Financial Planning

Fiscal Responsibility Act of 2023

The Fiscal Responsibility Act of 2023, signed into law on June 3, 2023, suspends the federal debt ceiling until January 2025. The legislation also...

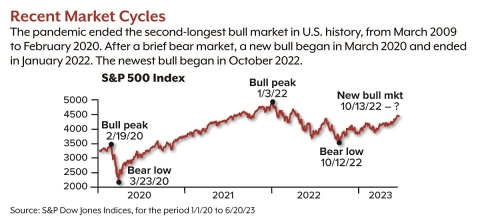

On June 8, 2023, the S&P 500 index closed at 4,293.93, just over 20% higher than its lowest recent closing value of 3,577.03 reached on October 12, 2022.1 According to a common definition of market cycles, this indicated that the benchmark index was officially in a bull market after a bear market that began in January 2022. By this definition, the current bull market began on October 13, 2022, the day after the bear market ended at its lowest point. In more general terms, a bull market is an extended period of rising stock values. Bull markets tend to last longer than bear markets, and bull gains tend to be greater than bear losses. Since the end of World War II, the average bull market has lasted more than five years with a cumulative gain of 177%. By contrast, the average bear market has lasted about a year with a cumulative loss of 33%.2Although a bull market is typically a time for celebration by investors, the current bull is being met cautiously, and it is unclear whether it will keep charging or shift into retreat. While it is impossible to predict market direction, here are some factors to consider.

One reason the new bull might not seem convincing is that (as of late June) the S&P 500 remains well below the record bull market peak in early January 2022.3 Investors who hold positions in the broader market are still looking at paper losses and could face real losses if they choose to sell, a situation that may not generate the kind of widespread confidence that often drives extended rallies.

The current bull is already eight months old, and it's unknown how much longer it might take to recover the total bear loss of about 25%, but recent history offers contrasting possibilities. The last bull market regained the pandemic bear loss of 34% in five months and went on to a cumulative gain of 114%. The long bull market that followed the Great Recession took more than four years to recover an even steeper loss of 57%. But that bull kept charging and went on to a cumulative gain of 400%.4–5

A more pressing question is whether the recent surge could be a temporary bear market rally that quickly slips back into bear territory. This happened during the bear markets of 2000–2002 and 2007–2009. However, in 12 other "bear exits" since World War II, a gain of 20% from the most recent low was the beginning of a solid bull market.6

Another key concern is that the current rally has been driven by large technology companies, which have posted big gains, due in part to excitement over the future of artificial intelligence.7 The S&P 500 is a market-cap-weighted index, which means that companies with larger market capitalization (number of shares multiplied by share price) have an outsized effect on index performance. As of May 31, the ten biggest companies, including eight technology companies, accounted for more than 30% of index value.8 Fewer than one out of four S&P 500 stocks have beaten the index in 2023, and nearly half have dropped in value. While it is not unusual for a relatively small number of companies to drive a rally, the current situation is more imbalanced than usual, and it remains to be seen whether exuberance for Big Tech will spread to the larger market.9–10

While the stock market sometimes seems to have a mind of its own, it is anchored over the longer term to the U.S. economy, and the current economy continues to send mixed signals. The long-predicted recession has so far failed to materialize, and both consumer spending and the job market remain strong.11 On the other hand, inflation, while improving, is still too high for a healthy economy. Although the Fed paused its aggressive rate hikes in June — one reason for the market rally — a majority of Fed officials projected two more increases by the end of the year, and Fed Chair Jerome Powell confirmed the prospect of higher rates in Congressional testimony on June 21.12

Higher interest rates are intended to slow the economy and inflation by making it more expensive for consumers and businesses to borrow, which should slow consumer spending and business growth — and could send the economy into a recession. Although it may seem counterintuitive, bull markets usually begin during a recession, or to look at it another way, the market usually hits bottom while the economy is down and recovers along with the broader economy. Along the same lines, a bull market typically begins when the Fed is lowering interest rates to stimulate the economy, not when it's raising them to slow it down.13 The current bull will have to buck both of these trends to sustain momentum. And if a recession does develop, it could turn the bull into a bear.

Although investor enthusiasm can carry the market a long way, corporate earnings are the most fundamental factor in market performance, and the earnings picture is also mixed. Earnings declined by 2% in Q1 2023 — less of a loss than analysts expected but the second consecutive quarter of earnings declines. The slide is expected to continue with a 6.4% projected decrease in Q2, which would be the largest decline since the pandemic rocked the market in Q2 2020. The good news is that earnings growth is expected to return in the second half of the year, with robust growth of 8.2% in Q4. As with the current market rally, however, the surge is projected to be driven by large technology companies.14

Clearly, this bull market faces serious headwinds, and it may be some time before its true character emerges. While market cycles are important, it's generally not wise to overreact to short-term shifts and better to focus on a long-term investment strategy appropriate for your personal goals, time frame, and risk tolerance.

The return and principal value of stocks fluctuate with changes in market conditions. Shares, when sold, may be worth more or less than their original cost. The S&P 500 index is an unmanaged group of securities that is considered to be representative of the U.S. stock market in general. The performance of an unmanaged index is not indicative of the performance of any specific investment. Individuals cannot invest directly in an index. Past performance is no guarantee of future results. Actual results will vary. Forecasts are based on current conditions, are subject to change, and may not come to pass.

The Fiscal Responsibility Act of 2023, signed into law on June 3, 2023, suspends the federal debt ceiling until January 2025. The legislation also...

On January 19, 2023, the outstanding debt of the U.S. government reached its statutory limit, commonly called the debt ceiling.

Understand Section 303 stock redemptions in the context of closely-held corporations. Discover its role in estate planning and its tax implications...