These are the estate planning concepts we'll be looking at today, and they are especially applicable to Fortune 500 employees. We'll talk about planning for incapacity first, briefly discussing both healthcare issues and property management issues. Then we're going to talk about planning for death, focusing on wills and probate, tax basics, lifetime gifting, trusts, and the role of life insurance in estate planning.

We'd like to remind Fortune 500 employees and retirees that not all types of healthcare directives are effective in all states. It's important to be sure to execute the one(s) that will be effective for you. You can leave instructions about the medical care you would want if conditions were such that you couldn't express your own wishes. There are three different ways to do this: with a living will; a durable power of attorney for health care, which is referred to as a health-care proxy in some states; and a Do Not Resuscitate order, or DNR.

A living will is a document that lists the types of medical treatment you would want, or not want, under particular circumstances. For example, your living will might state that you would not want life support if you fell into a persistent vegetative state. With a living will, you'll have to think about all possible scenarios where you would want a specific action to be taken, and then put your wishes in writing so that the reader will clearly understand them.

A durable power of attorney for health care, or health-care proxy, lets one or more family members or other trusted individuals (who are called agents) make medical care decisions for you. Unlike a living will, with this type of healthcare directive you don't have to envision specific circumstances. You simply grant authority to your agent or agents to make decisions for you.

A Do Not Resuscitate order is used for a different purpose. Let's say that you're in the hospital, lingering and suffering from a terminal illness, and you don't want the hospital staff to take life-saving measures if you suddenly go into cardiac or respiratory arrest. To make sure your wishes are carried out, you may be able to get your doctor to issue a DNR. A DNR is a legal form, signed by both you and your doctor, that's posted by your bed to give staff members the permission they need to carry out your wishes.

Be careful if you're using a DNR. Some states require their own DNR form, and some states require one DNR form if you're in the hospital, and a different DNR form if you're in a nursing home. Be aware also that some states don't recognize some of these healthcare directives. So, depending on your state, you might need one, two, or all three of them.

There are three ways you can plan to have your financial affairs taken care of for you in the event you become incapacitated. You can arrange to own property jointly, appoint an agent using a durable power of attorney, or create and put the property in a living trust and name someone to take over the management of the trust if something happens to you.

Granting joint ownership of your property to another person allows that person to have the same access to the property as you do. If you become incapacitated, your joint owner simply acts instead. For example, if you and your spouse have a joint checking account, each of you can make deposits and write checks. So, if you were to go into a coma, your spouse would still be able to make the mortgage payments on time.

A durable power of attorney lets you name family members or other trusted individuals to make financial decisions or transact business on your behalf (just like with the durable power of attorney for health care). In addition to joint ownership and a durable power of attorney, using a living trust is another common strategy. We'll talk in more detail about trusts later, but for now, we want Fortune 500 employees and retirees to know that a living trust can be used in planning for incapacity because someone (called a successor trustee) can step into your shoes to manage the property in the trust if something should happen to you.

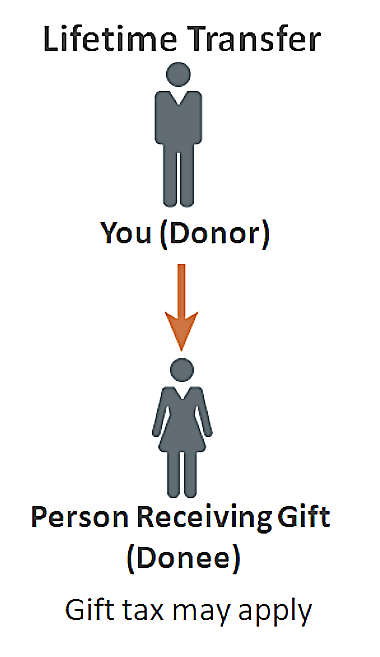

Gift tax applies to transfers made during your life

Certain gifts are excluded (e.g., $16,000 annual gift tax exclusion)

$12,060,000 excluded from all transfers (gifts and estates) combined in 2022

The $12,060,000 exclusion is the largest in the history of the federal gift and estate tax

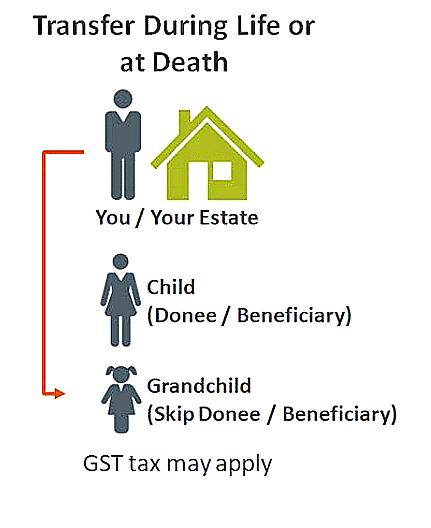

Estate tax applies to transfers made at death

Generally, does not apply to transfers made to spouse or charity

$12,060,000 excluded from all transfers (gifts and estates) combined in 2022

Any portion of exclusion used for gifts will be unavailable to the estate

The generation-skipping transfer (GST) tax may apply to transfers made to someone more than one generation below you

$12,060,000 GST tax exemption in 2022

Unlike the gift and estate tax exclusion, the GST tax exemption is NOT portable

Some key tax figures are adjusted each year for inflation. You can see here how the exclusion and exemption amounts have changed. The Tax Cuts and Jobs Act, signed into law in December 2017, doubled the gift and estate tax exclusion amount and the GST tax exemption to about $11,200,000 in 2018. After 2025, they are scheduled to revert to pre-2018 levels and cut by about one-half. If your estate is larger than the exclusion or exemption, you may want to do some estate planning to minimize the potential impact of transfer taxes.

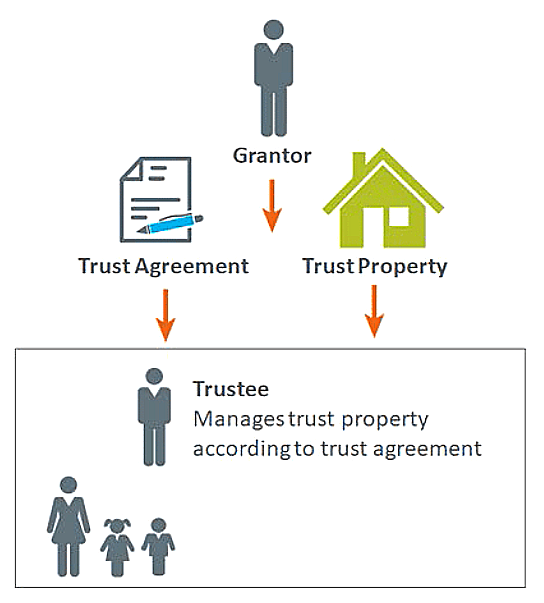

Legal entity that holds property

Parties to a trust: grantor, trustee, beneficiary

Living trusts vs. testamentary trusts

Revocable trusts vs. irrevocable trusts

A common strategy to avoid estate tax on life insurance uses a trust to own and hold the life insurance policy. Such a trust is commonly referred to as an irrevocable life insurance trust, or "ILIT." If the ILIT owns the life insurance policy. the proceeds of the policy will not be included in your estate for estate tax purposes. However, this is only true if the strategy is correctly implemented. Ultimately, you'll need to work with an experienced estate planning attorney if this strategy is of interest to you.

But let me give you a basic idea of how an ILIT can work. You create an irrevocable trust, name someone as trustee, and name beneficiaries. The trustee buys a new life insurance policy on your life. The ILIT owns the policy. You make cash gifts to the ILIT. The trustee notifies the beneficiaries as you make the cash gifts. The beneficiaries have a limited window of time during which they have a technical right to withdraw your cash gift, but they don't, since withdrawing the gifts would defeat the purpose of the trust. As the withdrawal periods elapse, the trustee uses the cash gifts to pay the premiums on the policy to the insurance company.

1. ILIT receives proceeds of life insurance policy

2. Proceeds not subject to estate tax

3. Proceeds distributed according to terms of trust

4. Beneficiaries receive full proceeds, free from estate tax

At your death, the ILIT receives the proceeds of the life insurance policy. If properly implemented, no estate tax is due on the life insurance proceeds, and the funds are distributed according to the terms of the trust. The beneficiaries of the ILIT receive funds free from estate tax. Like most trusts, irrevocable life insurance trusts are a more advanced estate planning strategy, and I've just attempted to give you a very basic understanding of how they might apply to your situation. If you are interested in learning more, I'd be happy to provide you with additional information.