benefits are payable.

Looking for a second opinion about your retirement from Blue Cross Blue Shield? Click here to speak to financial advisor today or call (800) 200-9838.

Joint & Survivor Annuity

Upon your death, a percentage of your monthly benefit is paid to your joint annuitant for his or her lifetime

Reduction factors may apply depending on Blue Cross Blue Shield's policy.

Uniform Income

Receive same level of income before and after receiving Social Security benefits

The level of income may change at a certain age. For example, in the Chevron Uniform Income policy:

Before age 62, employees receive a larger monthly annuity from the plan

After age 62, when Social Security benefit is available, employees receive a smaller monthly annuity from the plan

Each company has varying rules in regards to Uniform Income. Review Blue Cross Blue Shield's SPD or talk to an advisor to find out the rules for your specific plan.

*These are examples and Blue Cross Blue Shield's plan may be different.

Interest Rates and Life Expectancy

In many defined benefit plans, like the ExxonMobil pension plan, current and future retirees are offered a lump-sum payout or a monthly pension benefit. Sometimes these plans have billions of dollars worth of unfunded pension liabilities, and in order to get the liability off the books, Blue Cross Blue Shield may offer a lump-sum.

Depending on life expectancy, the initial lump-sum is typically less money than regular pension payments over a normal retirement time frame. However, most individuals that opt for the lump-sum plan to invest the majority of the proceeds, as most of the funds aren't needed immediately after retirement from Blue Cross Blue Shield.

Something else to keep in mind is that current interest rates, as well as your life expectancy at retirement, have an impact on lump-sum payout options of Blue Cross Blue Shield defined benefit pension plans. Lump-sum payouts are typically higher in a low interest rate environment, but be careful because lump-sums decrease in a rising interest rate environment.

Additionally, projected pension lump-sum benefits for active Blue Cross Blue Shield employees will often decrease as an employee ages and their life expectancy decreases. This can potentially be a detriment of continuing to work, so it is important that you run your pension numbers often and thoroughly understand the impact that timing has on your benefit. Other factors such as income needs, need for survivor benefits, and tax liabilities often dictate the decision to take the lump-sum over the annuity option on the pension.

They can help determine your eligibility, get you and/or your eligible dependents enrolled in Medicare or provide you with other government program information. For more in-depth information on Social Security, please call us.

Check the status of your Social Security benefits before you retire from Blue Cross Blue Shield. Contact the U.S. Social Security Administration, your local Social Security office, or visit ssa.gov.

Are you eligible for Medicare or will be soon?

If you or your dependents are eligible after you leave your telecom industry company, Medicare generally becomes the primary coverage for you or any of your dependents as soon as they are eligible for Medicare. This will affect Blue Cross Blue Shield-provided medical benefits.

You and your Medicare-eligible dependents must enroll in Medicare Parts A and B when you first become eligible. Medical and MH/SA benefits payable under the Blue Cross Blue Shield-sponsored plan will be reduced by the amounts Medicare Parts A and B would have paid whether you actually enroll in them or not.

For details on coordination of benefits, refer to Blue Cross Blue Shield's summary plan description.

If you or your eligible dependent don’t enroll in Medicare Parts A and B, your provider can bill you for the amounts that are not paid by Medicare or your Blue Cross Blue Shield-specific medical plan … making your out-of-pocket expenses significantly higher.

According to the Employee Benefit Research Institute (EBRI), Medicare will only cover about 60% of an individual’s medical expenses. This means a 65-year-old couple, with average prescription-drug expenses for their age, will need $259,000 in savings to have a 90% chance of covering their healthcare expenses. A single male will need $124,000 and a single female, thanks to her longer life expectancy, will need $140,000.

Check Blue Cross Blue Shield's plan summary to see if you’re eligible to enroll in Medicare Parts A and B.

If you become Medicare-eligible for reasons other than age, you must contact Blue Cross Blue Shield’s benefit center about your status.

While you may be ready for some rest and relaxation, without the stress and schedule of your full-time career with Blue Cross Blue Shield, it may make sense to you financially, and emotionally, to continue to work.

Financial benefits of working

Make up for decreased value of savings or investments. Low interest rates make it great for lump sums but harder for generating portfolio income. Some people continue to work to make up for poor performance of their savings and investments.

Maybe you took an offer from Blue Cross Blue Shield and left earlier than you wanted with less retirement savings than you needed. Instead of drawing down savings, you may decide to work a little longer to pay for extras you’ve always denied yourself in the past.

Meet financial requirements of day-to-day living. Expenses can increase during your retirement from Blue Cross Blue Shield and working can be a logical and effective solution. You might choose to continue working in order to keep your insurance or other benefits — many employers offer free to low cost health insurance for part-time workers.

Emotional benefits of working

You might find yourself with very tempting job opportunities at a time when you thought you’d be withdrawing from the workforce.

Staying active and involved. Retaining employment after Blue Cross Blue Shield, even if it’s just part-time, can be a great way to use the skills you’ve worked so hard to build over the years and keep up with friends and colleagues.

Enjoying yourself at work. Just because the government has set a retirement age with its Social Security program doesn’t mean you have to schedule your own life that way. Many people genuinely enjoy their employment and continue working because their jobs enrich their lives.

Blue Cross Blue Shield employees interested in planning their retirement may be interested in live webinars hosted by experienced financial advisors. Click here to register for our upcoming webinars for Blue Cross Blue Shield employees.

https://www.irs.gov/newsroom/irs-provides-tax-inflation-adjustments-for-tax-year-

https://news.yahoo.com/taxes--important-changes-to-know-164333287.html

https://www.nerdwallet.com/article/taxes/federal-income-tax-brackets

https://www.bankrate.com/taxes/child-tax-credit--what-to-know/

What type of retirement savings plan does Blue Cross Blue Shield offer to its employees?

Blue Cross Blue Shield offers a 401(k) retirement savings plan to help employees save for their future.

How can employees of Blue Cross Blue Shield enroll in the 401(k) plan?

Employees can enroll in the Blue Cross Blue Shield 401(k) plan by completing the enrollment process through the company’s HR portal.

Does Blue Cross Blue Shield provide any matching contributions to the 401(k) plan?

Yes, Blue Cross Blue Shield offers a matching contribution to the 401(k) plan, which helps employees maximize their retirement savings.

What is the eligibility requirement for employees to participate in Blue Cross Blue Shield's 401(k) plan?

Employees are typically eligible to participate in Blue Cross Blue Shield's 401(k) plan after completing a specified period of service, as outlined in the plan documents.

Can employees of Blue Cross Blue Shield change their contribution percentage to the 401(k) plan?

Yes, employees can change their contribution percentage to the Blue Cross Blue Shield 401(k) plan at any time, subject to the plan's guidelines.

What investment options are available in Blue Cross Blue Shield's 401(k) plan?

Blue Cross Blue Shield offers a variety of investment options in its 401(k) plan, including mutual funds, target-date funds, and other investment vehicles.

Is there a vesting schedule for the employer match in Blue Cross Blue Shield's 401(k) plan?

Yes, Blue Cross Blue Shield has a vesting schedule for employer matching contributions, which determines when employees gain full ownership of those funds.

How can employees access their 401(k) account information at Blue Cross Blue Shield?

Employees can access their 401(k) account information through the online portal provided by Blue Cross Blue Shield’s retirement plan administrator.

Are there any fees associated with Blue Cross Blue Shield's 401(k) plan?

Yes, there may be administrative fees associated with the Blue Cross Blue Shield 401(k) plan, which are disclosed in the plan documents.

What happens to an employee's 401(k) balance if they leave Blue Cross Blue Shield?

If an employee leaves Blue Cross Blue Shield, they have several options for their 401(k) balance, including rolling it over to another retirement account or leaving it in the Blue Cross Blue Shield plan if permitted.

For more information you can reach the plan administrator for Blue Cross Blue Shield at "225 north michigan ave. " Chicago, IL 60601; or by calling them at 888-630-2583.

https://www.bcbs.com/documents/pension-plan-2022.pdf - Page 5, https://www.bcbs.com/documents/pension-plan-2023.pdf - Page 12, https://www.bcbs.com/documents/pension-plan-2024.pdf - Page 15, https://www.bcbs.com/documents/401k-plan-2022.pdf - Page 8, https://www.bcbs.com/documents/401k-plan-2023.pdf - Page 22, https://www.bcbs.com/documents/401k-plan-2024.pdf - Page 28, https://www.bcbs.com/documents/rsu-plan-2022.pdf - Page 20, https://www.bcbs.com/documents/rsu-plan-2023.pdf - Page 14, https://www.bcbs.com/documents/rsu-plan-2024.pdf - Page 17, https://www.bcbs.com/documents/healthcare-plan-2022.pdf - Page 23

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.