New Update: Rising Oil Costs are Affecting Retirement Plans. Will you be impacted?

Managing Uncertainty, Biases, and Behavioral Intelligence for ConocoPhillips Employees and Retirees

ConocoPhillips sits at the front of the energy value chain where crude prices translate immediately into cash flow. The recent environment of 80% annualized volatility and a $50 to $120 price range has amplified both the upside and the uncertainty. Management must balance expanding production during high-price windows against the risk of overcommitting capital before the next downturn. ConocoPhillips employees should ensure their retirement savings strategy accounts for the concentrated exposure that comes from working in a commodity-sensitive industry, where income and investments may move together. Given this uncertainty, a financial advisor who understands energy sector dynamics can help you position your financial plan for long-term success regardless of oil price direction.

Â

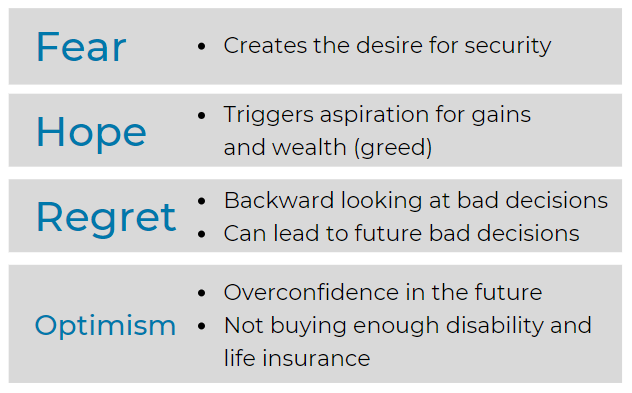

Financial Decision-making in Extremely Uncertain Times

Â

Emotional Intelligence Development and Maintenance

Â

Integrates retirement planning and modern portfolio theory with recent findings in the fields of neuro economics and behavioral finance to achieve an emotional state for making better financial decisions.

Â

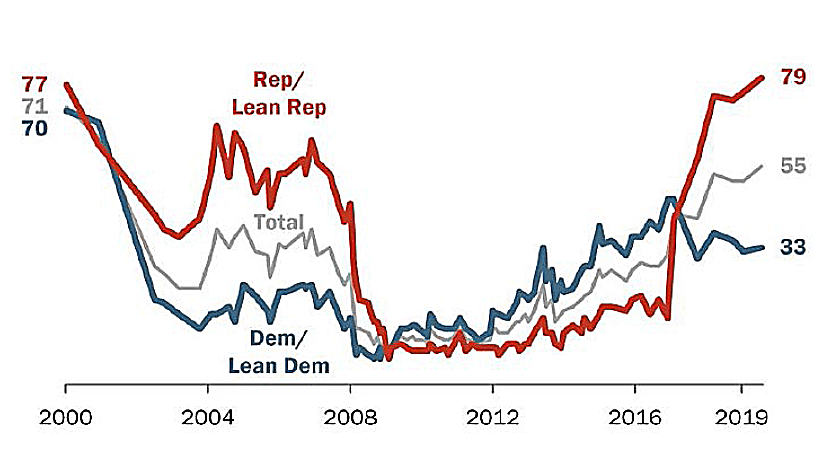

Three Uncertain Periods:

Â

S&P 500 Index

Â

U.S. Initial Jobless Claims, Per Week

Total U.S. Nonfarm Payrolls

Â

GDP Annualized Growth Rate

Â

During the last 75.75 years (since 1945) there have been 190 declines of 5% or greater.

Â

Before finalizing any estate plan, it is worth examining how ConocoPhillips's employer-sponsored benefits fit into the broader picture. According to publicly available information, ConocoPhillips maintains a cash balance pension plan, which defines your retirement benefit as a hypothetical account balance that grows over your career through pay credits and interest credits. Under ERISA, cash balance plan benefits vest on a three-year cliff schedule. ConocoPhillips also offers retiree healthcare benefits to eligible employees. Because the specifics of your cash balance account balance, vesting status, and benefit options depend on your individual employment history and plan documents, We encourage you to review your Summary Plan Description (SPD) or speak with ConocoPhillips's HR or benefits team for the most current details.

Sources: Standard & Poor’s Corporation; Copyright 2026 Crandall, Pierce & Company

Â

The Market's Reaction to a Financial Crisis

Cumulative total return of a balanced strategy: 60% stocks, 40% bonds

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Not to be construed as investment advice. Returns of model portfolios are based on back-tested model allocation mixes designed with the benefit of hindsight and do not represent actual investment performance. See the “Balanced Strategy Disclosure and Index Descriptions†pages in the Appendix for additional information.

Â

-

Pivotal to understanding ourselves

Â

Â

Â

Â

Nasdaq Composite: 2010-2026

Â

Â

Â

Â

Â

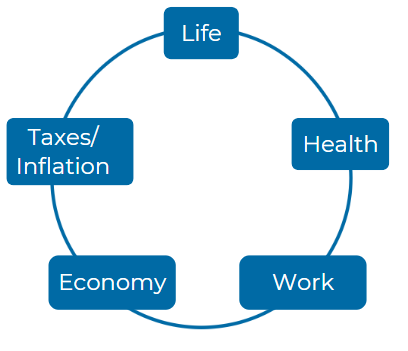

Consider these five Elements:

Â

Â

How does the retirement process at ConocoPhillips provide guidance to employees in selecting the most beneficial form of payment? In what ways can employees utilize available resources to maximize their understanding of the pension options offered by ConocoPhillips?

The retirement process at ConocoPhillips provides employees with various resources to guide them in selecting the most beneficial form of pension payment. Employees can access the "How to Choose the Best Form of Payment" link on Your Benefits Resources™ (YBR) to learn more about their options and determine what works best for their financial situation(ConocoPhillips_Your_Ret…).

What steps must be completed by employees at ConocoPhillips to ensure they initiate their retirement process accurately and avoid any delays? How crucial is the timing of these steps in determining the Benefit Commencement Date (BCD)?

Employees at ConocoPhillips must initiate the retirement process by requesting their pension paperwork 60-90 days before their Benefit Commencement Date (BCD). Timing is crucial, as missing deadlines may delay the BCD and associated payments. Completing all steps on time ensures that the retirement process flows smoothly(ConocoPhillips_Your_Ret…).

Given the complexities associated with the lump-sum pension payment option at ConocoPhillips, what considerations should employees take into account before electing this choice? How does the current interest rate at the Benefit Commencement Date impact the lump-sum amount?

Before electing a lump-sum pension payment, ConocoPhillips employees should consider the current interest rate at their BCD, as it directly affects the lump-sum amount. A higher interest rate typically reduces the lump-sum payment, making timing and rate awareness critical(ConocoPhillips_Your_Ret…).

In what ways can ConocoPhillips employees ensure their Pension Election Authorization form is completed correctly to facilitate timely pension payments? What are the implications of not adhering to the required notarized consent for married participants?

Ensuring the correct completion of the Pension Election Authorization form is vital for timely pension payments. For married participants, notarized spousal consent is required, and failure to provide this could result in delays or issues with payment processing(ConocoPhillips_Your_Ret…).

How does choosing direct deposit for pension payments at ConocoPhillips streamline the retirement process for employees? What should employees know about setup and changes regarding direct deposit after initiating their pension benefits?

Choosing direct deposit for pension payments simplifies the process for employees at ConocoPhillips, as it enables automatic payments to their bank account. Employees can set up direct deposit during their retirement process or update it at a later time(ConocoPhillips_Your_Ret…).

For employees considering rolling over their lump-sum pension payment from ConocoPhillips, what procedures should they follow to ensure compliance with IRS regulations and to avoid tax penalties? How can effective planning influence the success of this rollover?

Employees electing to roll over their lump-sum pension payment must follow specific IRS regulations to avoid tax penalties. Effective planning, such as obtaining rollover paperwork and adhering to IRS rules, ensures compliance and smooth fund transfer(ConocoPhillips_Your_Ret…).

What resources does ConocoPhillips provide for employees to calculate and project their retirement income? How can these tools empower employees to make informed decisions regarding their future financial security?

ConocoPhillips provides employees with tools such as the "Project Retirement Income" feature on YBR, empowering them to calculate and project their retirement income. These resources help employees make informed decisions about their financial future(ConocoPhillips_Your_Ret…).

How do deadlines play a pivotal role in the benefits process for retiring employees at ConocoPhillips, and what specific dates must be adhered to in order to avoid payment delays? Can you provide examples of consequences resulting from missed deadlines?

Deadlines are critical in ConocoPhillips' retirement process, as missing them can delay pension payments. For example, requesting pension paperwork after the 15th of the month can delay the BCD by a month, affecting the pension payout date(ConocoPhillips_Your_Ret…).

What are the added advantages for employees at ConocoPhillips who actively seek assistance or information from the Benefits Center during their retirement planning? How can this proactive approach enhance their overall retirement experience?

Employees who seek assistance from the Benefits Center during their retirement planning benefit from personalized guidance. This proactive approach ensures that they fully understand their options and deadlines, enhancing their overall retirement experience(ConocoPhillips_Your_Ret…).

How can employees at ConocoPhillips contact the Benefits Center to receive personalized assistance in navigating their retirement options? What specific resources and support can they expect when reaching out for help?

ConocoPhillips employees can contact the Benefits Center by calling 800-622-5501 or accessing YBR online. The Benefits Center provides personalized assistance and guidance, helping employees navigate their pension options effectively(ConocoPhillips_Your_Ret…).

For more information you can reach the plan administrator for ConocoPhillips at p.o. box 4783 Houston, TX 77079; or by calling them at 918-661-6199.

https://www.sec.gov/Archives/edgar/data/1163165/000119312523077649/d367442d10k.htm - Page 9, https://hrcpdocctr.conocophillips.com/Documents/HR-Benefits-documents/AE/Retiree_Handbook.pdf - Page 18, https://static.conocophillips.com/files/resources/conocophillips-pension-plan_implementation-stateme.pdf - Page 13, https://hrcpdocctr.conocophillips.com/Documents/HR-Benefits-documents/2022_SARs-ConocoPhillips.pdf - Page 22, https://hrcpdocctr.conocophillips.com/Documents/2024_Annual_Enrollment/COBRA_Guide.pdf - Page 15, https://hrcpdocctr.conocophillips.com/Documents/SPD/Savings_SPD.pdf - Page 25, https://retiree.uhc.com/content/dam/retiree/pdf/conocophillips/2024/2024-PG-ConocoPhillips-15750.pdf - Page 20, https://retiree.uhc.com/content/dam/retiree/pdf/conocophillips/2022/2022_Plan_guide_ConocoPhillips_15750-15773.pdf - Page 27, https://hrcpdocctr.conocophillips.com/Documents/2023_Annual_Enrollment/COBRA_Guide.pdf - Page 30, https://retiree.uhc.com/content/dam/retiree/pdf/conocophillips/2023/2023-conocophillips-pg-15750.pdf - Page 35

Help shape our next stories

Choose the topics you’d love to read more about. Your input helps us focus on content that matters to you.